Early October saw the latest update in Telefónica’s plans to reduce its presence in LATAM. News broke that Entel and América Móvil had entered a non-binding agreement to potentially buy its Chilean business, a move that would mark a realignment of Chile’s telecom landscape.

But first, why is Telefónica looking to sell in Chile? Chile’s fragmented market structure has long limited operators’ ability to reach scale — a challenge this deal directly addresses. The market is currently split between four main providers, with none commanding more than a 40% share. It’s also a challenging financial market, as seen in WOM’s struggles with bankruptcy in the last few years. Meanwhile, all operators are having to build out increasingly advanced services — like fiber and 5G — while competing for a narrow pool of subscribers. With this context, it’s clear that consolidation is needed to stabilize the telecoms sector, and enable ongoing investment in delivering superior connectivity.

Entel’s Fiber Ambitions and Fixed-Line Opportunity

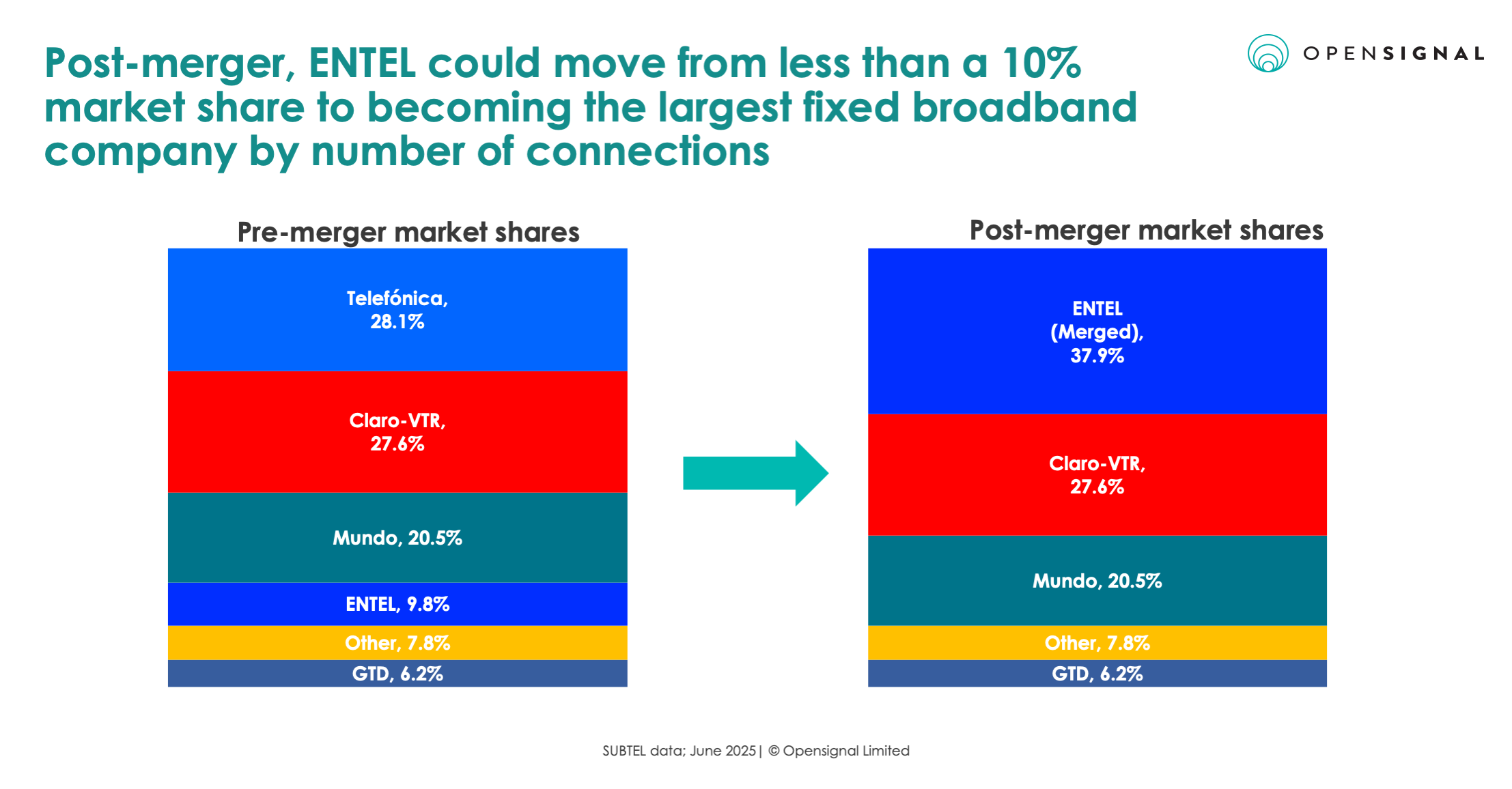

Despite its financial challenges, Telefónica is not a small player — and this offers its competitors a rare opportunity to buy scale. It represents almost a quarter of the mobile market in Chile, and nearly a third of fixed broadband — and this strong position across mobile and broadband makes its exit a rare chance to rebalance competition and investment incentives. If the reported split of Telefónica’s assets proves accurate, this would have two outcomes. Firstly, Claro would become the largest player in the mobile space. Meanwhile Entel would move from a <10% market share to over a third of the fixed broadband space.

For Entel, this additional scale would be backed up by robust infrastructure. Over the course of 2024, Telefónica invested in upgrading its legacy copper network to fiber. As a result, it now commands the largest share of the Chilean fiber market. These fiber assets would allow Entel a significantly larger presence in the broadband space, and more ability to offer converged services to more of its mobile subscriber base, likely improving retention and efficiency within the operator.

Telefónica’s mobile infrastructure offers América Móvil 5G scale

On the mobile side, it’s no surprise that Entel is less interested in Telefónica’s (Movistar) assets. Its network strength was clear when it won the bulk of our awards in our February 2025 report. However, for América Móvil (Claro), Movistar’s 5G assets would be useful. It was relatively late to the 5G landscape in the market, getting permission from SUBTEL to use its current 3.5GHz spectrum for 5G in 2023, and acquiring more mid-band 5G spectrum in the June 2024 auction.

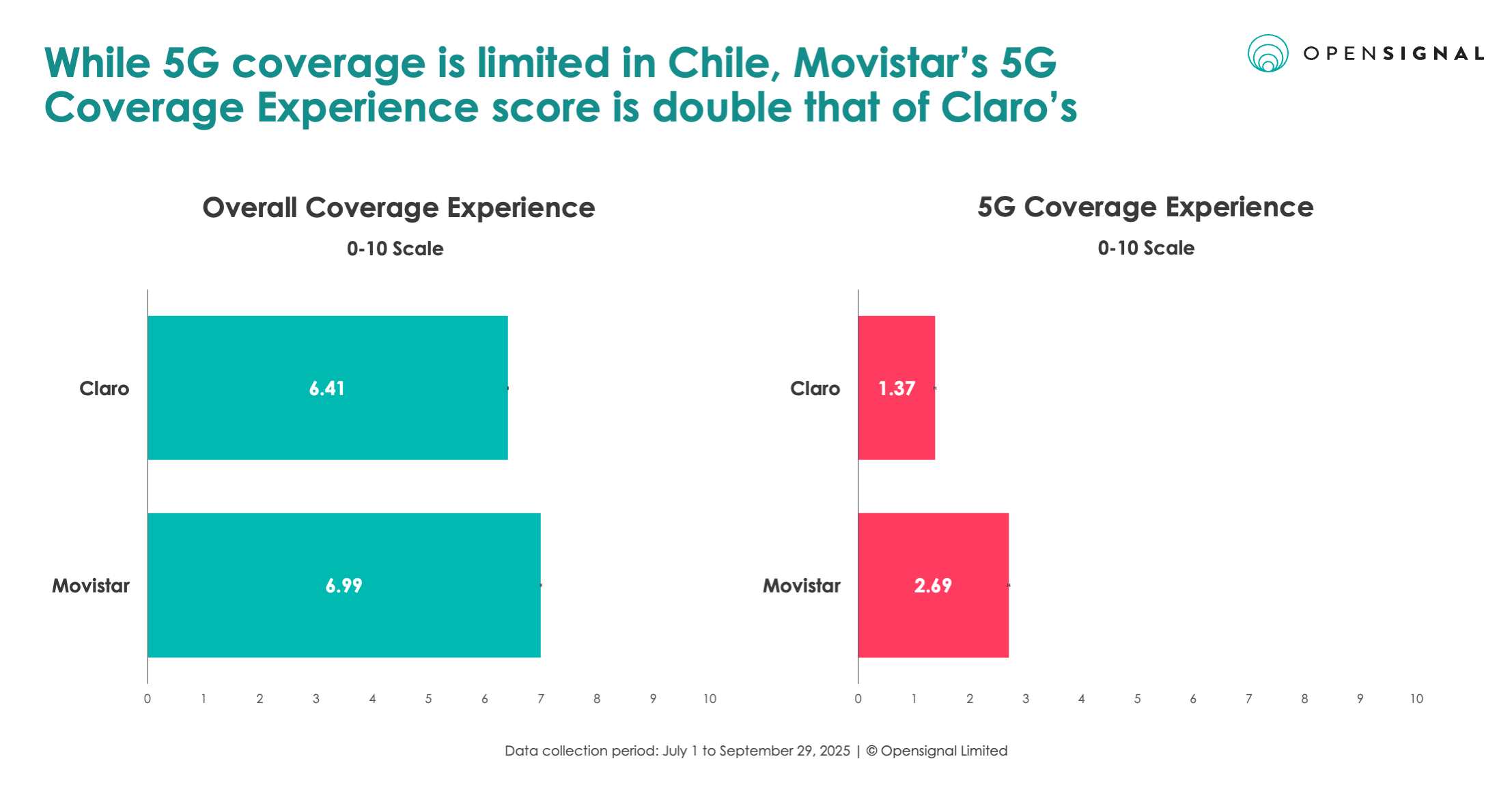

5G adoption in Chile is also still modest — GSMA Intelligence data suggests 31% of connections are 5G as of Q2 2025. Within that, Claro has a greater share of 5G connections than Movistar, however Movistar’s score for 5G Coverage Experience in Opensignal’s data is nearly double that of Claro’s, showing its broader footprint ready to facilitate wider adoption. Movistar also has a greater overall Coverage Experience.

This suggests that Movistar’s underlying physical infrastructure could also prove useful to Claro. As part of its spectrum licensing conditions it must reach 100 new localities and 1,500 kilometres of roads, which Movistar’s footprint could help achieve. Assuming the two networks interconnect following a merger, existing Claro customers may then see wider access to 5G. Meanwhile, Movistar customers may well see slight improvements in overall network reliability and consistency – as Claro has historically outperformed Movistar on both our Consistent Quality and Reliability Experience metrics.

Why (regulated) market consolidation is much needed in Chile

We’ve previously released blogs on market consolidation in Europe, which highlight the challenges of scale in markets characterized by lots of smaller countries, even with operator groups spanning multiple countries in a region. In this regard, LATAM’s market structure mirrors Europe’s. It too wrestles with achieving the types of efficiencies that are needed to support rising network investment demands like 5G and fiber deployments. Finding revenue growth to offset these costs takes time. However, Telefónica’s loss could be mutually beneficial as both Entel and América Móvil increase their customer bases and assets in the region. Consolidation could finally allow operators to align revenues with the high capital demands of next-generation networks — a balance many LATAM markets still struggle to achieve.

The proposed deal is the latest in a long line of consolidation moves, both in LATAM and worldwide. As operators seek efficiency gains alongside network upgrades, balancing investment, competition, and affordability will remain a central challenge both through the remainder of 2025 and likely many years to come. For all involved, the move likely would lead to longer term robustness in a more streamlined market, where operators are able to balance pricing with sustainable service upgrades.

For more information on Chile, read our recent research here, or subscribe to our newsletter to keep up to date with our latest reports.

The editorial views expressed in this article are solely those of the author and do not necessarily reflect the views of Opensignal.

Opensignal Limited retains ownership of this insight including all intellectual property rights, data, content, graphs & analysis. Reports and insights produced by Opensignal Limited may not be quoted, reproduced, distributed, published for any commercial purpose (including use in advertisements or other promotional content) without prior written consent. Journalists are encouraged to quote information included in Opensignal reports and insights provided they include clear source attribution. For more information, contact [email protected].