The debate over whether Wi-Fi or mobile dominates data consumption in Asia Pacific misses a more important reality: the region is not converging on a single connectivity model. Consumer behavior is increasingly shaped around two distinct trajectories, influenced by local usage patterns and the cost and availability of networks.

In some markets, expanding fixed infrastructure and falling broadband prices are pulling users toward Wi-Fi — both fixed-line and fixed wireless access (FWA) services. In others, improving mobile network quality — driven by 5G — is making cellular connectivity “good enough” to replace fixed access for everyday use. But time spent on a network does not tell the full story of how data is consumed.

Opensignal data reveals that the real story is a divergence driven by infrastructure, economics, and user behavior. Using our data across 12 Asia–Pacific markets, this analysis shows how opposing forces — affordability, infrastructure investment, policy, and network performance — are reshaping how smartphone users consume data, and why the balance between Wi-Fi and mobile is increasingly market-specific rather than universal.

Key Findings:

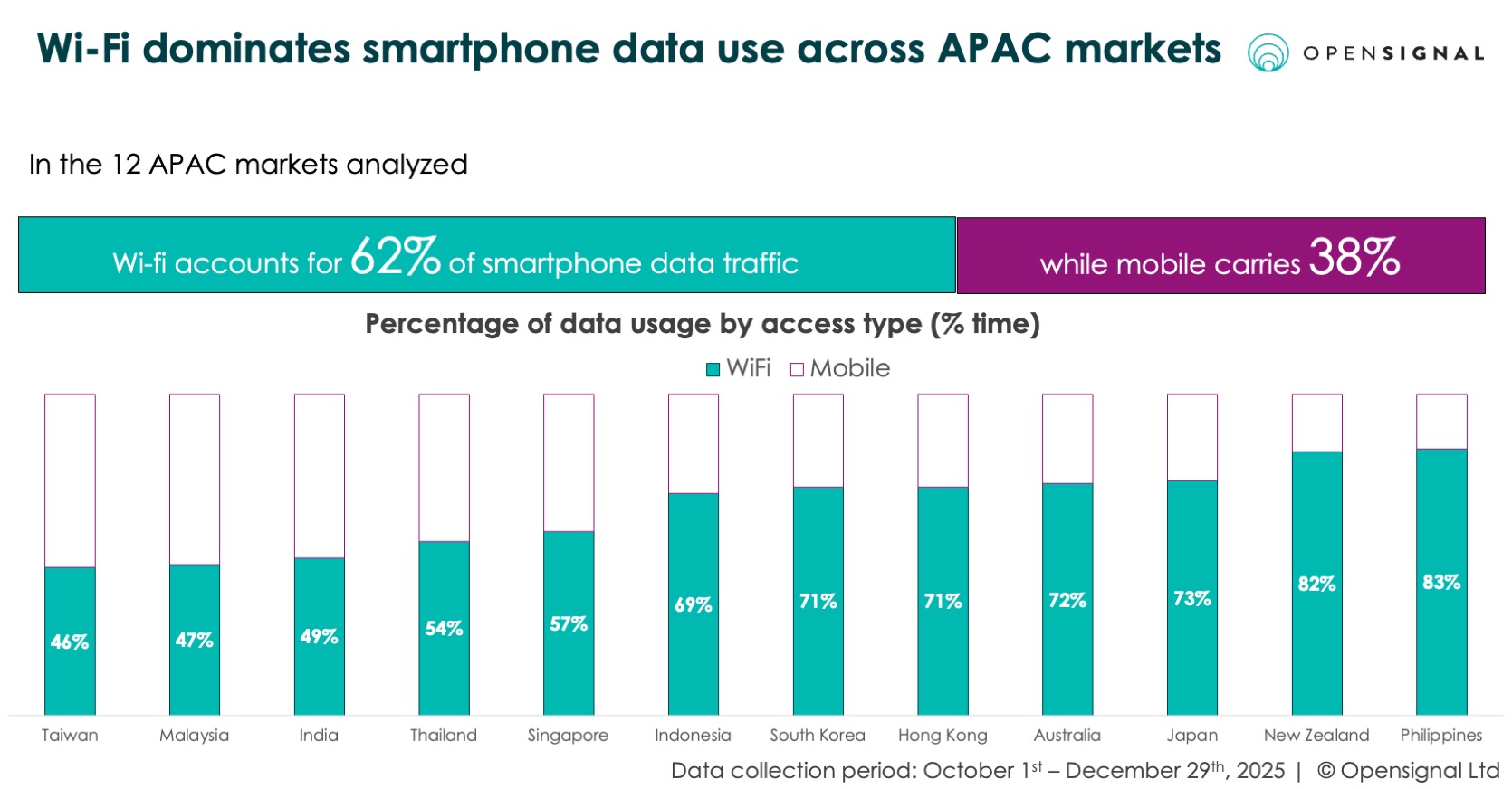

- Wi-Fi still dominates data consumption, but mobile plays a larger role in some markets. Across Asia Pacific, fixed broadband services account for 62% of total smartphone data traffic — but the share of data traffic carried over mobile services exceeds 50% in markets such as Taiwan, Malaysia, and India.

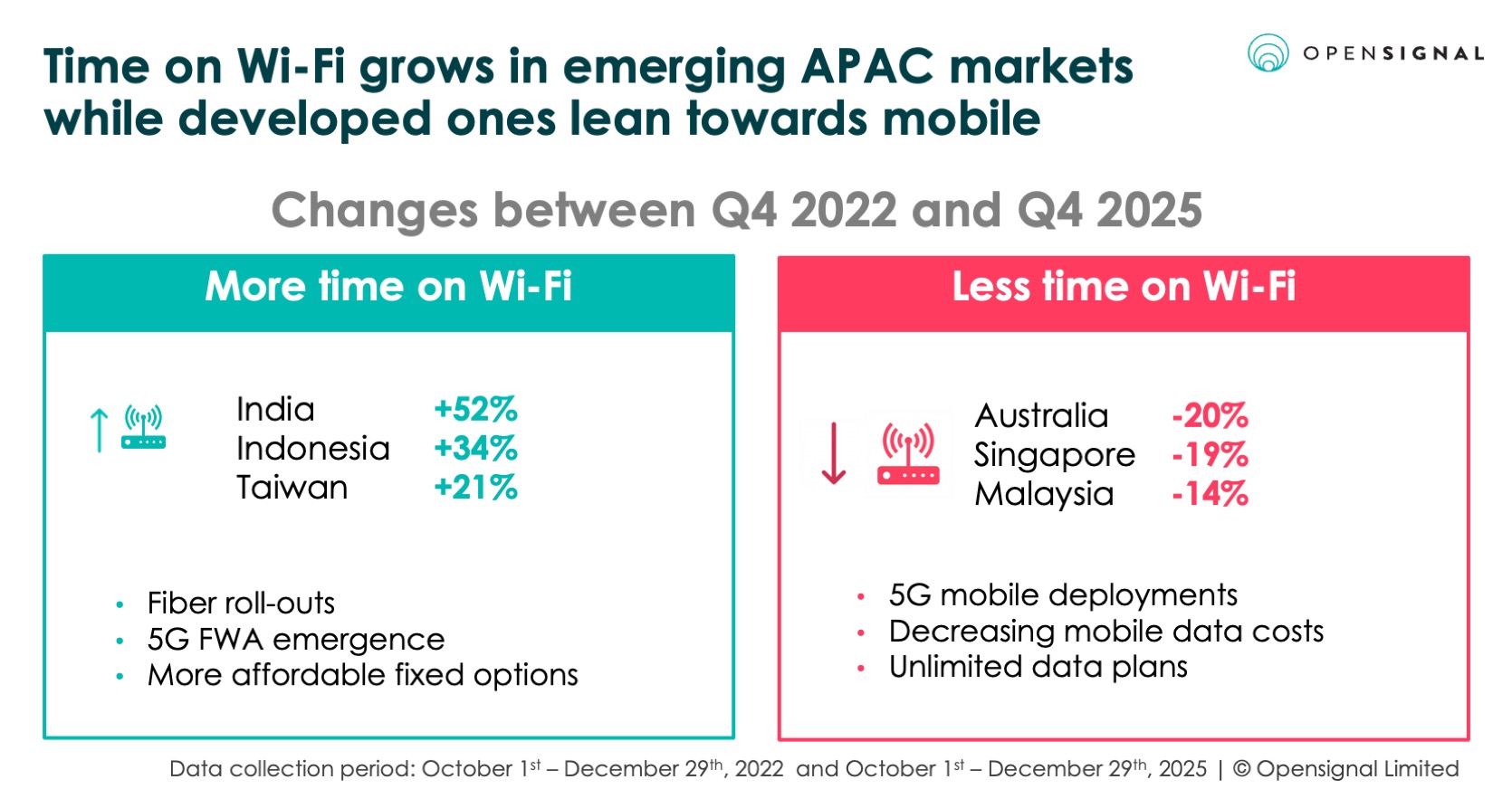

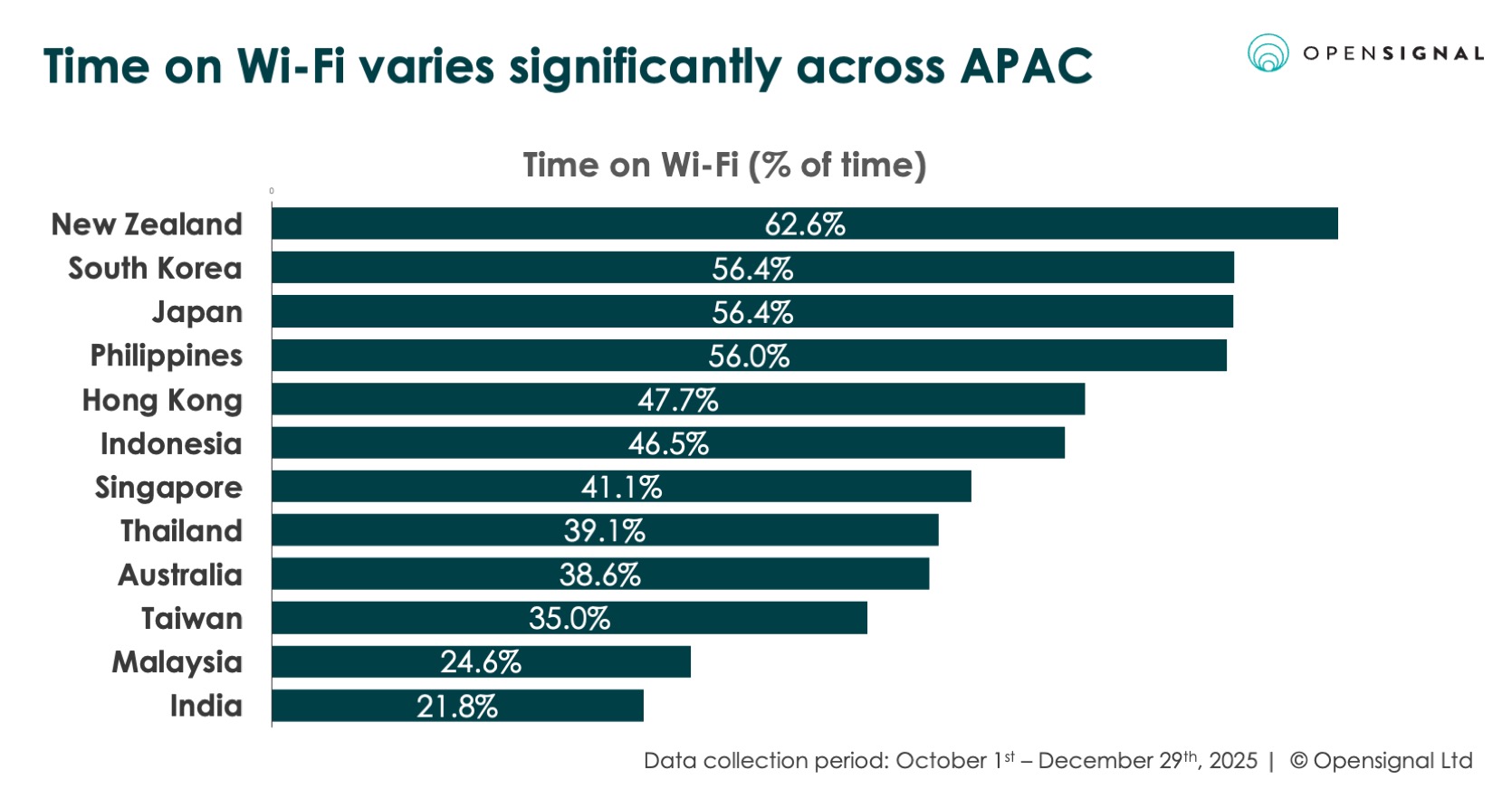

- Patterns of time spent on technology are shifting in opposite directions. Traditionally mobile-first markets such as India and Indonesia are seeing users move toward Wi-Fi — both fixed-line and FWA services. Meanwhile, more mature markets like Australia and Singapore are gravitating toward mobile data, driven by 5G improvements in mobile network quality and falling prices of mobile data.

- Wi-Fi remains the default for heavy data use. Smartphone users in APAC consume a disproportionately larger share of data over Wi-Fi relative to the time spent on it, indicating a continued preference for Wi-Fi for high-volume usage.

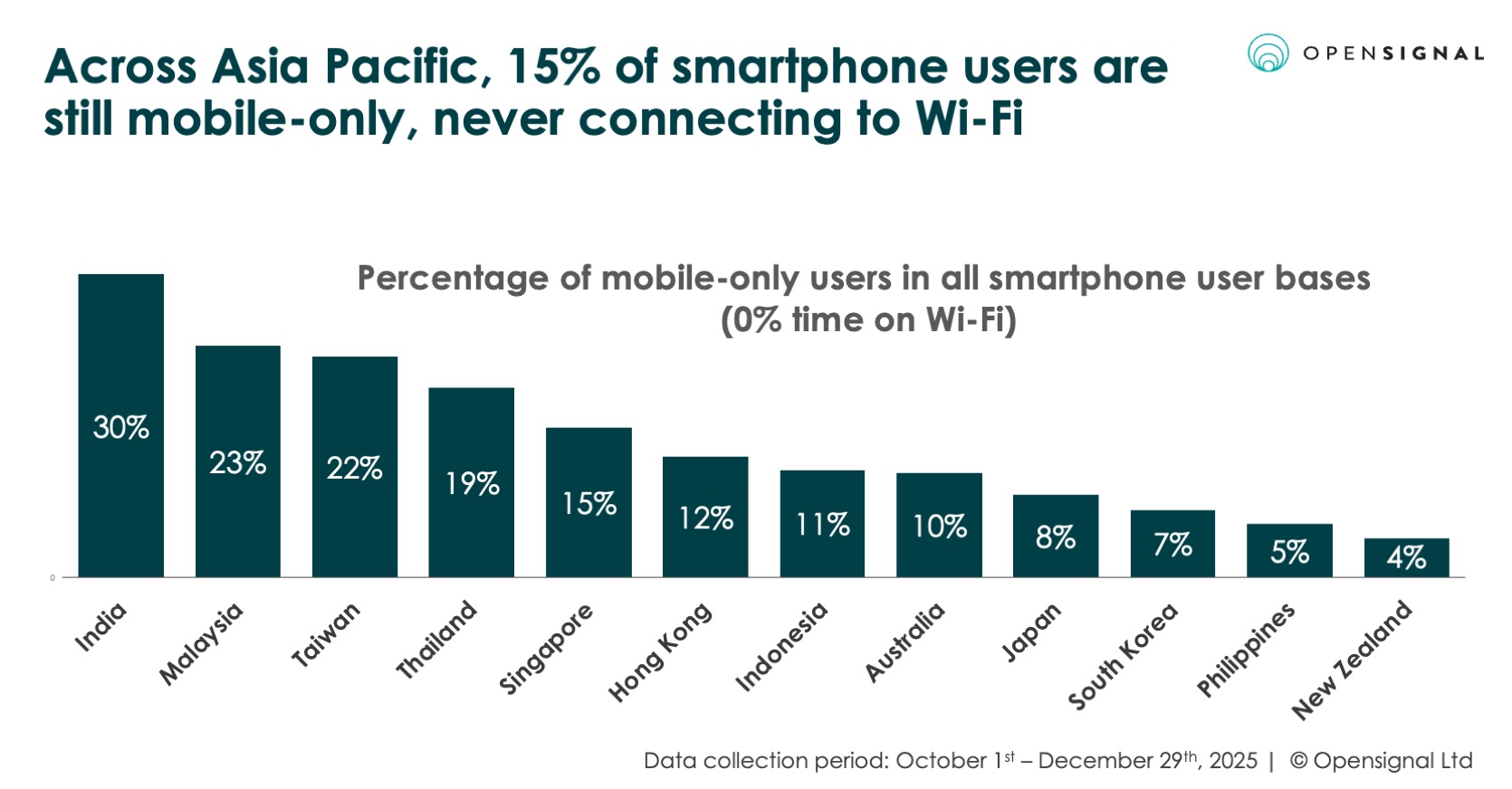

- For many users across Asia Pacific, mobile remains the only means of internet access. 15% of smartphone users in the region never connect to Wi-Fi, rising to 30% in India.

Table of Contents:

The Great Divergence: Two Paths for One Region

Asia Pacific has seen the fastest growth in data traffic of any region, across both fixed and mobile services. While Wi-Fi — both fixed-line and fixed wireless — accounts for 62% of total data usage across the 12 analyzed markets, this headline figure overshadows diverging trends. In markets such as Taiwan, Malaysia, and India, more than half of smartphone data traffic is carried over mobile networks.

Given Asia Pacific’s economic and social diversity, two distinct — and opposing — trajectories are unfolding across the region.

Path 1: Emerging markets are moving toward Wi-Fi

Emerging Asia Pacific markets still rely heavily on mobile for internet access. 15% of smartphone users in the region go online exclusively via mobile, never using Wi-Fi according to Opensignal data. In India, this figure is even double — 30%.

This underscores a broader challenge in many emerging markets: mobile internet use is driven more by accessibility and affordability, rather than preference. Household budgets often cannot support both mobile and fixed subscriptions, while broadband often isn’t available in rural areas and lower-income urban and suburban areas. As a result, mobile connectivity remains the primary, and sometimes only, means of internet access, mirroring patterns previously observed across Africa and Southeast Asia.

However, over the past three years, markets with substantial shares of mobile-only users, such as India or Indonesia, have recorded the largest increases in Time on Wi-Fi. Expanded fiber rollouts in India or Indonesia have played a key role in widening access to fixed internet in these densely populated countries. More affordable prepaid fiber options — such as those offered in the Philippines — have also lowered barriers to adoption of fixed-line services.

5G-powered fixed wireless access (FWA) is another factor contributing to increased Wi-Fi usage, particularly in India. The technology is expanding rapidly across Asia Pacific, enabling operators to deliver high-speed broadband to underserved or remote areas more quickly and cost-effectively than fiber.

Public policies behind digital society initiatives can also drive the shift from mobile to Wi-Fi, especially when they enable access to free Wi-Fi services. India has been developing public Wi-Fi access programs, like PM-WANI, which provides free Wi-Fi at thousands of public locations. Governmental smart city initiatives like iTaiwan can also explain the increase in time spent on Wi-Fi in Taiwan — which is a developed market with the highest mobile data consumption among those analyzed.

The Philippines is another example of a market where government initiatives are driving increased time spent on Wi-Fi and higher data consumption over Wi-Fi. The Department of Information and Communications Technology (DICT) has been rolling out the Pipol Konek (Free Wi-Fi for All) initiative over the past several years. The program is now undergoing a major overhaul, with the government exploring potential partnerships — possibly including Starlink — to accelerate and expand nationwide Wi-Fi deployment.

While 5G supercharges FWA, making it a viable fixed-line alternative, the increased capabilities of mobile 5G is driving the opposite trend in some more developed markets.

Path 2: Mature markets are gravitating toward mobile

In countries like Australia and Singapore — where fixed broadband is already nearly ubiquitous — mobile 5G is becoming "good enough" to replace Wi-Fi for many everyday tasks.

In effect, users are spending less time on Wi-Fi and increasingly relying on mobile networks. This shift is being driven primarily by expanded spectral capacity — especially from mid-band 5G deployments — which has made mobile services fast and reliable enough for everyday use, reducing the need for Wi-Fi. 5G Standalone also contributes to future capabilities — and 5G has already stimulated demand through higher capacity, broader coverage, and new service tiers enabled by technologies such as network slicing.

The growing availability of unlimited mobile data plans in more mature markets — supported by falling mobile data costs, like in Singapore — has reinforced the shift toward mobile services. As mobile data becomes more affordable, some users may choose to forgo fixed broadband altogether and rely instead on “good enough” mobile connectivity.

Improved mobile network performance also reduces the need to rely on public Wi-Fi, which is often unreliable, may pose security risks, requires registration, or delivers limited performance on free tiers. This pattern mirrors what we have observed at airports in the U.S. or Japan, where time spent on Wi-Fi is well below national averages, indicating that users increasingly rely on mobile connectivity when it adequately meets their needs, rather than deferring to public Wi-Fi.

While Malaysia is at an earlier stage of market maturity than Australia and Singapore, it has nevertheless seen steady 5G rollouts as well, along with unlimited prepaid data plans. However, another key driver of the shift from Wi-Fi to mobile is the success of the JENDELA program, which has expanded 4G/5G mobile coverage into underserved areas where fixed-line access is often unavailable or prohibitively expensive. By closing the digital gap and connecting new users and regions, the program has increased overall time spent on mobile networks.

Wi-Fi still carries the heavy data load in APAC

A key finding in our data is that time spent on a network does not fully reflect how data is consumed. Smartphone users show a clear “heavy-lift” bias: even when they spend most of their time not connected to Wi-Fi, they tend to reserve data-intensive activities for this technology.

Although expanding 5G coverage reduces reliance on Wi-Fi for everyday use, heavier data transfers are still typically deferred to Wi-Fi — either fixed-line or FWA services. This behavior is often reinforced by device settings, as large app or system updates are usually recommended — or sometimes restricted — to Wi-Fi connections.

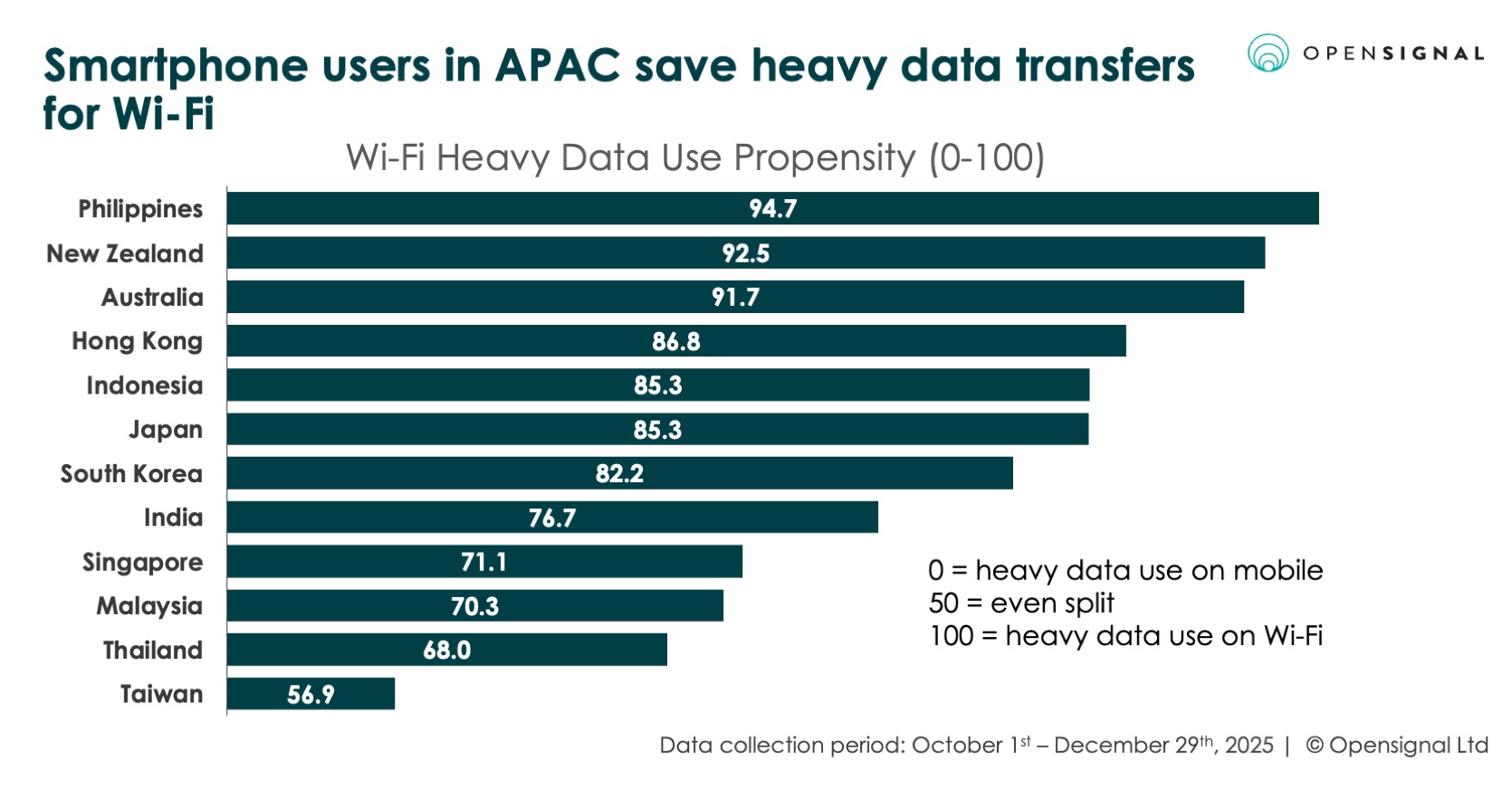

This pattern is clearly reflected in our data: across all 12 analyzed markets, the share of data traffic carried over Wi-Fi exceeds the share of time spent on Wi-Fi. This imbalance shows that the relationship between time spent on Wi-Fi and data usage is not linear, with heavier data loads disproportionately shifted to Wi-Fi. In other words, smartphone users consistently rely on Wi-Fi for more high-volume usage, though the strength of this preference varies by market.

Wi-Fi Heavy Data Use Propensity scores highlight a very strong preference for Wi-Fi in some markets, exceeding 90 in New Zealand, the Philippines, and Australia — even where overall time spent on Wi-Fi is relatively lower, like in Australia. By contrast, Taiwan scores closer to 50, indicating more balanced use of Wi-Fi and mobile networks and a lower reliance on Wi-Fi for heavy data traffic. In countries such as Taiwan, Malaysia, and Singapore, the widespread availability of unlimited data plans — even on prepaid services — encourages greater mobile data use, reducing reliance on fixed broadband networks for data transfers.

What does the future hold for data consumption in APAC?

Wi-Fi continues to play a central role in data transfers across all Asia Pacific markets — but reliance on it varies widely. At the same time, mobile data traffic is growing faster than fixed broadband, both in Asia Pacific and globally, with some APAC markets carrying more than 50% of smartphone data traffic on mobile networks.

Historically, fixed-line services were viewed as faster, cheaper per 1GB consumed, and more reliable, with a key advantage: the absence of data caps, allowing unrestricted use without performance penalties. As a result, consumers have long treated fixed and mobile internet as complementary rather than interchangeable.

This dynamic is beginning to shift with the expansion of 5G, while data-metered plans are becoming more common in fixed broadband, as seen in Starlink and some FWA offerings. However, in many APAC markets, 5G’s impact on total traffic remains limited by spectrum constraints and the high cost of network deployment. Some industry sources such as GSMA and Ericsson continue to forecast sustained growth in data usage across the region, others like recent research from Tefficient suggests that growth rates are slowing down globally.

Opensignal believes that several factors will shape future demand in Asia Pacific:

- Demographics: Younger generations are heavy users of video-centric platforms such as YouTube and TikTok.

- Services: the continued expansion of high-bandwidth applications — particularly high-resolution video streaming — alongside emerging AR/XR and GenAI apps.

- Accessibility: The availability and quality of fixed and mobile broadband services, along with access to capable devices.

- Affordability: While data and devices are becoming cheaper overall, cost constraints persist in parts of emerging APAC.

- Competition: Market pressure is likely to push operators to innovate on both pricing and network quality.

- Public policy: Government initiatives that enable internet deployment and promote its use for work, education, and entertainment.

Ultimately, data consumption in Asia Pacific will not be defined by a single access technology. Instead, it will reflect an evolving balance between mobile and fixed networks, as convergence increasingly blurs the line between the two. This shift will be shaped by successive generations of mobile technology — from 5G today to 6G in the future — alongside fixed broadband developments. As users increasingly default to the option that offers the best mix of performance, affordability, and convenience, their choices will guide investment priorities across the ecosystem.

Read out insight on data consumption in the U.S. If you're interested in more of our tailored analysis or in our Digital Shelf Market Analytics to track down Fixed or Mobile Price Tracking then please contact us. Don’t forget to subscribe to Opensignal’s newsletter for deeper insights on Indonesia and global markets.

If you are interested to see data behind the charts, please fill in this form.

Methodology

Wi-Fi Heavy-Data Use Propensity Score combines data intensity and usage footprint to show where heavy data use on Wi-Fi occurs and to what extent. It is calculated by deriving Wi-Fi and mobile data intensity ratios (technology data share divided by time on technology share), weighting them by each technology’s data share, and expressing Wi-Fi’s contribution as a 0–100 score. Higher scores indicate greater reliance on Wi-Fi for data-intensive use. A score of 50 represents perfectly balanced use between Wi-Fi and mobile services.

Additional charts

Data consumption

Mobile-only users

Time on Wi-Fi

Opensignal Limited retains ownership of this insight including all intellectual property rights, data, content, graphs & analysis. Reports and insights produced by Opensignal Limited may not be quoted, reproduced, distributed, published for any commercial purpose (including use in advertisements or other promotional content) without prior written consent. Journalists are encouraged to quote information included in Opensignal reports and insights provided they include clear source attribution. For more information, contact [email protected].