2025 has brought a major shift in the U.S. Fixed Wireless Access (FWA) market. What was once a two-horse race between T-Mobile and Verizon has now become a three-way contest, as AT&T Internet Air, AT&T's FWA offering, has gained critical mass. For consumers, this means more choice, but it also carries the risk of disappointment if marketing overstates the performance that networks can actually deliver.

Key Findings:

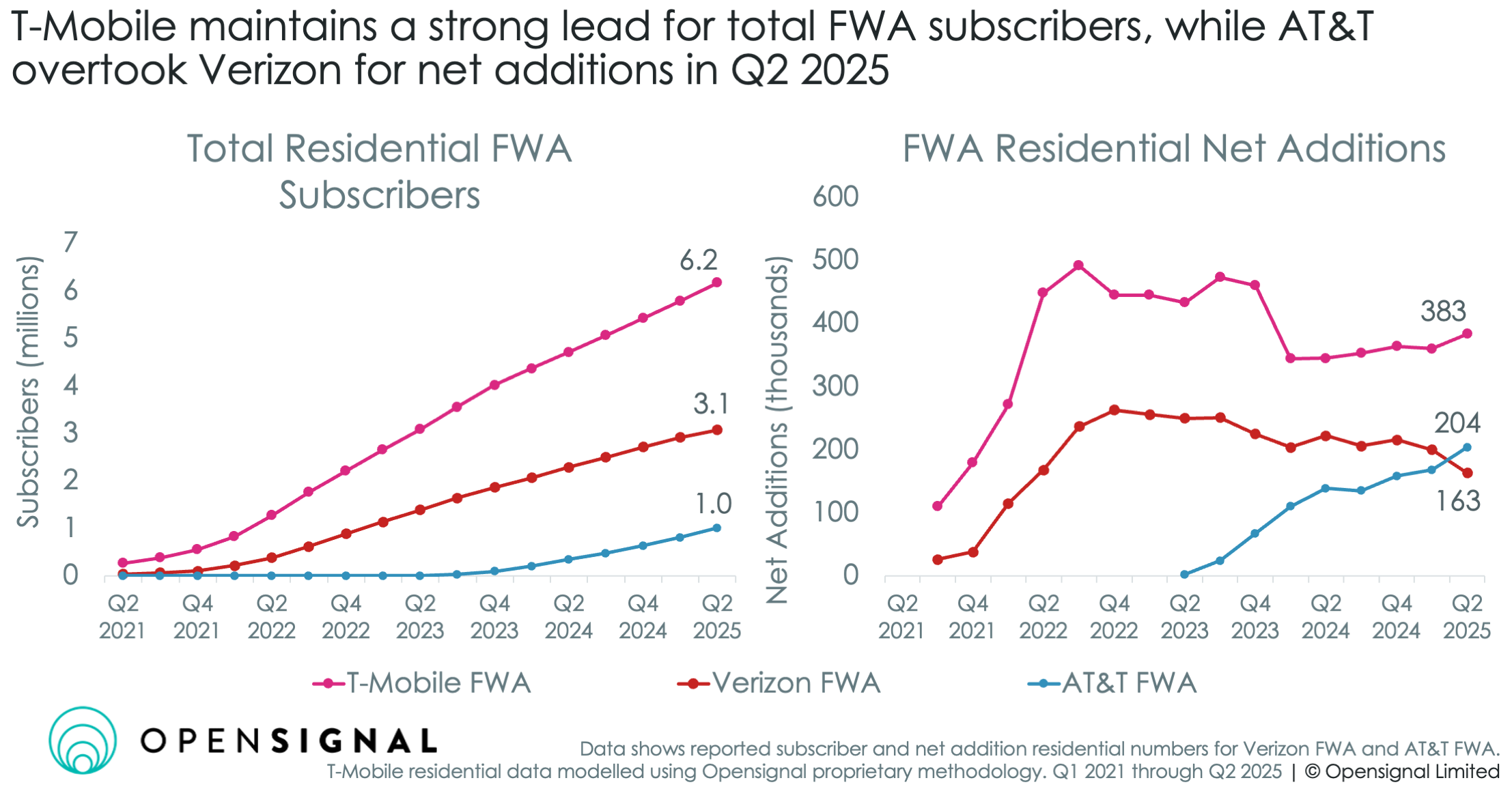

- T-Mobile continues to lead the FWA market in performance and subscribers.

It delivers the strongest network performance and continues to lead the broadband industry in net additions. - The FWA slice of the pie is growing.

Opensignal analysis shows that increased number of FWA options in a market leads to FWA having an increased share of all broadband subscribers. - AT&T Internet Air is moving from a stopgap solution to a core part of its converged strategy

In Q2 2025, AT&T Internet Air net additions outpaced Verizon’s. Leveraging its new EchoStar spectrum holdings, AT&T looks likely to continue expanding its FWA offering over the next few years. FWA providers are now in direct competition for some subscribers.

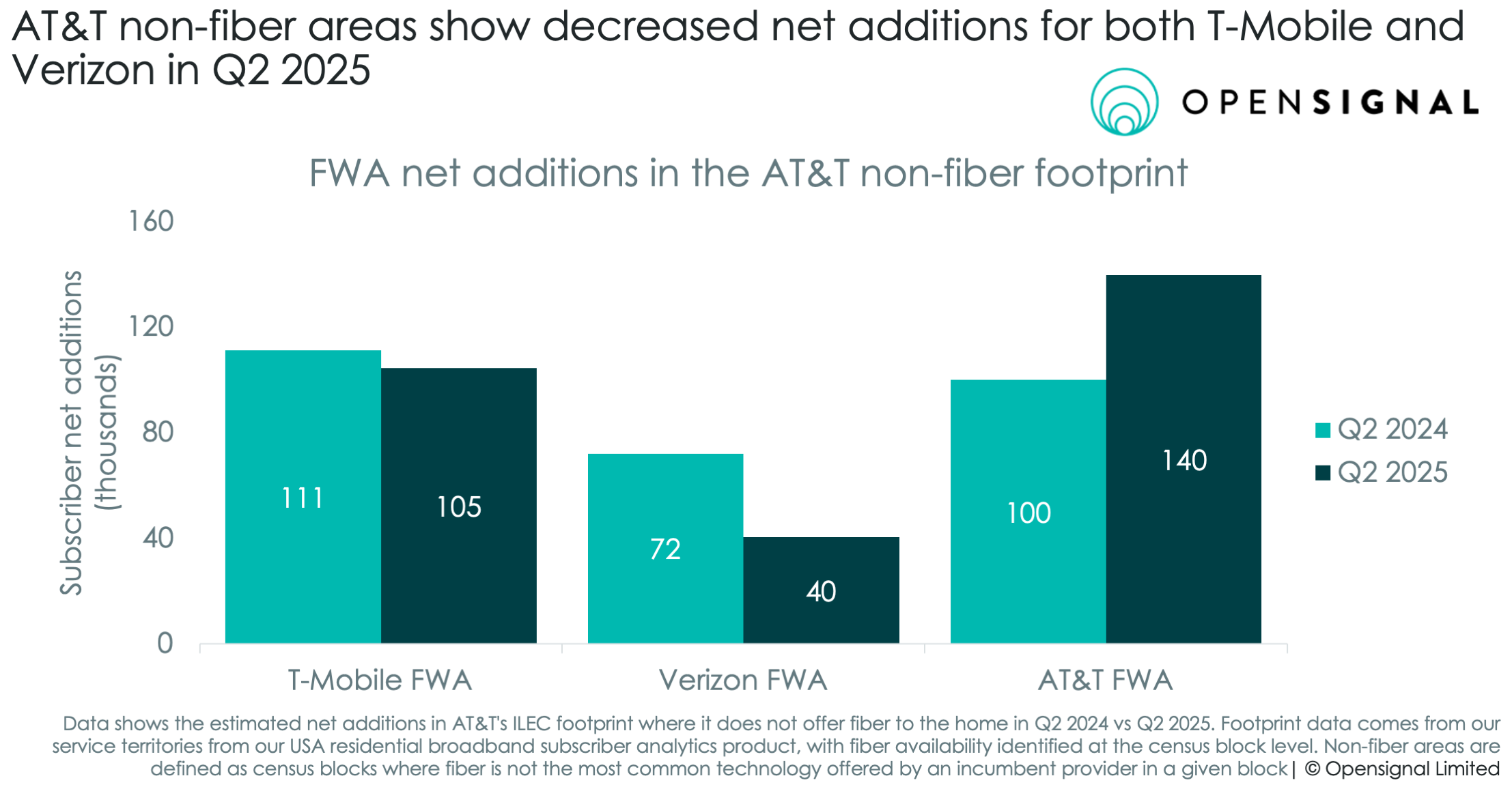

Most FWA subscribers typically come from within each carrier’s mobile subscriber base. However the drop in net additions for both T-Mobile and Verizon in AT&T non-fiber areas following the launch of AT&T Internet Air suggests that there had been direct competition for subscribers churning off of AT&T’s non-fiber service.

When it comes to the quality of experience FWA subscribers get, T-Mobile's FWA service is the clear leader. This can be seen across underlying metrics like download speed, but is best demonstrated by the metrics that speak to overarching user experience — Broadband Consistent Quality and Reliability. Opensignal’s Broadband Consistent Quality metric measures how consistently users have a connection strong enough for everyday tasks — a key indicator of real-world experience that traditional speed tests don’t capture. The results show a clear tiering: T-Mobile leads with 76.8%, while Verizon is second place at 73.4%, and AT&T is third at 59.4%.

To situate these results, T-Mobile and Verizon's FWA both outperform the average Consistent Quality for Fiber to the Node (FTTN - 65.7%) during the same time period. T-Mobile's FWA is closer than Verizon’s to the average we see on cable (81.5%). Meanwhile, AT&T's FWA outperforms DSL (56.0%), but is notably below the FTTN average.

A similar picture emerges for Reliability, which incorporates more strenuous sufficiency thresholds and the challenges of establishing a connection in the first place, to represent the whole household's experience. Here, the differences in performance are starker, and T-Mobile’s lead over second-place Verizon is clear. T-Mobile scores 578 on a 100-1000 scale, compared to 517 for Verizon. Meanwhile, AT&T trails at 379.

Outlining the FWA market

With this strong performance, and its early entry into the market, it is no surprise that T-Mobile remains the largest player with the highest quarterly net additions. AT&T, however, is growing despite its lower performance. In Q2 2025, AT&T achieved the dual milestones of one million total FWA customers and 204,000 net additions — making it the first quarter where AT&T FWA net additions outpaced Verizon’s. This is a significant change from our last deep dive back in 2024, where we included only T-Mobile and Verizon.

AT&T’s growth — why now?

As recently as its Q2 2025 earnings call in July, AT&T’s leadership referred to its FWA service as a temporary measure for areas where it “intend[s] to offer fiber in the future”.

Its most recent uptick in net additions reflects a realization from AT&T that its broadband subscriber base would be declining without FWA. Since Q2 2023, the first quarter it reported AT&T Internet Air net additions, AT&T’s total residential subscriber base has grown from 13.9 million to 14.3 million — but would have declined by over 600,000 if not for AT&T Internet Air. This is in spite of newly passing nearly 5 million homes with fiber in that time, and adding more than 2 million fiber subscribers. But fiber gains are not keeping pace with non-fiber losses. Since 2022, AT&T’s non-fiber customer base has dropped by over 50%, from 7.5 million at the end of Q2 2022, down to just short of 3.5 million for Q2 2025.

In light of this, it seems AT&T’s strategy has changed. Building on its recent successes growing net additions for AT&T Internet Air, its $23 billion acquisition of ~50 MHz of nationwide spectrum from EchoStar suggests it is targeting a near nationwide FWA offering. Most useful to this will be the ~30 MHz of mid-band 3.45GHz spectrum, which has been a critical enabler of FWA globally. Undoubtedly, this should raise AT&T's FWA performance thanks to the additional capacity. This likely reflects an acceptance that AT&T is unlikely to reach all of its customer base with fiber in the near to mid-term future. FWA offers faster deployments across far greater areas, supporting both those areas where fiber will (eventually) come, and where it won’t — while also allowing AT&T to offer a converged solution in the more than half of the country where AT&T is not the incumbent telco.

More FWA providers grows the FWA slice of the pie — but also creates head to head contests

As AT&T prepares for near-nationwide FWA and the increased competition that this brings, this puts the U.S. fixed broadband industry in uncharted territory. In Opensignal’s FWA footprint data, 48% of US housing units have access to two or more FWA providers — and just 13% have access to all three. With the increasing reach and capacity of AT&T's FWA service, it is likely these figures will increase.

Looking at market share in current markets with one, two or three FWA providers reveals two clear trends:

- Category expansion: In areas with more FWA providers, a greater share of total broadband goes to FWA, indicating that multi-provider presence grows the FWA category. This makes sense, given the majority of FWA subscribers are typically sourced from within the operator’s mobile subscriber base. These subscribers would then be non-competitive between the three FWA providers, but instead cause challenges for providers using other access technologies like cable.

- Stronger competition within FWA: In single-provider markets, we see an average of a 7.2% market share. At two, share expands to 10.7%, and at three, 13.4%. This shows that extra players may lead to increased total FWA penetration, but diminishing returns for each individual provider, likely due to increased competition for the same subscribers.

AT&T’s change drives headwinds for Verizon, but has limited impact on T-Mobile

This stronger competition is borne out when comparing net additions for Verizon and T-Mobile in the areas most impacted by AT&T Internet Air — AT&T’s non-fiber footprint.

Both Verizon and T-Mobile see a decrease in net additions within the AT&T non-fiber footprint, but Verizon’s decrease is more severe. It saw nearly 32 thousand fewer net additions in the AT&T non-fiber footprint in Q2 2025 compared to Q2 2024 — over a 40% reduction year on year. This drop in net additions was also more than what we see outside of AT&T’s non-fiber footprint, despite the fact that the AT&T non-fiber footprint only accounts for approximately 25% of US homes. T-Mobile, meanwhile, saw over six thousand fewer net additions in these areas, but more than makes up the difference outside AT&T’s non-fiber footprint.

Until recently, both Verizon and T-Mobile benefited from AT&T’s non-fiber decline by capturing subscribers leaving AT&T’s legacy DSL service. Many of these were likely T-Mobile or Verizon mobile customers who had relied on AT&T for home broadband. Others left AT&T’s non-fiber offering looking for an alternative provider — either for better performance or lower prices — and ended up with Verizon or T-Mobile FWA. With the launch of AT&T Internet Air, however, that dynamic has shifted. AT&T is now retaining a greater share of these households.

Implications & Outlook

The rise of AT&T Internet Air intensifies competition across the broadband market. AT&T’s acquisition of EchoStar spectrum will allow AT&T to increase its capacity, and hopefully improve its performance in the areas it covers with FWA. This rollout likely continues to focus on the areas where it intends to offer fiber, as well as those with customers relying on legacy AT&T copper-based services in the short to medium term. It can then expand outside of its incumbent telco footprint to broaden its convergence strategy across its entire mobile subscriber base.

The key question now is how each provider will implement a combined FWA and fiber strategy — and which of these strategies will prove most effective in attracting and retaining subscribers. Can AT&T’s new spectrum deliver an experience closer to Verizon and T-Mobile? Will Verizon lean harder on FWA as it integrates Frontier, or focus its attention on fiber? And how long before T-Mobile starts to pivot more visibly toward its fiber bets like its joint ventures to buy Metronet, Lumos and U.S. Internet?

FWA is no longer an experiment — but its exact role in converged operator strategies is still being defined. Opensignal will continue to track these shifts in real-world user experience and market dynamics, helping operators, investors, and regulators understand the true impact of FWA. To keep abreast of the latest developments in the U.S. fixed broadband market, read our recent research here, or subscribe to our newsletter to keep up to date with our latest reports.

Opensignal Limited retains ownership of this insight including all intellectual property rights, data, content, graphs & analysis. Reports and insights produced by Opensignal Limited may not be quoted, reproduced, distributed, published for any commercial purpose (including use in advertisements or other promotional content) without prior written consent. Journalists are encouraged to quote information included in Opensignal reports and insights provided they include clear source attribution. For more information, contact [email protected].