Authored by Robert Wyrzykowski, data support by Bill Murphy

For decades, satellite internet in rural areas was a reluctant compromise — a high-latency, high-cost last resort for those beyond the reach of wired infrastructure like fiber, cable or xDSL. However, by early 2026, this dynamic has changed. Starlink is no longer merely filling gaps in broadband availability; it is showing rural users that they no longer have to settle for unreliable, expensive service — effectively challenging the regional monopolies once held by incumbent ISPs. In the United Kingdom, it is now often cheaper to secure a Starlink subscription than the lowest-priced plans from the national incumbent, BT.

With plan prices dropping and hardware costs reduced, Starlink is no longer just a luxury for second homes. In less than two years, the service has transformed from a niche alternative to a mainstream disruptor. Starlink doubled its customer base in 2025 — surging from 4.5 million to 9 million subscribers, adding roughly 20,000 new users a day on average in November and December 2025. And the momentum shows no signs of slowing, as Starlink passed the 10 million mark in February 2026, adding another million subscriptions in less than two months.

Key Findings:

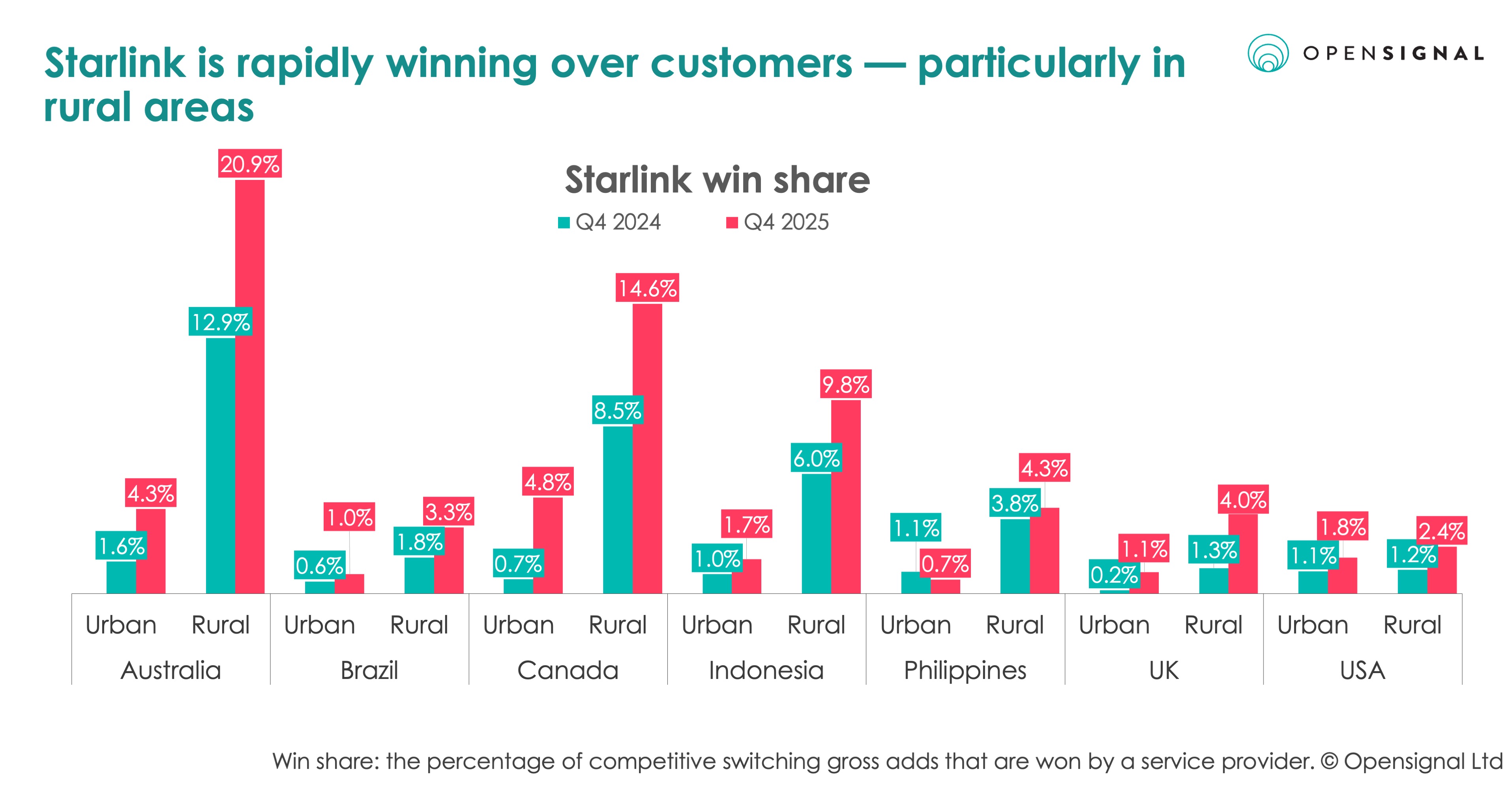

- Winning the fixed broadband switchers: Our switching data shows that Starlink’s win share of customers switching ISPs grew across major markets throughout 2025, with particularly high shares in rural Australia and Canada.

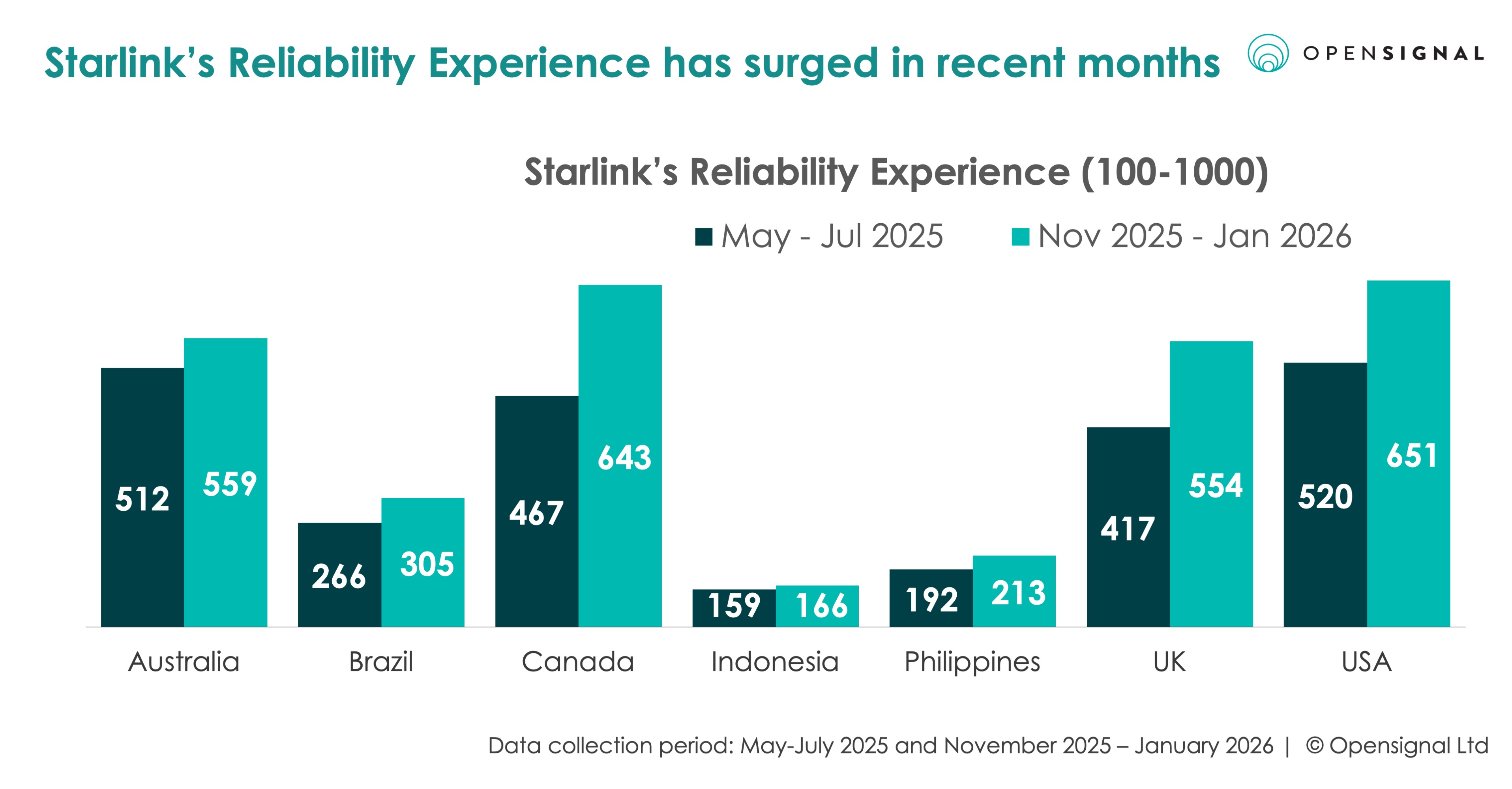

- A major boost in reliability: The rollout of V2 Mini satellites and Inter-Satellite Links (ISL) has pushed network capacity past 600 Tbps. This has helped Starlink’s Reliability Experience scores surge by more than 30% in Canada and the UK, and over 25% in the U.S.

- Price reductions drive expansion: In more mature markets, Starlink has lowered monthly fees and offered free kit rentals — driving big customer gains in North America, Europe, and Oceania.

- High barriers, higher demand: Affordability remains a hurdle in emerging markets, yet despite hardware costs and demand surcharges that represent a massive portion of local income, Starlink frequently sells out its available capacity. This robust demand gives Starlink little reason to cut prices in regions where they are already struggling to keep up with the waitlists.

- Operational risk: Despite its lead, Starlink faces increasing structural risks, particularly regarding launch dependency on SpaceX’s Starship schedule and mounting regulatory pressure concerning orbital crowding.

Table of Contents:

Winning big in rural areas

Conventional wisdom suggests that in developed markets, Starlink is a luxury for secondary or summer homes — a complementary service for wealthy customers who have access to wired fixed broadband at their primary urban residence. However, Opensignal Subscriber Analytics show that users are increasingly churning from traditional ISPs to make Starlink their primary gateway. Essentially, Starlink is winning wherever the prohibitive cost of building physical networks has left traditional providers unable to offer a competitive alternative.

In Australia, one out of every five rural households that switched internet providers last year chose Starlink. Canada shows a similar surge in rural win share. However, this momentum is not confined to the countryside; urban areas are also seeing a steady rise in adoption. The broader catalyst for growth is Starlink's evolution into a mass-market competitor. Much like Fixed Wireless Access (FWA), it is pivoting from a niche rural solution to a value-driven alternative for urban and suburban households as well.

The profile of these switchers is also fundamentally changing. According to Opensignal data, Starlink’s "win composition" in the U.S. has evolved from capturing mostly legacy telco and satellite users to increasingly pulling customers away from cable providers — particularly among those who are not moving homes. This shift suggests that Starlink is increasingly being chosen as a primary connection choice rather than a situational necessity for relocation.

In emerging markets like Brazil and Indonesia, Starlink is capturing significant win share by moving the infrastructure to the sky. This reflects a clear cause-and-effect: Starlink fills the gap where the upfront capital for terrestrial rollouts fails to pencil out for traditional ISPs. While fiber’s marginal costs are remarkably low once a home is connected, the prohibitive expense of reaching remote households remains the primary barrier—one Starlink bypasses with its plug-and-play model.

This global momentum is no accident; it is the result of three interlocking forces working in tandem: a major leap in service quality, aggressive pricing in developed markets, and a strategic push to capture high-demand, underserved areas in emerging markets, where terrestrial options have failed to scale.

The boost in reliability of services

In the seven markets we studied for this analysis, Opensignal observed a substantial increase in Reliability Experience — a metric measuring a household’s ability to complete uninterrupted tasks like video conferencing or gaming. These scores improved by more than 30% in Canada and the UK and by 25% in the U.S. within the second half of 2025. In the US, their Reliability score now is at least as good as fixed wireless reliability.

Our Opensignal Network Experience (ONX) fixed broadband data shows that a substantial reduction in packet loss was the primary driver of these Reliability Experience gains. This technical shift is likely the direct result of a massive hardware overhaul that Starlink confirmed in its reports. By early 2026, the rollout of V2 Mini satellites — boasting four times the capacity of Gen 1 models — pushed total network capacity past 600 Tbps, boosting both speed and reliability. This is complemented by Inter-Satellite Links (ISL), which allow satellites to communicate directly. By bypassing ground station “bounces”, ISL lowers latency and extends coverage to remote regions lacking ground infrastructure.

Further gains come from over 650 "Direct to Cell" satellites deployed as of early 2026. While mobile-centric, their advanced phased array antennas and custom SpaceX silicon have been integrated network-wide. This optimizes beam management, driving a 100-fold capacity increase over the first-generation constellation. Also, Starlink has expanded the number of its ground stations — to over 100 in the U.S. alone — and refined its handover software to virtually eliminate the "micro-drops" that impact the quality of satellite connections.

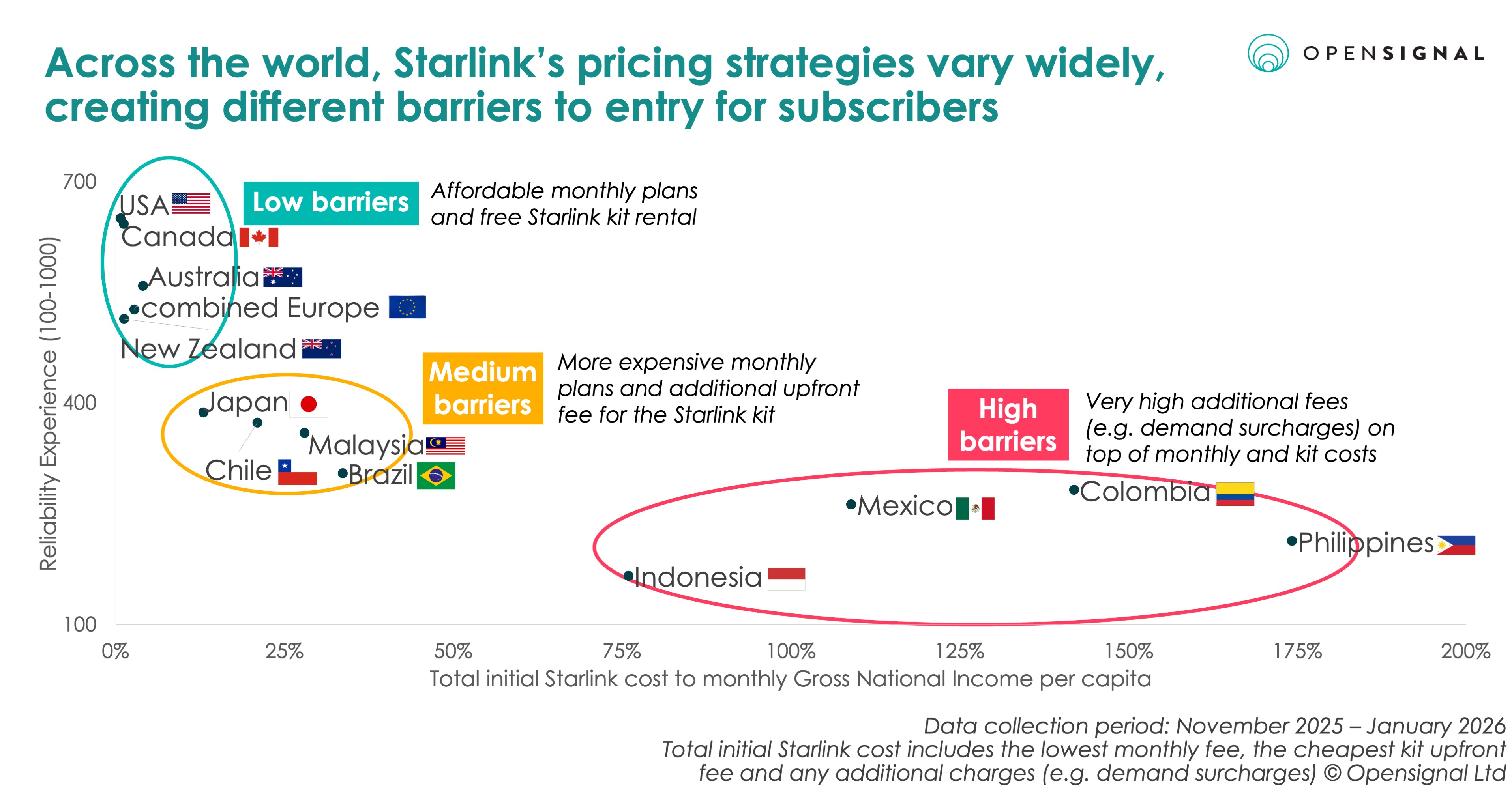

The two-track pricing strategy

Starlink’s pricing is a calculated two-track strategy designed to optimize for market maturity and capacity availability.

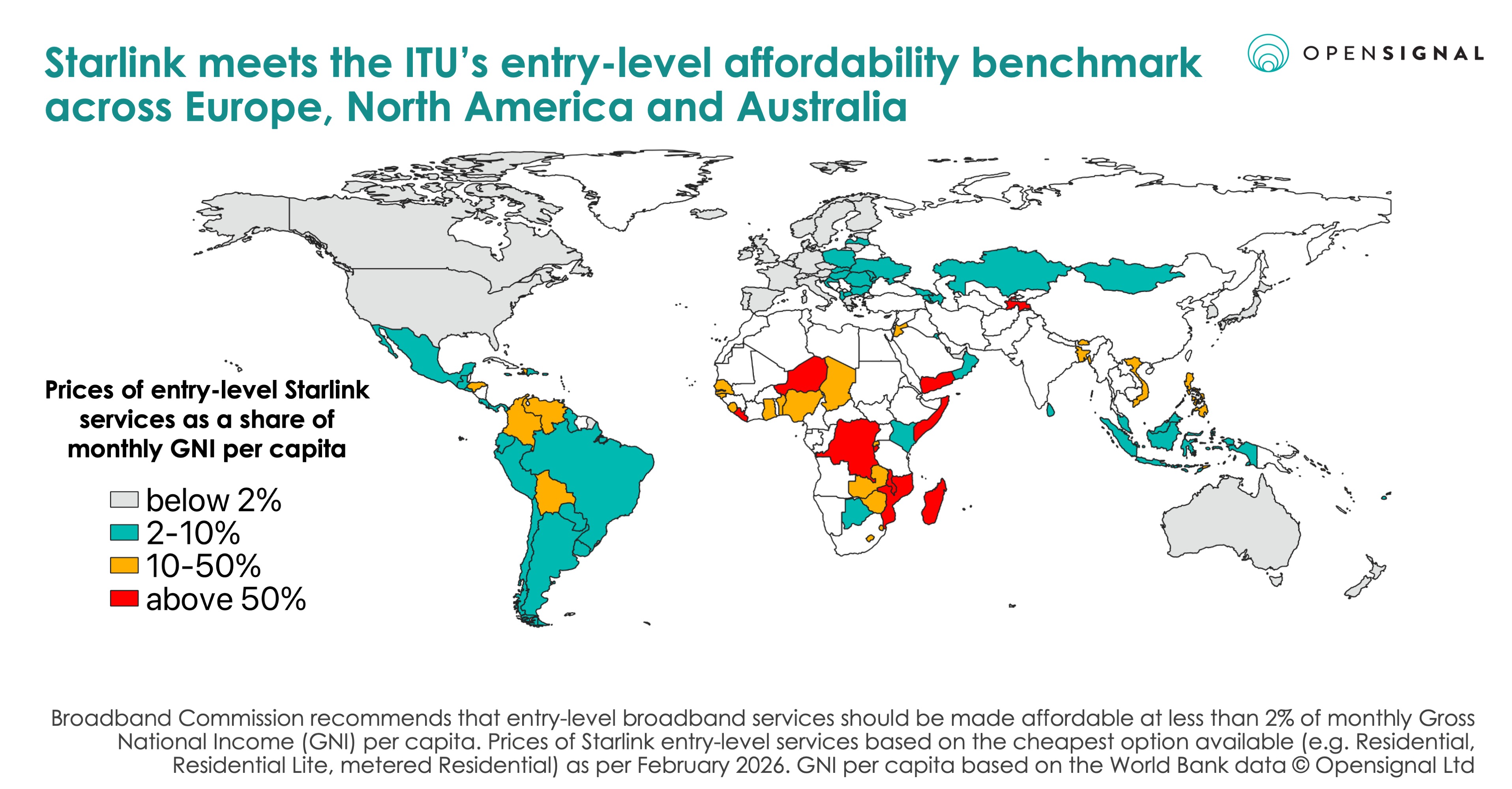

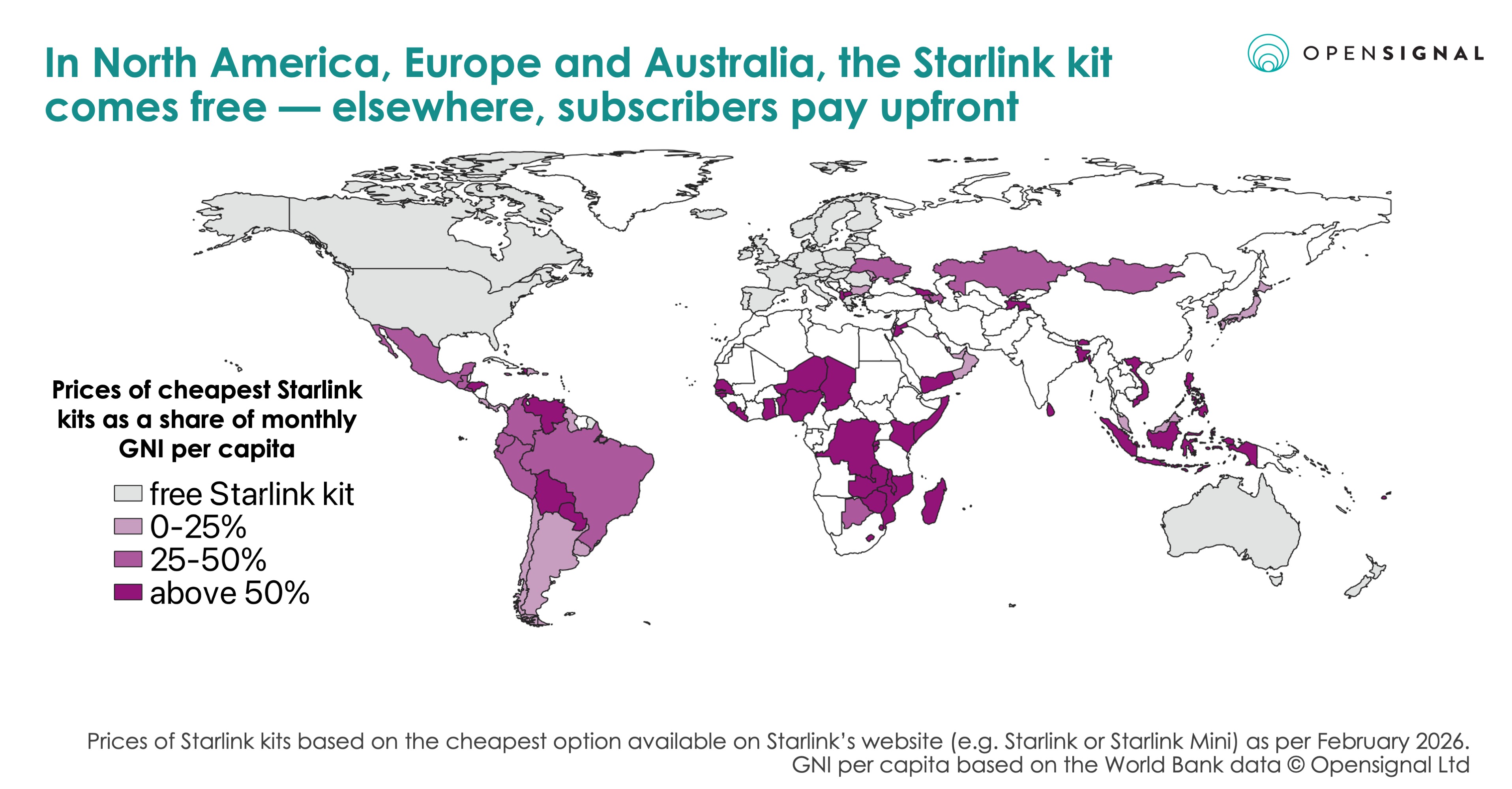

- Saturated market disruption: In North America and Europe, Starlink is pricing as an aggressor. By reducing monthly fees and introducing free Starlink kit rentals, it has brought costs below 2% of monthly GNI per capita for its entry-level propositions — the ITU threshold for broadband affordability. In rural areas of markets like the UK, North America, and Oceania, Starlink now offers budget-friendly metered options with speed limits of 100 and 200 Mbps.

- Emerging market value capture: Conversely, in regions like Nigeria, the Philippines, and Indonesia, demand is so robust that the service frequently sells out. Here, Starlink maintains a premium pricing tier, bolstered by "demand surcharges" to manage network congestion. Even the "Residential Lite" plan — a deprioritized, lower-cost tier — frequently exceeds the 2% GNI per capita affordability threshold — and customers need to pay for their Starlink kits (although some markets have introduced instalment plans) With long waiting lists and a lack of viable alternatives — such as well-developed 5G FWA services — Starlink has little incentive to lower entry barriers in regions where it is already operating at peak capacity.

While users in Low-and-Middle-Income Countries (LMICs) often pay a significantly higher percentage of their income for entry-level Starlink services, they frequently experience objectively lower reliability. This gap is driven by several critical factors. First is the infrastructure bottleneck: many LMICs lack a sufficient density of "gateways"—the ground stations that connect satellites to the fiber backbone. Second is the environmental challenge: tropical rainfall and intense monsoons in equatorial regions cause "rain fade" where water droplets scatter the Ku-band signal.

Local market conditions further strain service reliability. In many regions, soaring demand frequently overwhelms local satellite capacity, leading to congestion during peak hours. Reliability is also impacted by the way Starlink is deployed in these markets — often as a shared resource for public hotspots in community centres, like in Indonesia. This creates a hardware mismatch where the advanced throughput of a Starlink dish is throttled by the 'last-meter' reality of congested local Wi-Fi and the older mobile devices used by the broader community.

Finally, because entry costs are already high, many subscribers opt for self-installation to save on fees — or simply because professional installation services are unavailable locally. This often results in suboptimal dish placement; even minor obstructions, such as overhanging trees or roof lines, can cause frequent and avoidable "micro-drops" in connectivity.

The sky is no longer the limit

Starlink is currently riding a wave of unprecedented momentum. Looking ahead, the company is set to enter untapped markets like India and finalize partnerships with mobile giants like Deutsche Telekom to launch satellite-to-cell services.

Technical optimization is also accelerating. In early 2026, Starlink began lowering the orbit of approximately 4,400 satellites from 550 km to 480 km. While primarily a safety maneuver to ensure faster de-orbiting, this move triggers a 'virtuous cycle' for network capacity. By operating at a lower altitude, each satellite's signal footprint becomes more concentrated. This reduction in beam diameter means fewer users compete for the same satellite's capacity at any given time — leading to more consistent speeds and reduced congestion across the network, effectively prepping the orbital shells for the massive throughput of the upcoming Starlink V3 fleet. Designed for deployment via Starship, the V3 satellites are expected to offer a massive increase in bandwidth, and this denser orbital configuration ensures the ground network can actually absorb that capacity in high-demand areas.

The rise of a viable orbital broadband layer has profound implications for the traditional telecom ecosystem:

- National incumbents: Legacy operators are losing their rural revenues As Starlink undercuts their pricing, these incumbents face a difficult choice: write off rural infrastructure investments or pivot to hybrid satellite-terrestrial models.

- Public broadband subsidies: Governments are increasingly re-evaluating multi-billion-dollar fiber-to-the-home subsidies in favor of more cost-effective alternatives. Funding expensive rural trenching projects is becoming harder to justify when orbital connectivity can provide comparable speeds at a fraction of the public cost. This shift is most evident in the recent restructuring of the Broadband Equity, Access, and Deployment (BEAD) program. The move from a "fiber-priority" mandate to a "technology-neutral" strategy allows satellite providers like Starlink to compete directly for funding in regions where laying down infrastructure is no longer the most efficient use of taxpayer dollars.

- Fiber overbuilders: Small-to-medium fiber deployments in underserved areas now face an overbuild risk from above. Starlink can enter a market instantly, whereas fiber takes years to permit and lay, potentially siphoning off the customer base before the first cable is even buried.

- Mobile/FWA operators: Fixed Wireless Access (FWA) providers, once the primary alternative to fiber, are losing their competitive edge as Starlink’s V2 Mini satellites improve the latency and reliability that once favored 5G-based solutions.

We are witnessing a new "space race" — only this time, the finish line isn't the Moon, but the customer on the ground. This shift is headlined by Amazon Leo (formerly Project Kuiper), which is leveraging Amazon’s logistical ecosystem and AWS integration to bridge the gap. While Starlink maintains a commanding lead in satellite count, Amazon is strategically targeting the enterprise and government sectors, utilizing its existing relationship with millions of Prime households to aggressively lower customer acquisition costs. Similarly, legacy players like Viasat and Eutelsat OneWeb are pivoting toward a multi-orbit strategy; Viasat’s plan to expand its constellation to 2,800 satellites aims to synthesize the high-throughput capacity of Geostationary (GEO) orbits with the low-latency advantages of LEO.

However, Starlink’s dominance is subject to significant structural friction, most notably its absolute launch dependency. While this creates a capacity cap tied to SpaceX’s internal manifest, it also highlights a broader industry vulnerability: competing LEO providers like Amazon Leo or OneWeb are equally dependent on SpaceX for affordable orbital access. In this environment, any programmatic delay in Falcon 9 or Starship missions wouldn't just stall Starlink—it would effectively paralyze its competitors, who lack a comparably priced, high-cadence alternative for heavy-lift rocketry.

Beyond launch logistics, the competition has shifted toward capital intensity and regulatory gatekeeping. Rivals are increasingly utilizing international bodies to challenge SpaceX’s orbital shell assignments, citing "orbital crowding" and light pollution as grounds for intervention. As active satellites in LEO approach the tens of thousands, the rising probability of "conjunction events" necessitates frequent, autonomous debris-avoidance maneuvers. These maneuvers consume vital onboard fuel, effectively shortening a satellite's operational lifespan and increasing the long-term capital burden of constellation maintenance. Finally, Starlink’s mission to bridge the digital divide faces a geopolitical bottleneck. As the operator seeks to enter untapped markets, it is encountering localized scrutiny.

Ultimately, satellite providers are no longer just participating in the broadband market; they are rewriting its rules. For these disruptors, the sky is no longer a limit — it is a competitive advantage. Tracking how subscriber adoption evolves over time will be critical for ISPs looking to understand this shift and respond effectively to a rapidly emerging competitive landscape.

Read our previous insights on Starlink experience in Canada or Indonesia. If you're interested in more of our tailored analysis on network performance, subscriber analytics or pricing data, please contact us. Don’t forget to subscribe to Opensignal’s newsletter.

Additional charts

Opensignal Limited retains ownership of this insight including all intellectual property rights, data, content, graphs & analysis. Reports and insights produced by Opensignal Limited may not be quoted, reproduced, distributed, published for any commercial purpose (including use in advertisements or other promotional content) without prior written consent. Journalists are encouraged to quote information included in Opensignal reports and insights provided they include clear source attribution. For more information, contact [email protected].