At the inaugural MWC Doha, I had the pleasure of moderating the session:

“Telcos as the Digital Spine: The Role of Telcos as AI Service Providers”.

It was a timely discussion. AI may be the industry’s loudest buzzword, but for operators, the question is much more grounded:

Are telcos genuinely evolving into the foundational infrastructure that will power AI ecosystems? Or are we still circling around the edges of what’s possible?

Our goal in the session was simple: to strip away the noise and focus on what generates measurable, bankable value today. We sought answers to three crucial questions:

- Where is AI already delivering measurable, bankable value?

- What must networks evolve into to support AI at scale?

- And crucially: how do telcos monetise AI without defaulting to “technology for technology’s sake”?

The conversation included opening presentations from Dell Technologies and Jazz, followed by a dynamic panel including Ooredoo, MTN Chenosis, Ericsson, and Turkcell — each offering a different vantage point on how AI is reshaping telecom strategy.

Setting the scene: AI beyond the buzzwords

I opened the session with a challenge familiar to every operator: AI only matters if it improves productivity or simplifies the customer journey. Everything else is noise.

This is where telcos must differentiate themselves.

AI should help:

- run more efficient networks (CapEx/OpEx savings).

- deliver more personalised and effortless customer experiences

- And create new, commercially viable services

The goal isn’t to deploy AI. The goal is to deliver outcomes. And globally, we are beginning to see proof points:

Key Insights from the Opening Presentations

Dell Technologies: AI Needs the Right Network DNA

Eric van Vliet highlighted a critical truth: AI doesn’t simply fit onto existing infrastructure. It fundamentally requires distributed compute, cloud-native core, and programmable, modular architectures. His main point was clear: AI’s value collapses unless networks become flexible enough to host real-time, data-intensive processes seamlessly.

Jazz: AI as a driver of national development

Kazim Mujtaba (Jazz) grounded the discussion in emerging-market realities. Jazz’s work across health-tech, insure-tech, ed-tech, gaming, and marketplaces shows the scale of opportunity when connectivity + platforms + AI intersect. He showed that AI is fast becoming a tool for national digital uplift, not just operator transformation.

Panel Highlights: the shift toward AI-native telcos

Our speakers represented four distinct perspectives: a consumer-first operator (Mustafa Peracha, Chief Consumer Officer, Ooredoo Qatar), a pan-African API ecosystem ( Saad Syed, CEO, MTN Chenosis), a network vendor driving RAN/Core transformation ( Zoran Lazarevic, CTO, Ericsson), and a digital-first telecom company ( Yusuf Yiğit, AI and Analytics Solutions Director, Turkcell).

Across the panel, three themes stood out.

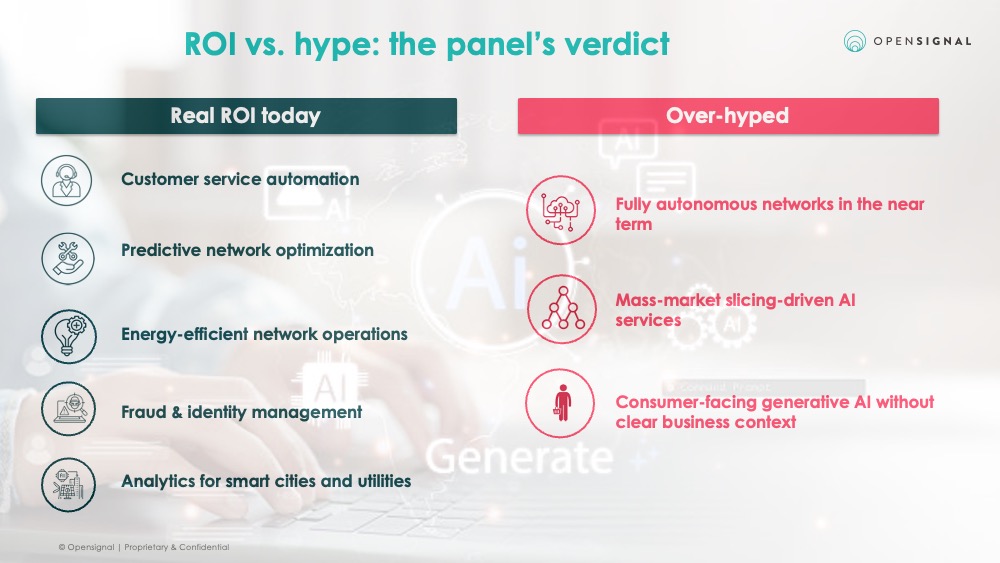

1. The AI-Powered Network: from reactive to autonomous

The starting point for value creation is internal efficiency. Mr Mustafa Peracha of Ooredo Qatar emphasised that AI’s strongest near-term impact is productivity — both for customers and internal operations.

Ooredoo Qatar’s vision is centred on AI-first customer interactions, ensuring simplicity and speed, over unnecessary complexity..

Moving from immediate customer gains to core operational infrastructure, the focus shifts to prediction. Yusuf Yiğit explained how Turkcell is embedding AI across network operations and digital services.

This isn’t about hype; it’s about:

- Predicting performance and automating routine processes.

- Preparing for 5G/6G services built around agility and responsiveness.

Ultimately, he noted, this necessitates a network foundation capable of anticipating needs, self-tuning, and eventually self-governance. Acknowledging the extreme complexity of this autonomous future, the discussion turned to the role of network vendors.

Zoran Lazarevic of Ericsson framed the core issue: The network is becoming too complex for humans to manage manually.

Distributed compute, multi-layer architectures, and real-time workloads require AI-driven optimisation. One of his examples was Ericsson’s collaboration with Mobily to support connectivity services for millions of pilgrims through AI during Hajj 2025.

If AI runs the network for efficiency, how is that operational value captured externally? We shifted the conversation to a commercial opportunity.

Saad Syed captured the commercial reality: after years of fragmented API attempts, MTN’s Chenosis is repositioning its platform to monetise AI capabilities. Real examples include offering AI agents, translation APIs, and cross-operator capabilities. His assessment was sharp: “We’re not doing AI for the sake of AI. We’re solving real problems for customers who have budgets.”

2. Autonomous networks: ambition vs reality

Are we already in the AI-backbone era? According to Mr Zoran of Ericsson, the answer is yes — partially.

AI is active across:

- the business layer

- the service orchestration layer

- the resource layer (RAN/core/transport)

What’s missing is agent-to-agent coordination, a key focus for 6G standardisation.

Mr Yusuf of Turkcell pointed to three practical challenges preventing full autonomy:

- Readiness of talent within the organisation.

- Achieving end-to-end closed-loop automation.

- Ensuring interoperability between various AI systems.

Mr Mustafa of Ooredo Qatar was realistic about the timeline: pockets of automation will scale fast, but full network autonomy requires robust governance models, clearer intent frameworks (Intent-Based Networking), and aligned ecosystems. In summary: progress, yes. Hype, no.

3. Monetising AI: From Connectivity to B2B2X Models

The consensus was that the traditional connectivity revenue model cannot capture the value of AI. The strategic shift is to move up the value chain by packaging AI capabilities.

Leading the charge in defining the new growth vector was Mr Saad Syed (MTN Chenosis). He detailed how MTN is leveraging its multi-country footprint to bring AI-enabled APIs to market, not just internally, but across operators, creating continental-scale value. The key insight is that the target market is not individual developers, but enterprises with concrete, monetisable use cases, signaling a clear pivot to B2B2X, where telcos enable others' digital transformation.

Final Thoughts

The central message from all our speakers was consistent: AI will not replace the role of telcos - it will redefine it.

From autonomous operations and hyper-personalised customer experience to new B2B2X service models, operators hold a unique opportunity to become the true digital spine of entire economies. This future is achievable, but only if AI is deployed with clarity, discipline, and measurable outcomes.

Thank you to all our speakers and to everyone who joined us for a conversation that brought much-needed realism, ambition, and direction to the AI–telecom intersection.

If you are interested in more insights like that, make sure you visit our website. We will be at MWC 2026, so follow this link if you would like to set up a meeting with us.

Opensignal Limited retains ownership of this insight including all intellectual property rights, data, content, graphs & analysis. Reports and insights produced by Opensignal Limited may not be quoted, reproduced, distributed, published for any commercial purpose (including use in advertisements or other promotional content) without prior written consent. Journalists are encouraged to quote information included in Opensignal reports and insights provided they include clear source attribution. For more information, contact [email protected].