Webinar: We’ve complemented this report with two in-depth webinar discussions, featuring report authors, Micah Sachs (VP Global Broadband Products), and Opensignal's regional experts for Europe, the Gulf, and APAC. Watch or listen to the on-demand recording here for analysis on Europe and the Gulf, or here for learnings from APAC.

Fixed Wireless Access (FWA) has rapidly emerged as the most disruptive force in broadband in decades. Its rise is driven by the unique ability to scale availability to millions of homes within months, while giving mobile operators a way to monetize their vast 5G spectrum investments. Backed by existing national distribution channels and strong brand recognition, FWA is finally delivering on a promise two decades in the making. Yet even its strongest advocates admit the network experience is not yet on par with fiber or modern cable. The critical question is: how far behind is it? In this report, we analyze the network experience gap between FWA and fixed-line broadband across 11 key markets, and show how these differences shape the varied role FWA can play in the global broadband ecosystem.

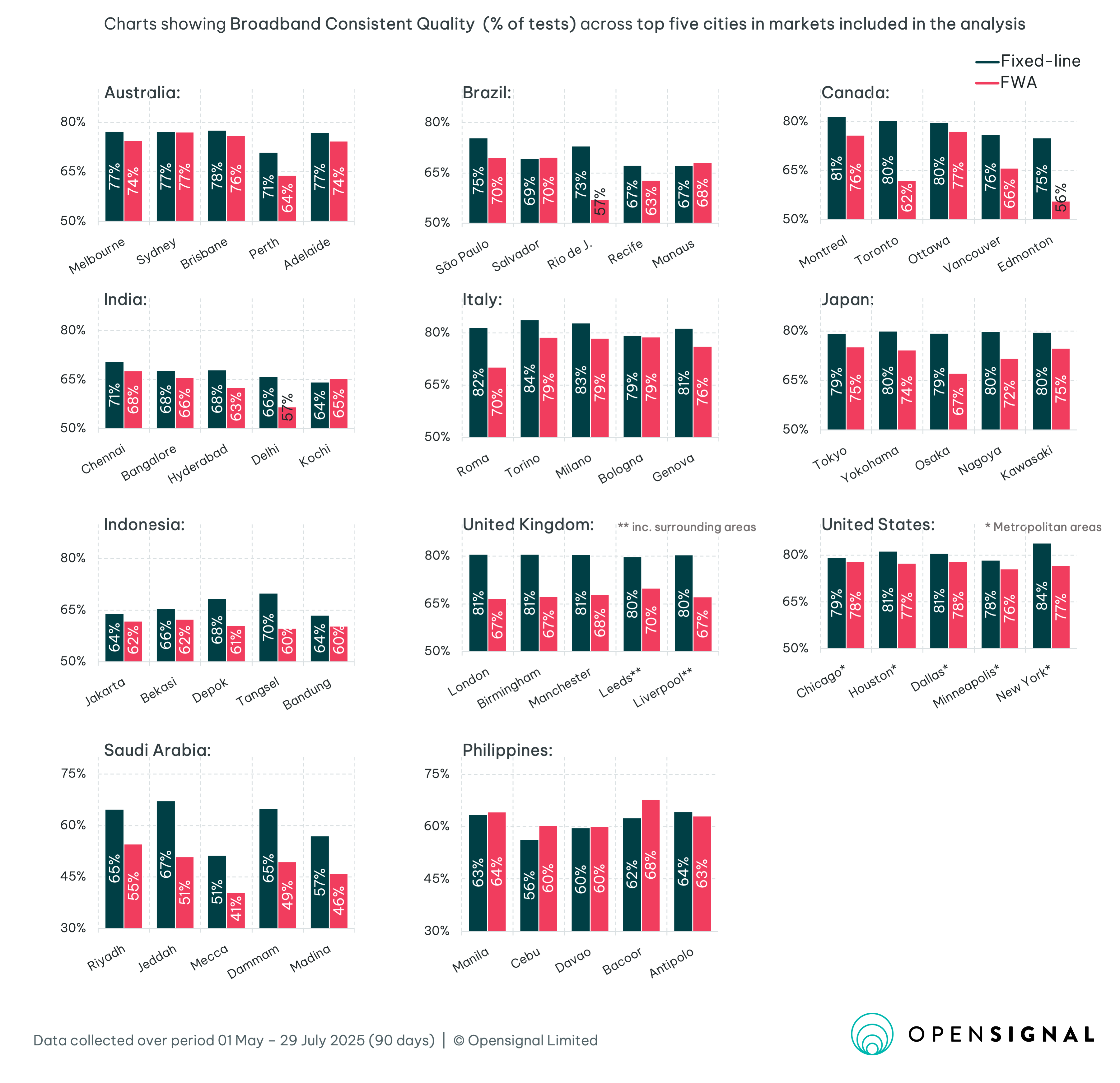

Our analysis is anchored in Broadband Consistent Quality (CQ), our flagship metric that condenses everyday broadband performance into a single measure. We define ‘Fixed-line’ as broadband delivered through fiber, xDSL, or cable (HFC). For ‘Fixed Wireless Access’ our focus is limited to services operating on 4G LTE and 5G using licensed spectrum, thereby excluding a small number of wireless internet service providers using unlicensed spectrum.

Key Findings:

- In a handful of markets, FWA experience is almost on par with fixed-line.

The role of FWA varies sharply across markets. In the U.S. and India, it has become a true growth engine for mobile operators. Fixed wireless CQ scores only around five percentage points below fixed-line, placing the U.S. and India in the ‘Near-parity’ category. The U.S. and India now count around 13 and 8 million FWA subscribers, respectively, making them the largest FWA markets in the world.

By contrast, most other markets fall into ‘Good enough’ or ‘Niche’ tiers, where fixed-line retains a clear advantage. Seven of the countries we analyzed illustrate this gap – from early 5G FWA leaders like Saudi Arabia and Japan, to 4G-heavy markets such as Indonesia, and those where FWA remains niche, including Brazil, the U.K., and Canada.

- Capacity management is critical.

Across all markets, the FWA is seeing a larger decline in performance during times of peak usage than fixed-line – but the impact varies. The U.S. and India have maintained an FWA congestion curve that is comparable to fixed-line, demonstrating that through strategic network management FWA can be scaled without overloading their networks. By contrast, in markets like the U.K., Canada, Indonesia and the Philippines, structural limitations in spectrum availability, backhaul capacity, and overall network resources create systemic bottlenecks – limiting FWA’s growth potential.

- Fixed wireless advantages extend beyond absolute performance.

Even when experience falls short of fixed-line, FWA still complements ongoing broadband development – extending coverage rapidly alongside fiber and cable networks. FWA’s key advantages are accessibility, affordability and ease of deployment. By leveraging existing mobile infrastructure, it can connect new customers in days rather than months. Unlike fiber or cable that require costly, time-intensive rollouts, FWA is especially impactful in underserved lower-density areas where traditional broadband is uneconomical.

Table of Contents:

FWA’s gap with fixed-line has narrowed in several markets

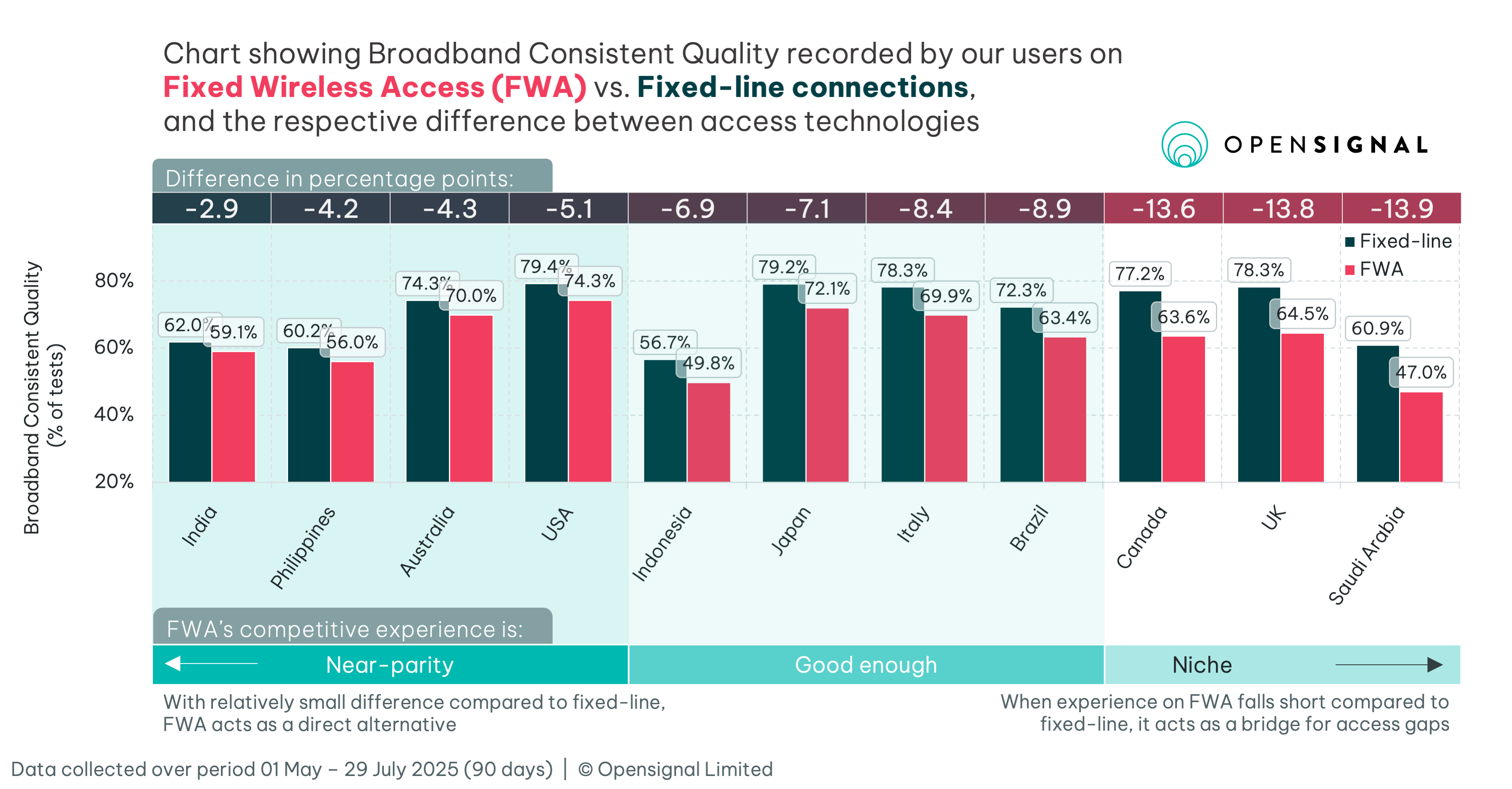

In this report, we examine eleven markets to assess the impact of FWA, varying both in terms of technology penetration and geographic context. While the scale of adoption and operator strategies differ significantly, one consistent pattern emerges: fixed-line networks deliver a higher quality of experience than FWA in every market. The size of this performance gap defines FWA’s competitive position, shaping whether it falls into the ‘Near-parity’, ‘Good enough’, or ‘Niche’ experience bands within the local fixed-line broadband landscape.

In this analysis, we use Broadband Consistent Quality metric to benchmark experience – as the metric assigns a single value to how good the experience is of a user’s connections on a network. It evaluates whether the network is sufficient for common everyday activities involved in browsing the web, video streaming, making calls, or online gaming and is expressed as the share of tests that pass the defined CQ thresholds.

The larger disparity will translate into a noticeably weaker broadband experience on FWA during normal activity, leaving FWA users’ significantly worse off compared to that on fixed-line. At one end of the spectrum, markets like India, the Philippines, Australia, and the United States show narrow differences in measured experience. This is particularly significant in the U.S. and India – where the relatively small performance gap with fixed-line makes FWA a highly competitive alternative. With 13.4 million and 7.9 million subscribers, the U.S. and India are the world’s two largest FWA markets (as reported by the U.S. FWA providers and by India’s regulator, TRAI, respectively).

At the other end of the spectrum, Saudi Arabia, the United Kingdom, and Canada record the widest gaps in user experience, with differences of 13.6 to 13.9 percentage points. As a result, FWA’s role in these markets is largely transitional – filling coverage gaps or serving only the most cost-conscious households – while also exposing the constraints of the mobile network resources on which it depends.

Capacity management underpins FWA’s growth

The sustainability of FWA growth hinges on how operators manage shared spectrum resources. Unlike fixed-line’s dedicated last-mile connections, FWA depends on spectrum that must serve both fixed broadband households and mobile users. Capacity management is therefore the central challenge, as fixed subscribers typically consume far more data than mobile users – for example T-Mobile in the USA reported FWA usage of over 400GB per month, while Nokia reports 12x monthly data consumption compared to mobile data users in India. The trade-offs also vary sharply by geography. In densely populated urban areas the spectrum is the most contested resource, while in rural areas the backhaul becomes the constraining factor, especially in markets where the existing fixed-line infrastructure is underdeveloped.

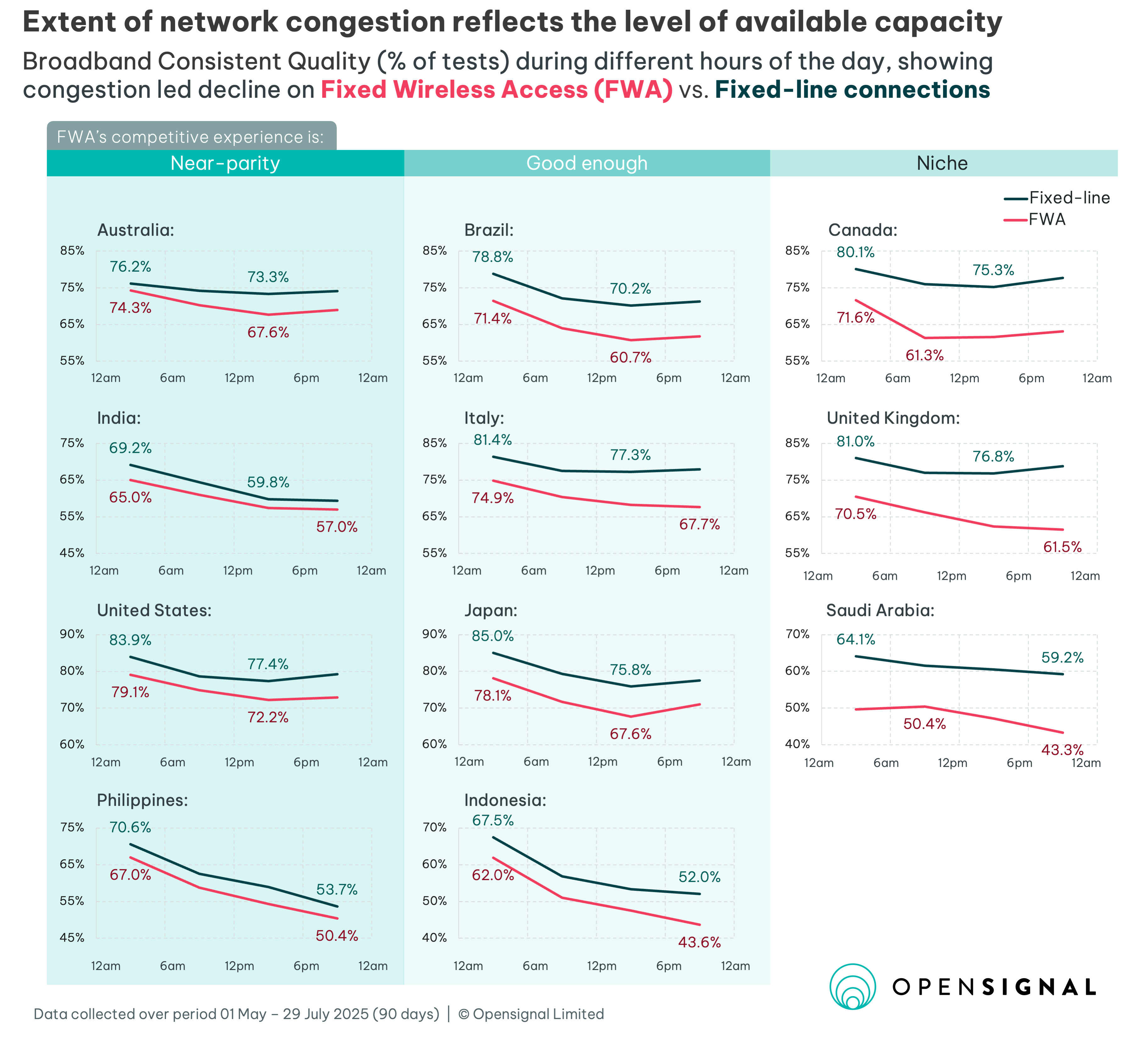

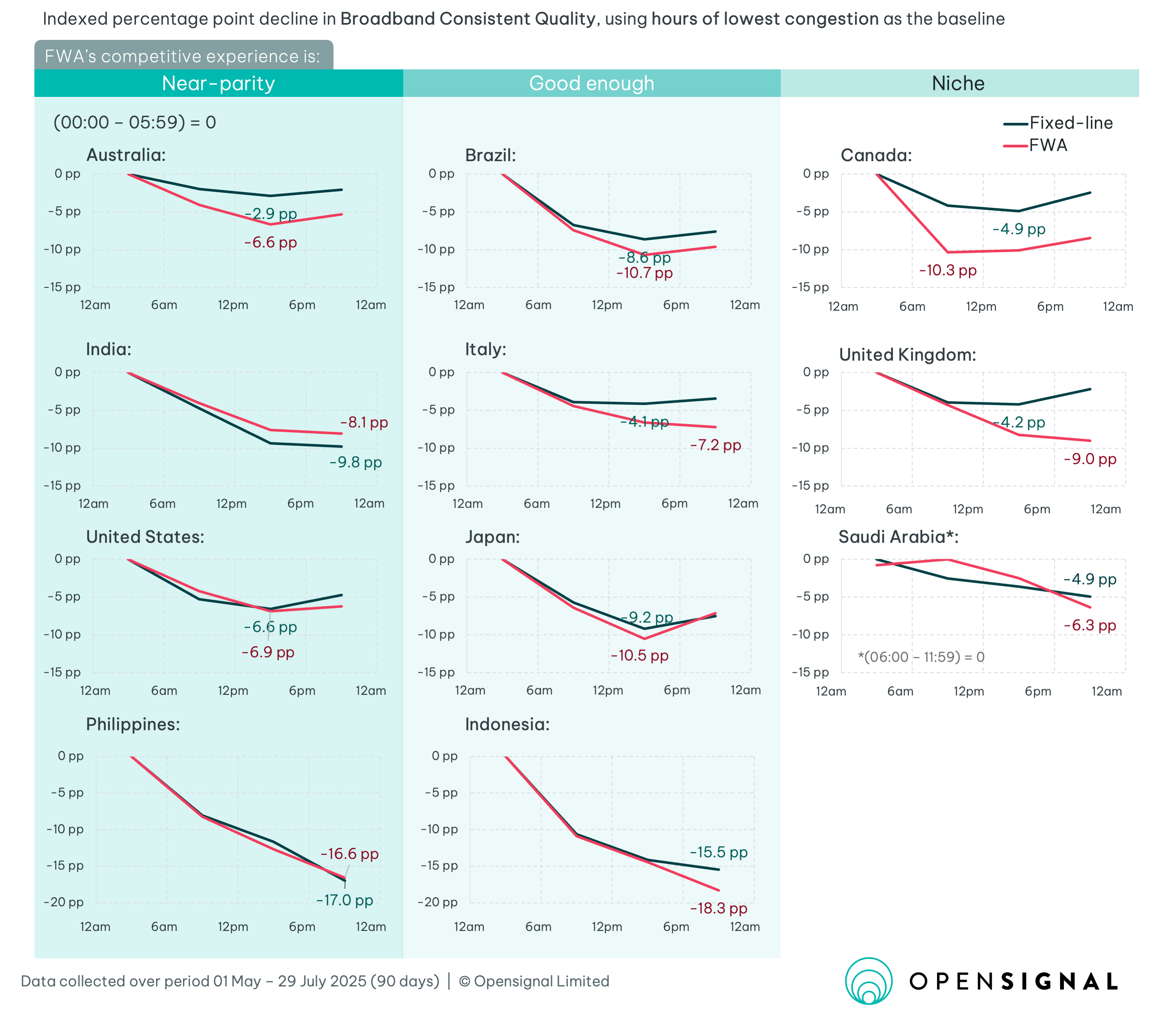

To assess the impact of congestion, we compare Consistent Quality during peak and off-peak hours. To calculate congestion-related decline, we assess the difference in CQ during the hours of lowest congestion (typically between 12am and 6am) and the busier hours (typically between 6pm and 12am), looking at the difference between the two access technologies. The charts showing indexed impact of congestion for each market are included in the appendix.

Across markets, three patterns emerge. In the U.S. and India, the markets with the largest number of fixed wireless subscribers, congestion impacts are nearly identical to fixed-line. This indicates effective capacity management – by restricting FWA to areas with surplus capacity and offloading heavy usage where possible, providers in the two markets have enabled expansion of FWA without overloading their networks. Our U.S. users’ CQ measure declines by -6.9pp on FWA compared with -6.6pp on fixed-line, while India reports -8.1pp versus -9.8pp. This puts experience on FWA into a ‘near-parity’ position in relation to fixed-line.

The ‘good enough’ group shows moderate gaps. Here, we see the impact of broadband and mobile users taxing the same shared cellular network resources causing noticeable degradation between off-peak and peak hours. In Italy and Japan, declines on FWA range from -7.2pp to -10.5pp, compared with smaller drops on fixed-line.

In the U.K. and Canada, where comparative experience on FWA is ‘niche’, the experience on wireless networks slows by -9pp and -10.3pp under load, while fixed-line degradation is mild. These results highlight how FWA struggles to match the resilience of mature fixed networks.

In developing markets, network constraints can be much more severe on both forms of access. Our FWA users in Indonesia and Philippines see declines of -18.3pp and -16.6pp, respectively, with fixed-line experience doing marginally better only in Indonesia. This symmetry on fixed-line suggests systemic capacity shortages where neither mobile nor fixed broadband can consistently meet demand, but it also means FWA remains relatively competitive compared to fixed-line in that context.

Role of FWA in each market is shaped by fixed-line broadband landscape

While FWA user experience cannot match fiber or modern cable broadband, its role in the broadband ecosystem is more nuanced than a simple comparison of absolute performance. Its adoption is fueled by lower barriers to entry: installation is often plug-and-play, avoiding technician visits, wall drilling, or lengthy contracts. Many offers are contract-free, giving households more flexibility. These advantages – ease, affordability, and accessibility – underpin its rapid uptake, even in markets where fixed-line still delivers a higher quality of experience.

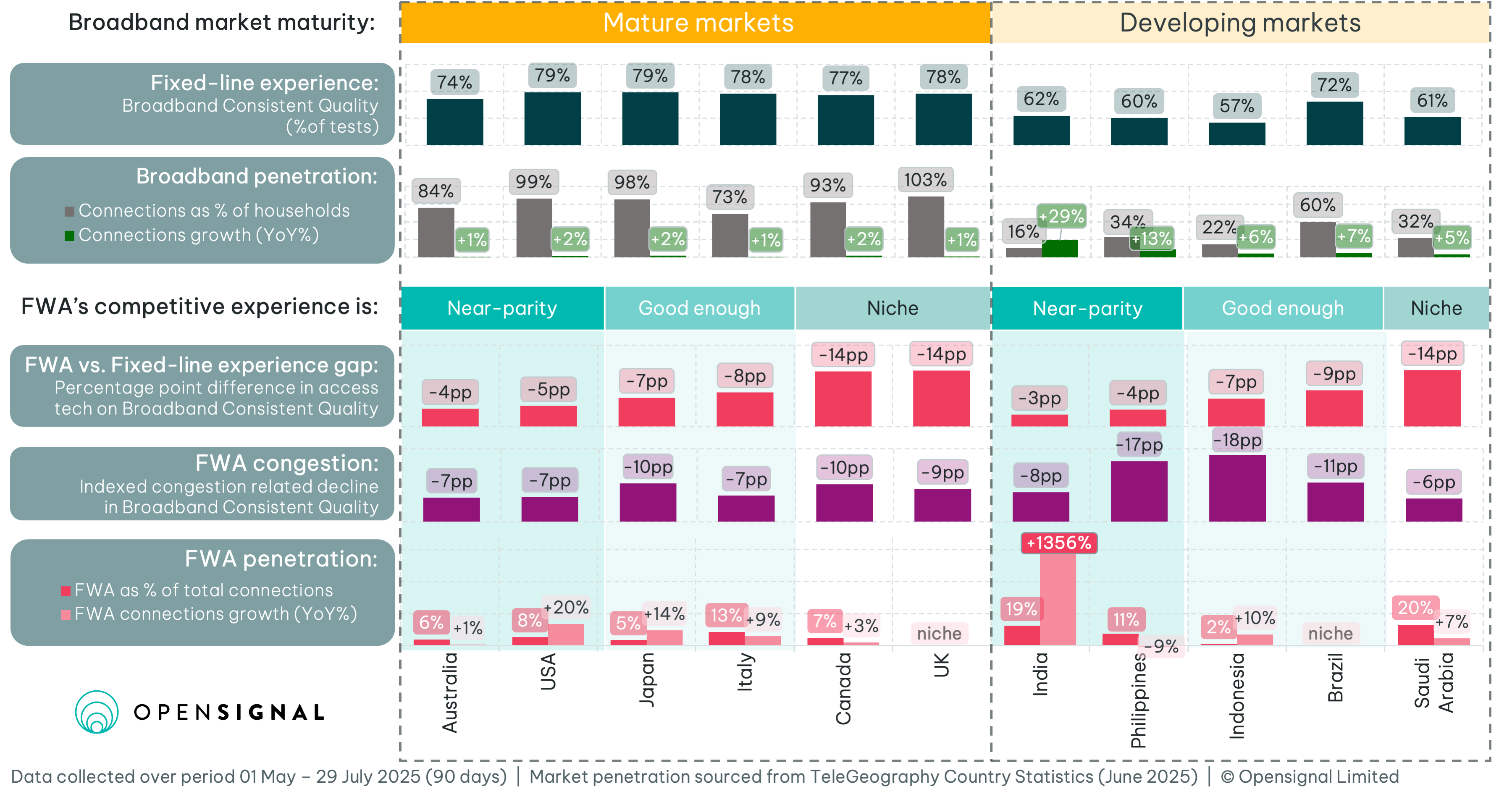

To map FWA’s position across markets, we examine two factors: the maturity of existing broadband infrastructure and the quality gap between FWA and fixed-line connections.

In mature markets, where the level of fixed-line experience and broadband penetration is already high, FWA is emerging as both a competitive disruptor and a niche extender. The competitive position, however, is to a large degree influenced by the scale of the quality gap with fixed-line.

The United States illustrates FWA’s disruptive potential. With FWA delivering experience just 5.1 percentage points below fixed-line, adoption continues to accelerate. In Q2 2025, the three national FWA providers collectively added 935,000 subscribers (including residential and business), while the four largest cable operators – Comcast, Charter, Altice, and Cable One – together lost 414,000 residential broadband customers. Verizon and T-Mobile now serve over 10 million FWA households combined, sustaining growth by actively monitoring network performance and temporarily closing cell sectors to new customers when utilization nears capacity.

Elsewhere in mature markets, FWA plays a more selective role. In Italy, it trails fixed-line by 8.4pp yet still accounts for 13% of broadband lines (according to TeleGeography), mainly in rural and suburban areas where fiber rollout is less viable. Italian FWA provider EOLO is among the very few globally to deploy mmWave-based solutions commercially, while Linkem/Tiscali serves as another specialized fixed wireless service provider. By contrast, TIM and Vodafone position FWA as a way to monetize their 5G networks and offer a substitute where fiber is absent, meeting coverage obligations, through offerings that range from external antennas to low-cost indoor modems.

Australia is a unique case where the three mobile operators offer fixed wireless as a way to differentiate their broadband offers from the low-margin undifferentiated wholesale options available from the NBN (National Broadband Network). Similar to the U.S., operators use availability restrictions and service deprioritization to ensure fixed wireless doesn’t degrade mobile user experience. In Canada, FWA has gained traction as a rural lifeline. Xplore’s “5G Ultra” now delivers 100–500 Mbps to small towns across nine provinces, positioning wireless as a “game changer” for bridging the digital divide.

In the U.K., fixed wireless access (FWA) remains a niche part of the broadband market, according to the national regulator Ofcom, which does not publish an official penetration figure. Ofcom has previously indicated around 400,000 connections (roughly 1% of total broadband lines as of 2024), underscoring its limited footprint compared with fixed-line. This is despite strong promotion by Three, which markets low-cost unlimited 5G home broadband. Across the market there remains a large gap with fixed-line, at -13.8pp, and the dense fiber/cable footprint limits FWA’s role in the market. However, the UK’s upcoming mmWave auction could inject new momentum into fixed wireless by enabling higher-capacity services that compete more directly with fiber.

In developing markets, the broadband landscape is defined by low penetration and subpar experience with the existing fixed-line options. In those markets, FWA is a more competitive alternative to fixed-line regardless of gaps in experience.

In theory, fixed-line in developing markets should have a decisive quality advantage over fixed wireless. Almost all fixed-line access in developing markets is via fiber-to-the-home, as few have widespread DSL networks or subscriber bases. The issue is that operators and their contractors often forsake the security (and cost) of buried infrastructure for the deployment speed (and affordability) of aerial cables. In the Philippines, both Globe Telecom and PLDT have sought to reduce fiber cuts by road crews and construction workers via increased coordination with government agencies. In Indonesia, local governments will sometimes remove aerial cables unilaterally in order to improve the appearance of the streets. And in India, the big ISPs rely on thousands of small Local Cable Operators (LCOs) to deploy and manage last-mile infrastructure. In contrast, fixed wireless relies on physically secured cell sites with power back-up.

In India, a -2.9pp quality gap between fixed-line and FWA is a key part of its competitive success. With household broadband penetration at just 16%, FWA has grown 15-fold year-on-year, capturing 19% of the home broadband market (according to TeleGeography). Reliance Jio’s AirFiber reached 7.4 million subscribers in under a year, the fastest FWA adoption curve globally. Remarkably, low congestion impacts indicate resilient infrastructure, with only an -8.1pp drop in CQ between low- and high-congestion hours, keeping FWA’s expansion curve on track for continued growth.

Other markets tell more mixed stories. The Philippines has one of the smallest gaps in network experience between fixed-line and FWA, but FWA’s share of the home broadband market is declining (–9% YoY). Prepaid 4G home Wi-Fi offers were once transformative, giving millions affordable internet access without contracts. But as fiber expands, operators like Globe and PLDT are now shifting customers to fiber. Still, new entrant DITO continues to push 5G FWA as a disruptive play.

Indonesia, where broadband penetration is just 22% (according to TeleGeography), faces harsher constraints. While Telkomsel’s Orbit service has connected hundreds of thousands of households, severe congestion (–18.3pp CQ drop between off-peak and peak hours) limits scalability.

By contrast, Saudi Arabia has aggressively promoted FWA as a primary broadband channel. The story began with Zain, which, unencumbered by a fiber network, went all-in on 5G FWA, reshaping the market and forcing STC and Mobily to follow. Regulators played their part too. By ensuring generous spectrum allocations and enforcing price parity with fiber, CITC balanced disruption with stability. Despite a –13.9pp quality gap with fixed-line, one in five of all broadband connections today in the Kingdom are now on FWA, making it one of the most advanced FWA markets globally. Saudi Arabia is an exemplary case of how FWA can transform national broadband access, documented in our previous research: The state of Fixed Wireless Access in Saudi Arabia: June 2025.

Conclusion: Where is FWA heading?

FWA is no longer just filling coverage gaps, as in many markets it has entered the near-parity stage, reshaping the competitive landscape and emerging as a genuine substitute for fixed-line options. Elsewhere, the experience still falls short of wireline, but FWA continues to play a vital role in extending access where fixed-line networks remain limited in reach or accessibility.

By leveraging existing mobile infrastructure, operators can deploy FWA rapidly and at lower cost, making it especially valuable in underserved or hard-to-reach areas. Unlike fiber, which requires slow-moving and expensive civil works, FWA availability can be scaled rapidly as long as the network has sufficient capacity.

For consumers, this means simpler installation, faster activation, and competitive pricing that often undercuts fixed alternatives. With experience approaching parity in more markets, these advantages have made FWA a compelling choice in both urban and rural contexts, broadening competition and helping close the digital divide. Evidence from the U.S. and India demonstrates that, with the right spectrum mix and careful capacity management, mobile networks can absorb FWA traffic at scale without compromising mobile user experience. The U.S. is well documented in our earlier report 5G Fixed Wireless Access (FWA) Success in the US.

For operators, the long-term success of FWA depends on active capacity management at both the cell and site level. Sustained growth requires accurate demand forecasting, continuous congestion monitoring, and a careful balance between subscription intake and strategic network investment to maximize utilization.

Contact us if you want to assess the potential of FWA in the context of existing fixed-line networks, drill down to the city level, or benchmark operator performance. Get in touch to learn what we can offer in your market.

Definitions

Broadband Consistent Quality

Broadband Consistent Quality (CQ) measures how often a network, from the perspective of a single device once connectivity is established, meets the requirements for common applications. Broadband Consistent Quality uses six key performance indicators: download and upload throughput, latency, jitter, packet loss, and time to first byte, setting thresholds appropriate for individual rather than multiple device usage. Metrics represent the percentage of users’ tests meeting these performance thresholds to support activities like watching HD video, completing group video calls, and gaming across all hours of the day.

Fixed Wireless Access (FWA) / Fixed-line segmentation

Our segmentation of FWA is limited to services operating on licensed spectrum – namely 4G LTE and 5G – thereby excluding a small share of access, most notably wireless ISPs in Canada and the United States. The experience on fixed-line refers to our users across wired methods of broadband access delivery i.e. Fiber, xDSL, Cable (HFC). Regardless of access technology, our readings are measured when users are connected to home gateways via Wi-Fi.

> Appendix: Additional data cuts

Opensignal Limited retains ownership of this insight including all intellectual property rights, data, content, graphs & analysis. Reports and insights produced by Opensignal Limited may not be quoted, reproduced, distributed, published for any commercial purpose (including use in advertisements or other promotional content) without prior written consent. Journalists are encouraged to quote information included in Opensignal reports and insights provided they include clear source attribution. For more information, contact [email protected].