By Burhan Kamal – VP, Client Analytics & Insights for MEIA and Sylwia Kechiche – VP, Industry Analysis

India’s telecom market in early 2026 is entering a more mature phase — increasingly shaped by experience led differentiation rather than price disruption.

Following tariff adjustments and continued regulatory focus on user-measured performance, operators are evolving their strategies. While national trends still remain important, Opensignal’s data shows that competitive advantage is now increasingly determined at the local level.

At a national scale, Reliance Jio continues to lead. With more than 500 million subscribers and over 43% of the sector's Adjusted Gross Revenue (AGR), its 5G standalone deployment is shaping both market structure and India’s position in Opensignal’s Global Network Excellence Index, where it ranks 15th among large landmass markets. Jio also leads on Consistent Quality (CQ) in 58 out of 63 metro areas.

However, national leadership alone does not explain competitive outcomes.

BSNL is gaining subscribers through lower-priced plans despite weaker CQ. Airtel continues to attract higher-value users through premiumization. Vodafone Idea (Vi) is focusing investment on defending key markets.

To understand how these strategies translate into results, we look beyond national averages, using Opensignal’s Subscriber Analytics to analyse how network performance is driving customer acquisition and retention.

Key takeaways

- Competitive advantage is increasingly local, not national. Metro-level Consistent Quality (CQ) better explains subscriber gains and losses than national metrics.

- Operators win where network experience and commercial strategy align. Targeted CAPEX and localized CVM create defensible “urban fortresses” that sustain market share.

- Network superiority must be visible at the point of sale. Performance only drives growth when it is clearly demonstrated to consumers in specific locations.

From national competition to local advantage

Opensignal’s metro-level analysis — comparing Consistent Quality (CQ) with local market share — shows a clear pattern.

Operators outperform where strong network experience is reinforced by localized commercial execution.

We describe this as the Urban Fortress strategy: building defensible positions in specific cities or regions by aligning network performance, investment and customer strategy.

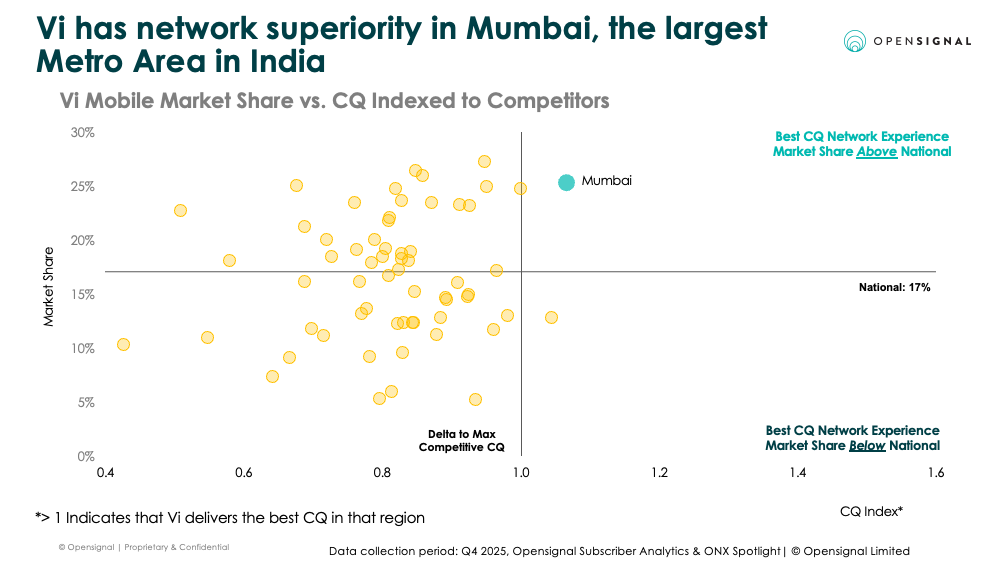

Vi in Mumbai: Local strength despite national pressure

At a national level, Vi has experienced subscriber losses — Opensignal Subscriber Analytics shows Jio accounted for 59% of Vi’s net losses in 4Q25.

However, this trend does not hold in Mumbai.

In India’s largest and most valuable metro area, Vi maintains a strong position. This reflects a clear alignment between network performance, investment and commercial execution.

Vi’s massive ₹45,000 crore ($4.5bn) CAPEX plan targets 17 priority circles, including Maharashtra, while its localized CVM (Customer Value Management) strategy focuses on Below-The-Line (BTL) offers and digital bundles tailored to the region.

Rather than competing through national price reductions, Vi reinforces its position through targeted, location-specific propositions — helping limit exposure to broader churn dynamics.

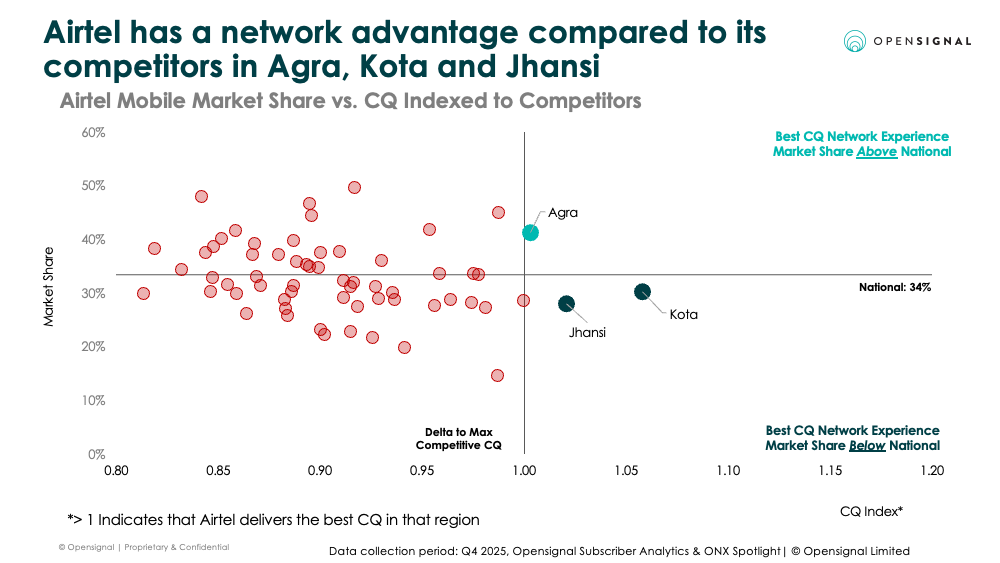

Airtel: Enabling premiumization through regional performance

Airtel shows a similar pattern.

According to Opensignal Subscriber Analytics platform, nationally, Airtel has increased its market share by around 1 percentage point since early 2024, with 73% of gains coming from Jio — indicating direct competitive switching.

However, these gains are not uniform.

Airtel performs particularly strongly in regional cities such as Agra, Kota and Jhansi, where network experience supports its premium positioning.

This is underpinned by sustained investment, with quarterly CAPEX routinely exceeding ₹11,000 (US$ 1.3bn) crore, alongside targeted deployment in specific regions. In these markets, improved network experience enables Airtel’s premium strategy e.g., the "Airtel Black" converged plans to translate into measurable gains.

The importance of the point of sale

The recent tariff adjustments mark a clear shift: price-led acquisition is no longer the primary growth driver.

Instead, performance and perception at the local level are becoming more important.

Even where operators lead on network experience, this advantage must be visible and credible at the point of sale — across both retail and digital channels.

Solutions such as Opensignal’s Frontline Network Experience (FNX) enable operators to demonstrate independently verified, location-specific performance — helping convert network strength into commercial outcomes.

The Power of the relative claim

In our experience working with operators, being the undisputed CQ leader in a metro provides a strong marketing advantage. However, the greater commercial opportunity often lies in the relative performance claim.

Through the lens of FNX, an operator doesn't necessarily need to rank first in the entire city to drive acquisition. They simply need to be measurably better than the market share leader. Where the incumbent underperforms on quality, even by a small margin, this creates a clear opportunity to target high-value switchers.

FNX enables frontline teams to move beyond broad claims of “best network” and instead demonstrate a more relevant message: “better than your current provider” — a localized and more effective proposition at the point of sale.

The Playbook for localized growth

In the competitive landscape of 2026, the era of the “one size fits all” national strategy has ended. As the Indian market continues to mature, the operators that succeed will be those that treat network experience not just as an engineering goal, but as a precision instrument for growth.

To win in this environment, leadership must execute on three critical fronts:

- Master local positioning: Success begins with a granular understanding of where you stand in every metro. National averages mask the “Urban Fortresses” where an operator holds a clear advantage, and the vulnerable metros where they are at risk.

- Leverage network experience to win: At Opensignal we help operators identify the right toolkit to equip them with to win market share. In markets where an operator holds the CQ edge, they must lead with network-driven acquisition. In markets where they trail, they must use aggressive BTL offers or value based retention.

- Communicate with precision: It is not enough to have a network advantage; that advantage must be visible at the point of sale. By utilising verified, 3rd part data through solutions like FNX, operators can give their retail and digital teams the tools to prove their superiority over the incumbent in real time, converting “value seekers” into "quality loyalists”

Ultimately, the goal is to provide operators with the tools to identify how to win in any given circle. Whether the lever is network, price, or service, the foundation of the decision remains the same: a hyper-local, data-driven view of the truth.

To understand where local network performance translates into commercial advantage — and how to act on it — contact Opensignal to learn more about our Subscriber Analytics and Frontline Network Experience solutions.

To explore these dynamics further, including how 5G is shaping real-world experience and competition across India, read our latest insights:

- India Mobile Network Experience Report (February 2026)

- 5G experience in India: from rollout to real-world impact

These analyses provide a detailed view of how network performance, coverage and user experience are evolving across operators and regions in India

Methodology note

Opensignal Subscriber Analytics metrics assess market share and flow share (i.e., competitive switching). These metrics are used to monitor and measure subscriber movements between all players in the market. They answer what is happening in the industry and are most often used to inform both reactive and proactive decision-making.

We calculate market performance metrics from our first-party dataset of automated device tests. Data — including provider, network type, location, and device details — is aggregated and calibrated to accurately reflect performance outcomes.

Metric Definitions:

Market Share: A carrier’s total subscribers as a percentage of all subscribers in the market

Consistent Quality (CQ): Quality calculation providing an indication of customer experience for high performance activities such as live HD video streaming

CQ Index: Carrier CQ / Strongest Competitor CQ

Opensignal Limited retains ownership of this insight including all intellectual property rights, data, content, graphs & analysis. Reports and insights produced by Opensignal Limited may not be quoted, reproduced, distributed, published for any commercial purpose (including use in advertisements or other promotional content) without prior written consent. Journalists are encouraged to quote information included in Opensignal reports and insights provided they include clear source attribution. For more information, contact [email protected].