Webinar: We have complemented this report with an in-depth webinar discussion featuring Micah Sachs, Andrey Popov and Simon Lumb of Opensignal, Martin Scott of Analysys Mason, and Domenico Dichiarante of Italy’s Open Fiber.

Watch or listen to the on-demand recording here

Europe’s broadband market is entering a new phase in its fiber transition. In a number of markets, fiber coverage has far outpaced take-up, shifting the industry conversation away from how to accelerate deployment and towards how operators can migrate customers to fiber and accelerate return on investment. At the same time, last-mile infrastructure is only part of the story. The battleground for reliable connectivity is moving increasingly inside the home, where Wi-Fi frequently forms the real bottleneck for meaningfully improving the user experience.

In this report, we examine 18 European markets, including the UK and Turkey, assessing the region’s broadband infrastructure in the context of industry discussion at the FTTH Council Europe Conference held in London in April 2026. By bringing together infrastructure progress and Opensignal’s proprietary insights into real-world user experience, we assess how close European markets are to realising fibre’s promise of flawless connectivity, and why the next stage depends on what happens inside the home.

Key Findings:

- Europe’s fiber adoption bottleneck is now activation, not buildout. Across the EU27+UK, FTTH/B (fiber-to-the-home/-building) rollout efforts have only translated into take-up of 54.9% among homes passed, as of September 2025, showing that the main challenge is now about how to effectively convert the existing footprint into active lines. This theme dominated the discussion at the FTTH Council Europe Conference.

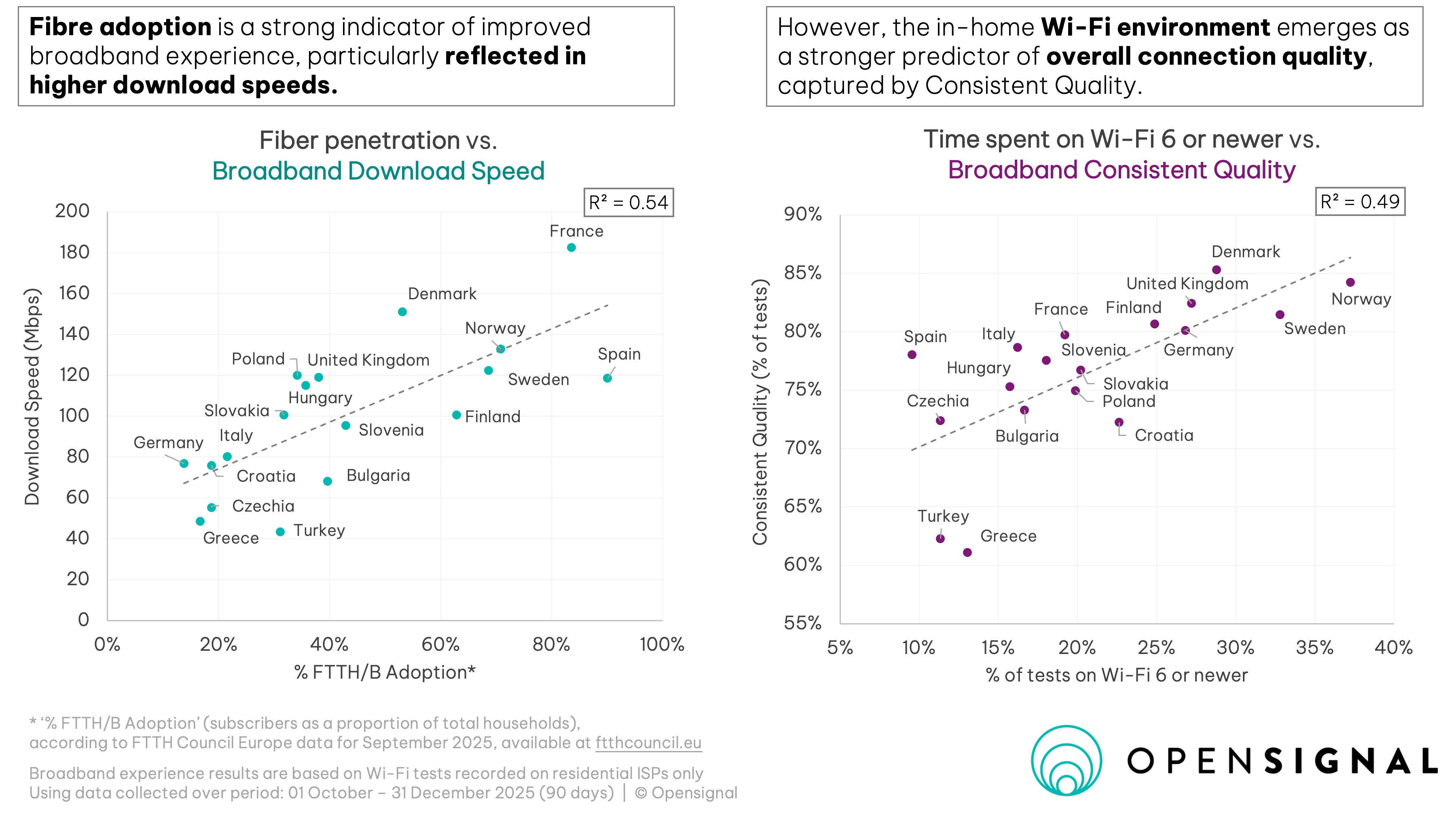

- Fiber-led markets deliver faster, more symmetrical speeds, but not always better overall experience. Our data shows a weaker relationship between FTTH/B adoption and Broadband Consistent Quality, highlighting the role of non-fiber infrastructure and in-home Wi-Fi conditions in shaping broadband performance.

- The quality bottleneck has moved inside the home. The micro-frictions created by poor Wi-Fi environment inside the home have a much stronger impact on overall connectivity experience, more so than the headline throughput capacity. Newer routers, better spectrum use, lower interference and stronger in-home coverage all translate into a better everyday user experience. Our data shows that markets where operators focus on providing customers with the latest Wi-Fi gateways achieve stronger Consistent Quality, while the biggest practical uplift comes from moving users off congested 2.4GHz connections and onto 5GHz or 6GHz.

Table of Contents:

Fiber rollout to migration challenges – where Europe stands today

Nearly a decade after Europe set its Gigabit Society goals, the fiber transition has materially advanced, but remains incomplete and is now facing a distinct set of new challenges. FTTH Council Europe’s 2026 Market Panorama shows that FTTH/B networks passed 191 million homes (76.8%) in the EU27+UK as of September 2025, yet only 105 million (42.1%) subscribed. This translates into a take-up of 54.9% among homes passed – the gap being one of the defining features of Europe’s broadband landscape today. The strategic problem is therefore no longer mainly whether fiber has been built, but whether operators can turn passed homes into active, paying fiber lines.

How infrastructure translates into better experience

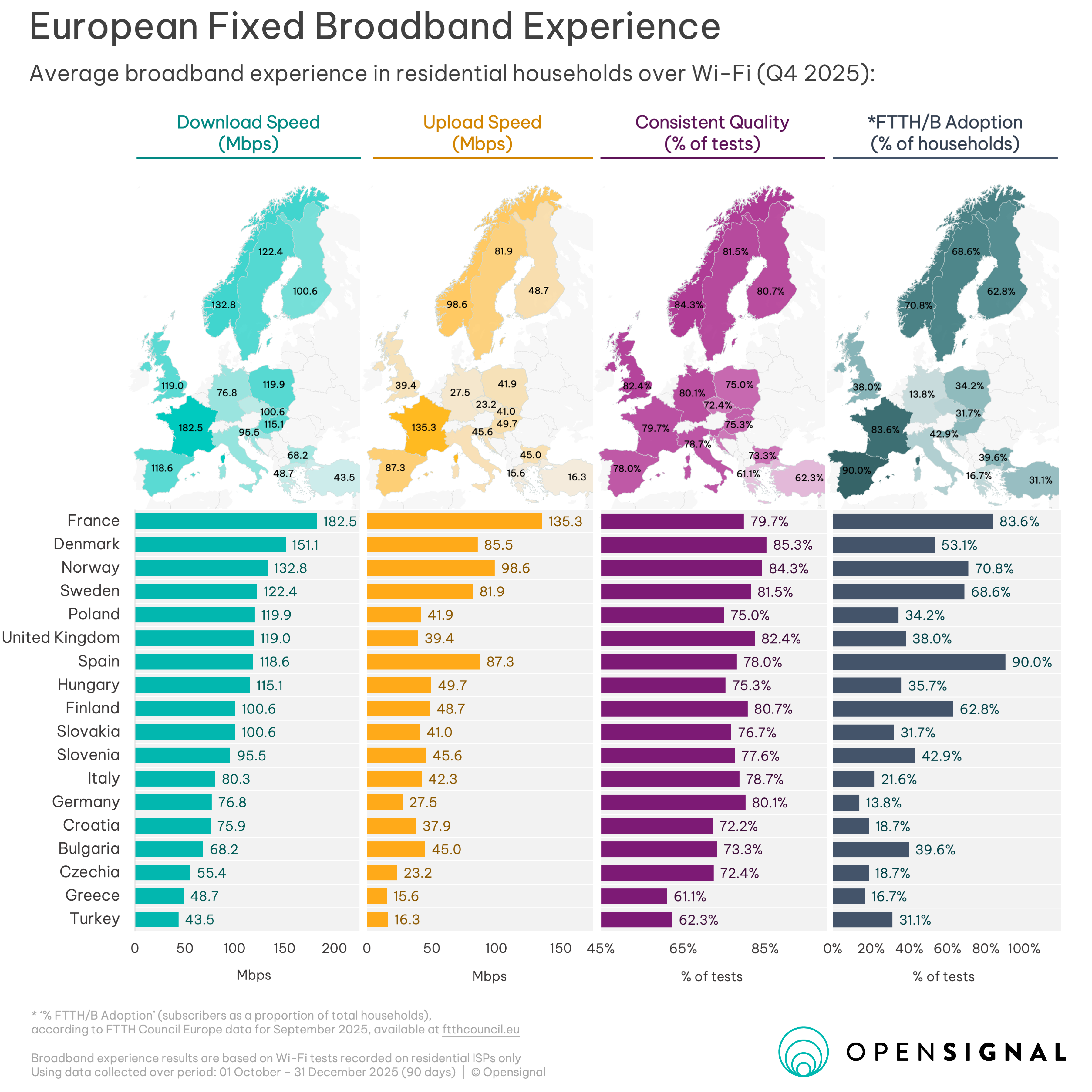

In this analysis, we assess broadband experience on residential providers as measured by Opensignal users across 18 European markets. All readings are taken from end-user devices while connected to residential broadband providers over Wi-Fi, giving a comparable view of the experience users actually receive inside the home.

We focus on three metrics:

- Broadband Download Speed and Broadband Upload Speed reflect the average speeds users observe in everyday use.

- Broadband Consistent Quality is a more comprehensive measure of what matters for experience. The metric is measured as the share of tests that exceed thresholds needed to support most common everyday online use cases, such as watching HD video, making video calls or playing online games. The metric is a composite measure of download and upload speeds, latency, jitter, packet loss and time to first byte. Full definition can be found here.

The underlying infrastructure across these markets still differs substantially. In this analysis, we supplement our data with fiber adoption figures from FTTH Council Europe, defined as FTTH/B (fiber-to-the-home/-building) subscribers as a percentage of total households.The data shows that, as of September 2025, FTTH/B adoption ranged from just 13.8% in Germany and 16.7% in Greece to 83.6% in France and 90.0% in Spain. This however, does not capture the full fixed broadband picture in markets where cable, modern fixed wireless or upgraded copper play important roles.

The European Commission’s VHCN (Very High Capacity Network) framework is technology-neutral, capturing other fixed networks capable of delivering comparable performance under peak conditions, most notably upgraded cable. On that broader definition VHCN coverage in the EU reached 82.5% of EU households in 2024, compared with its reported figure for FTTP coverage of 69.2%. This reflects the continued role of modern cable and other high-capacity networks in several markets, and highlights that gigabit-capable availability is somewhat ahead of active full-fiber footprint.

This leaves Europe with several different access-layer realities. Spain and France are the clearest fiber-advanced markets, with very high FTTH/B adoption and limited remaining copper dependence. Denmark, Germany, Hungary, Poland, Slovenia and the UK retain the highest share of cable/HFC (Hybrid Fiber-Coaxial) base among the included markets (estimated at >15% of broadband connections), meaning cable remains large enough to influence pricing, competitive dynamics and the pace of migration to full fiber. These markets form the most readily distinct outlier group.

This coexistence narrative came through clearly at FTTH Conference 2026, where industry voices described a prolonged phase-out in which HFC remains part of the access mix rather than being rapidly replaced. While universal fiber connectivity remains the long-term destination, HFC continues to play a rational role in parts of the footprint, and the next phase of the transition lies in navigating the complex and often messy process of copper retirement.

In our data among the European markets France stands out with the highest average speeds at 182.5Mbps download and 135.3Mbps upload, while Norway reaches 132.8Mbps down and 98.6Mbps up, and Spain 118.6Mbps down and 87.3Mbps up. These more symmetrical download and upload outcomes are consistent with markets where fiber has become a much larger part of the fixed broadband base. By contrast, more asymmetric profiles remain visible in HFC-legacy markets – such as the UK at 119.0Mbps down and 39.4Mbps up, and Germany at 76.8Mbps down and 27.5Mbps up.

Meanwhile, our data points to a finding that higher fiber adoption does not automatically translate into the stronger overall broadband experience – as reflected in our measure of Consistent Quality. Europe’s most fiber-advanced markets, France and Spain, demonstrate Consistent Quality scores of 79.7% and 78.0%, below those seen in Denmark at 85.3%, Norway at 84.3%, or Sweden at 81.5% – where in-home Wi-Fi experience comes into play as the explanatory link.

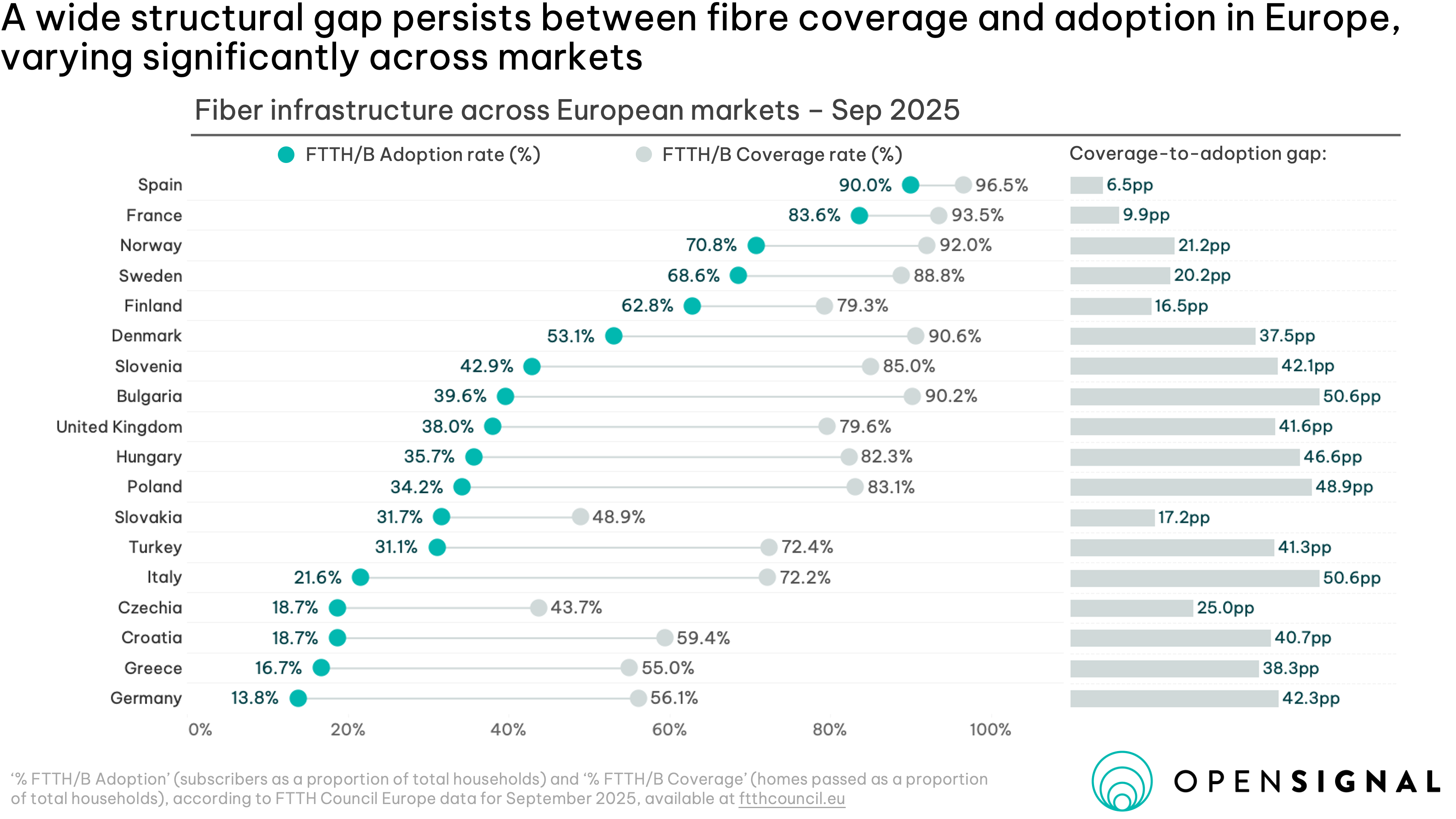

Rapid rollout has left many markets with a large adoption gap

The uneven progress of Europe’s fiber transition is not only visible in rollout, but also in how effectively coverage is converted into active subscriptions. This variation is now central to understanding the scale of unrealised potential across the region. Spain and France stand out as the most advanced markets, combining near-universal coverage — with fiber available to more than 9 in 10 households (96.5% and 93.5% respectively) — with equally strong adoption, as over 8 in 10 households (90.0% and 83.6%) have already subscribed. As a result, their fiber footprint is close to fully utilised.

In contrast, adoption has lagged more noticeably in the Nordics, where the coverage-to-adoption gap ranges from 16.5 percentage points in Finland to 37.5 in Denmark. A larger middle tier of markets — including the UK, Poland, Bulgaria, Hungary, Turkey and Italy — shows a wider disconnect, where fiber coverage is ranging from 72.2% to 90.2%, but adoption remains limited at just 21.6% to 39.6%. This leaves a significant share of fiber infrastructure underutilised, with coverage-to-adoption gaps reaching as high as 50.6 percentage points in Italy and Bulgaria.

Notably, many HFC-legacy markets sit toward the higher end of this adoption gap, underlining how the continued presence of cable can slow migration onto fibre. Where existing cable or upgraded copper connections remain good enough for everyday needs, many households do not feel a strong reason to switch. In that sense, the industry has also created an “overshoot market”, offering extreme multi-gigabit capabilities that exceed what the average consumer currently needs or is willing to pay extra for. Unless a household consists of gamers or other heavy data users, the technical superiority of fiber does not translate into an attractive selling proposition over the existing packages.

This creates a significant commercial problem. Kearney’s European Telecom Health Index, based on a survey of 20,000 consumers across 21 European countries, reported that demand-side behaviour is a major barrier to fibre monetisation. In slow-adopter markets such as Italy, the Netherlands, Poland, Ireland and Denmark, fibre take-up (adoption as a proportion of coverage) is closer to 45% and returns on capital employed have fallen to 6%, compared with take-up of up to 84% and returns of 11% in stronger markets such as Sweden, Norway, France, Spain and Portugal.

The operational reality of migration is also messy. Unlike turning off legacy voice networks, copper broadband retirement requires physical, household-level intervention. Migration is expensive and labour-intensive, involving dispatching installation teams, rewiring the home, replacing customer equipment, and managing appointments. Customers view this disruption and the need for in-home works as a significant source of friction, especially when their current experience is already satisfactory. Many consumers also mistakenly believe they already have full fiber when they do not, effectively killing any urgency to migrate, while others remain attached to legacy services such as traditional cable TV setups and are uncomfortable switching to IPTV.

The challenge can be more complex in apartment blocks and other multi-dwelling units. FTTB deployments typically already include the connection to the building, but in some units, access permissions, internal wiring choices, shared infrastructure and split decision-making can slow conversion from a passed building to active fibre subscriptions.

Operators also have reason to prefer demand-led migration over supply-led migration. The cost of connecting customers to fibre is fundamental to the investment case, but proactively moving a satisfied VDSL or cable customer can “poke the bear”: it forces the household to reconsider its broadband service, compare alternatives and potentially switch providers. In competitive markets, the migration moment can therefore become a churn risk This helps explain why operators often prefer customers to move when they already perceive a need, rather than being pushed into a change while their existing connection still feels good enough.

The battleground for closing the experience gap is inside the home

The next battleground in European broadband increasingly sits inside the home. Fiber can raise the ceiling of broadband performance, but the experience users actually feel is shaped by the Wi-Fi layer: router quality, device capability, band usage, interference, household layout and whether users remain stuck on older Wi-Fi generations. This was also evident at FTTH Conference 2026, where industry discussions repeatedly returned to customer micro-frictions such as buffering, dead zones, lag, unstable video calls and inconsistent performance as users move around the home. These everyday issues matter more to perceived quality than abstract claims about maximum line speed.

The burden on home networks is also rising. Households are connecting more smart home devices, and the progressively growing data demands create congestion on the Wi-Fi that is coming not only from within the home, but also from the neighbouring networks and offices.

Wi-Fi frequency bands are central to understanding this dynamic:

- 2.4GHz is useful because it travels further and penetrates walls better, but is often crowded and has limited capacity. It has fewer non-overlapping channels, narrower usable bandwidth, and more interference from neighbouring Wi-Fi networks. It is therefore good for reach, but poor for consistently high-capacity performance.

- 5GHz is the major step change. It does not travel as far as 2.4GHz and is more affected by walls, but it offers much more usable capacity, wider channels (20/40/80MHz and even 160MHz) and typically less congestion. For most demanding broadband use cases, moving from 2.4GHz to 5GHz users feel the benefit of a better wireless connection.

- 6GHz improves on 5GHz, but the uplift is more incremental unless congestion is at play. 6GHz adds cleaner, more contiguous spectrum, making it easier to use wider channels with less overlap — although the number of available wide channels depends on national spectrum rules. Because 5GHz is already a high-capacity band, the move from 5GHz to 6GHz only brings benefits for higher demand and latency intensive use cases, within more densely congested areas. Its real-world benefit is still limited by router availability, device compatibility and whether households are close enough to the access point to use it effectively.

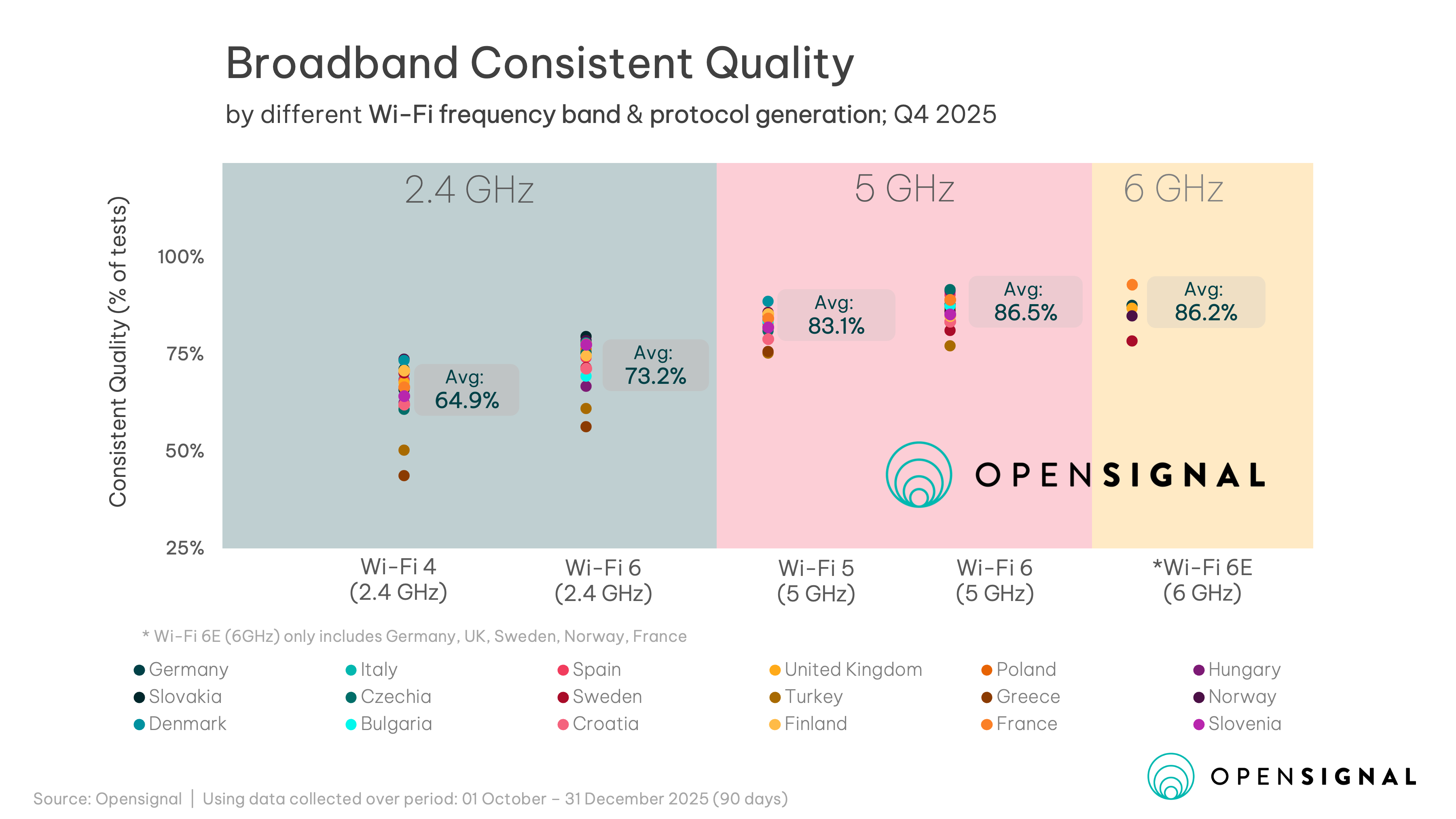

That pattern is visible in our data. Across the region, average Broadband Consistent Quality rises from 64.9% on Wi-Fi 4 over 2.4GHz to 73.2% on Wi-Fi 6 over 2.4GHz. Newer protocol generations clearly help. But the larger step change comes when users move onto higher-capacity spectrum: average Consistent Quality reaches 83.1% on Wi-Fi 5 over 5GHz and 86.5% on Wi-Fi 6 over 5GHz. On 6GHz, Wi-Fi 6E delivers an average of 86.2% across the subset of markets where we have enough observations. The key point is not that 6GHz is unimportant, but that the biggest practical improvement usually comes from getting users off congested 2.4GHz and onto 5GHz or 6GHz in the first place.

That helps explain why line upgrades do not always translate neatly into better lived experience.

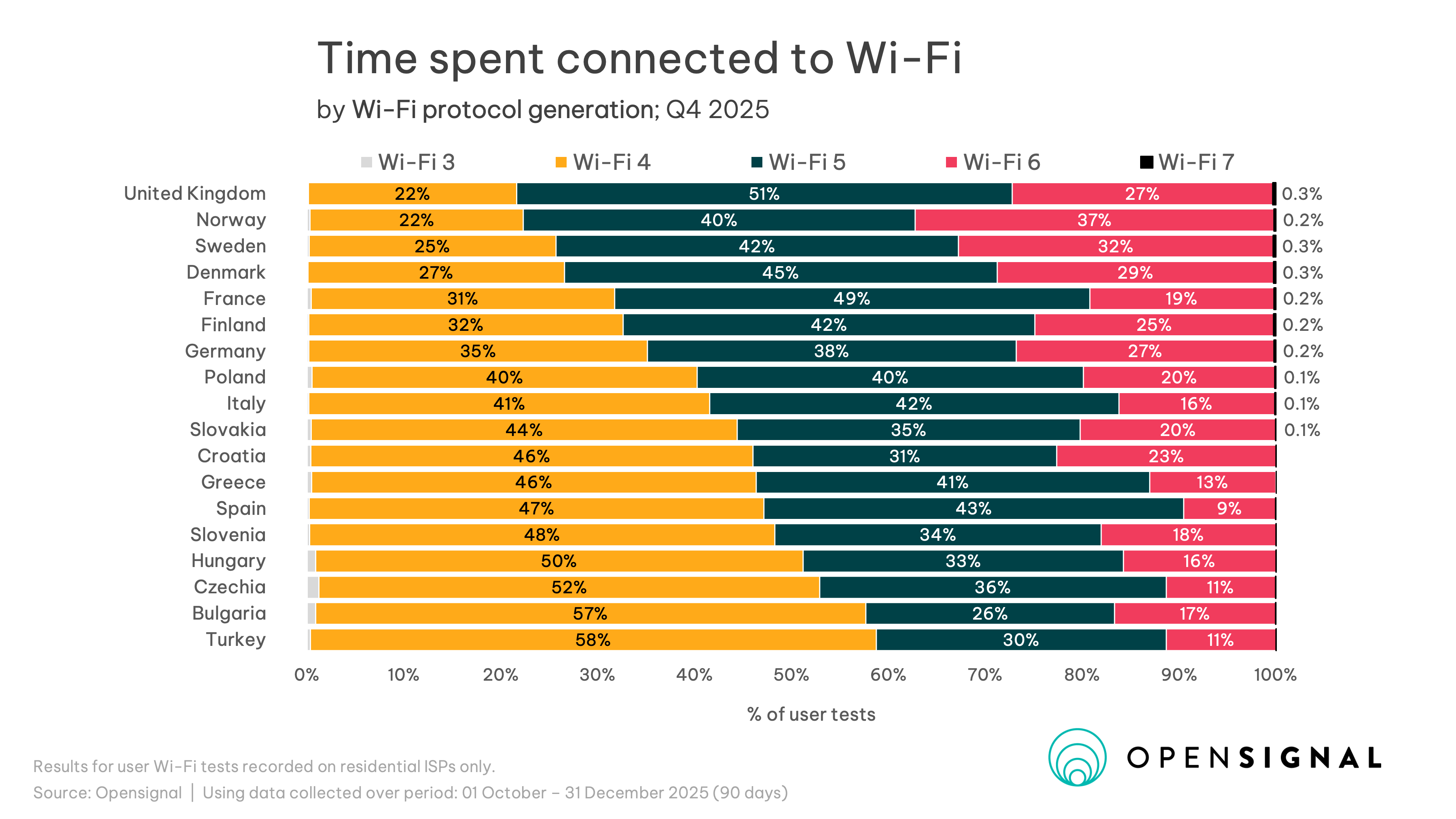

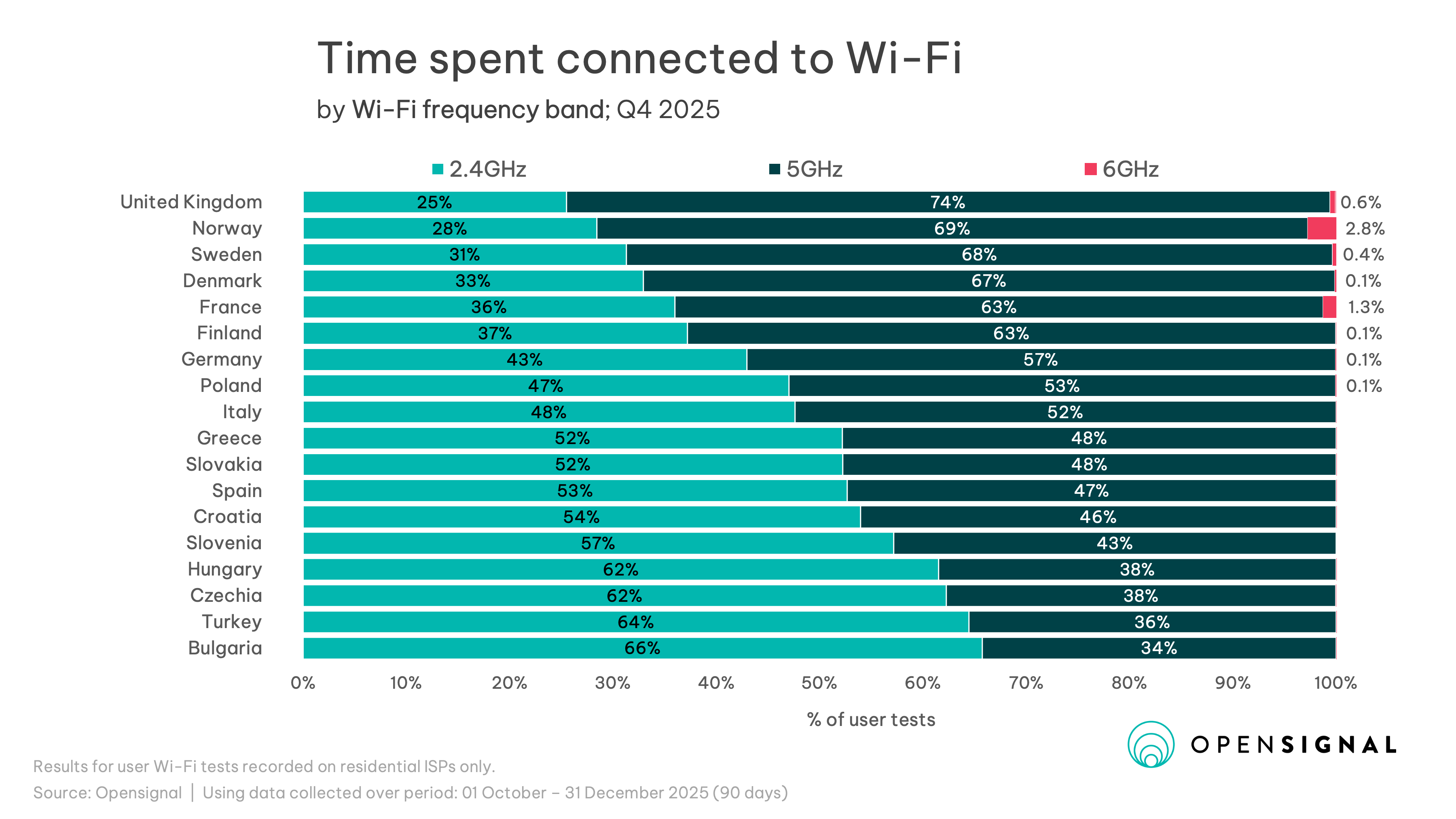

In the strongest markets, Wi-Fi 6 accounts for a large share of time residential broadband users spend online with 37% of user time in Norway, 32% in Sweden, 29% in Denmark, and 27% in the UK and Germany. But elsewhere, the home layer remains stuck further back, Wi-Fi 4 still accounts for around half or more of connected time in Hungary, Czechia, Bulgaria and Turkey, and remains very high in Spain, Slovenia, Croatia and Greece. Wi-Fi 7 was barely visible yet at the end of Q4 2025, but has since been gaining footing with widescale adoption by providers.

Europe’s broadband market is therefore not only split by fiber adoption; it is also split by how far households have progressed in the in-home upgrade cycle.

Our market results reinforce this distinction between access infrastructure and in-home delivery. Fiber adoption remains a good indicator of speed: markets with higher FTTH/B adoption generally deliver faster download experience. But fiber adoption is a less complete explanation of overall connection quality, as seen through a weaker relationship with Consistent Quality. The relationship becomes clearer when we compare Consistent Quality with the share of tests spent on Wi-Fi 6 or newer.

The implication is straightforward – fiber still matters, but the in-home Wi-Fi environment is becoming a stronger predictor of whether users actually feel the benefit.

The same pattern appears in spectrum usage. 5GHz is now the dominant working band in most of the markets we looked at, but 2.4GHz still accounts for a large share of time in lower-performing markets, and 6GHz remains niche. Even among users with compatible devices, meaningful 6GHz usage is visible only in a handful of countries, led by France and Norway. This suggests that the bottleneck is no longer only device capability. It is also the installed base of home gateways, the availability of newer Wi-Fi standards in operator-provided CPE, router placement, and whether households are actually connecting over the better-performing bands.

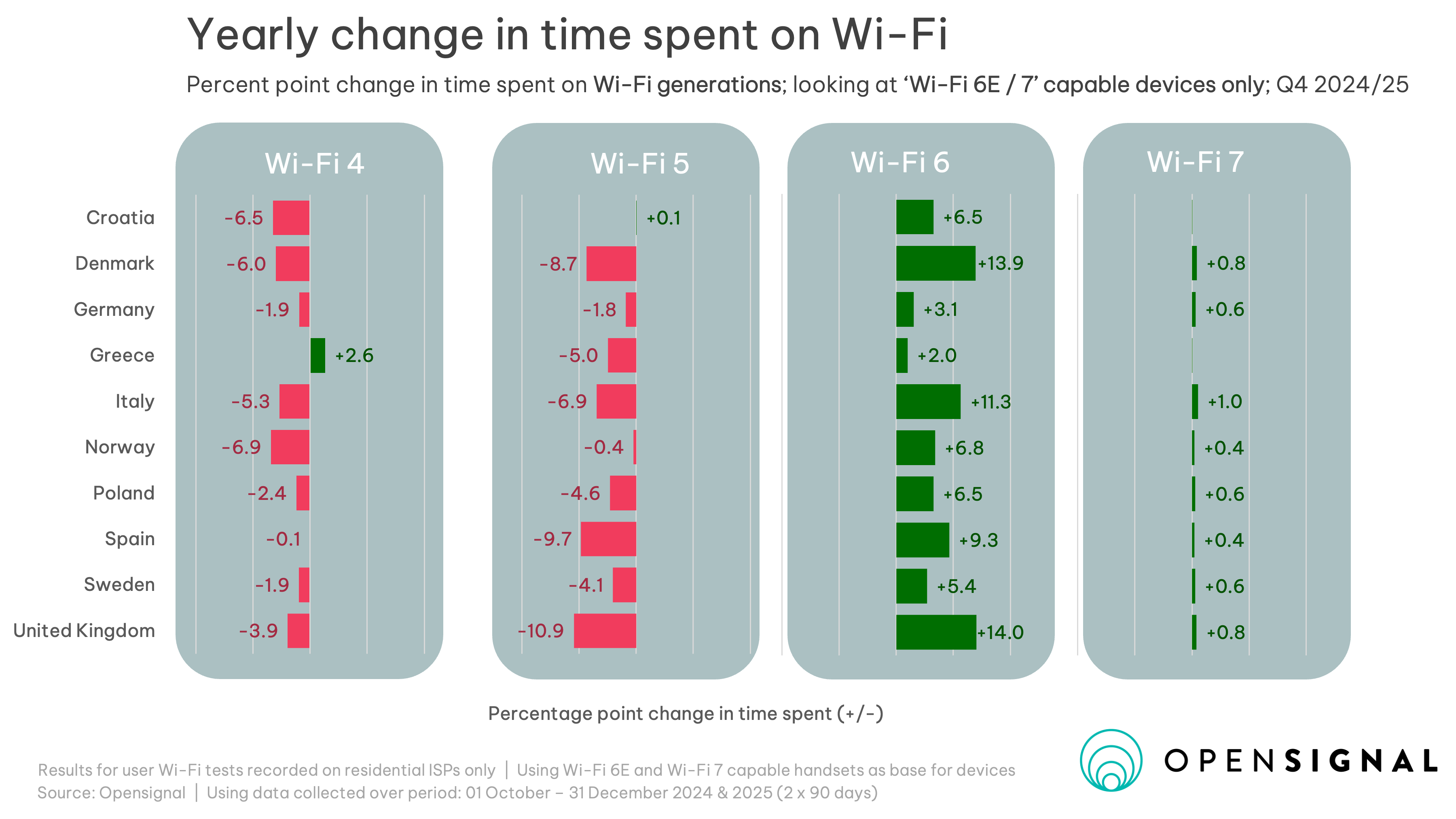

Meanwhile, the upgrade cycle is moving rapidly. Compared with a year earlier across all European markets we tracked, the share of time spent on Wi-Fi 6 has risen sharply, particularly in the UK, Denmark, Italy and Spain, at the expense of Wi-Fi 5 and Wi-Fi 4. But the transition is not uniform, as some markets remain much more dependent on older generations and 2.4GHz connections.

This has direct implications for how broadband is being assessed and sold. In-home Wi-Fi is no longer sitting separately from the provider’s broadband connection, but is part of a single service package. As operators look for new ways to improve customer satisfaction and monetise fiber investment, the experience inside the home is central to that conversation. That includes more modern gateways, proactive customer support, and a greater focus on consistency and reliability. Operators are actively developing service in this area — for example Vodafone Spain offers coverage assessments with live technicians, who advise on optimal router placement or the need for mesh extenders, while Deutsche Telekom says it analyzes Wi-Fi signals of its customers connections as part of the fixed-line customer management. In mature broadband markets, the next layer of differentiation is now opening avenues for future technologies enabled by AI – including sensing movement around the home, and parsing the wealth of data available on customer relationships that was untapped before.

More from Opensignal

Further reading on the themes explored in this report can be found in our previous publications:

- Fixed Broadband Experience: European Awards (Feb 2026)

- Experienced speed tiers vs. subscribed speed tiers: The bottleneck of home Wi-Fi (Jul 2025)

- Wi-Fi 7 vs. previous generations (May 2025)

- How ISP-issued gateways drive better home broadband in the US (Apr 2025)

- The impact of Wi-Fi generation and frequency bands on the Spanish fixed broadband experience (Sep 2024)

- Bridging the digital divide: Unlocking reliable broadband for all (Jul 2024)

To learn more about our capabilities and explore how Opensignal can support your use case, please get in touch via our contact form.

Opensignal Limited retains ownership of this insight including all intellectual property rights, data, content, graphs & analysis. Reports and insights produced by Opensignal Limited may not be quoted, reproduced, distributed, published for any commercial purpose (including use in advertisements or other promotional content) without prior written consent. Journalists are encouraged to quote information included in Opensignal reports and insights provided they include clear source attribution. For more information, contact [email protected].