by Giulio Sinibaldi (main author), and Andrey Popov (supporting author)

The 5G RAN sharing agreement, announced on 7 January 2026 by TIM and Fastweb+Vodafone, represents the latest development in the ongoing consolidation of the Italian telecommunications market. While broader competitive and regulatory implications will unfold over time, the immediate network-level effects are clearer: accelerated rural 5G expansion, measurable improvements in 5G Coverage Experience, and stronger positioning ahead of Italy’s 2029 spectrum renewal process.

This analysis focuses exclusively on network and customer experience implications. It does not assess potential competitive dynamics, cost efficiencies, or regulatory outcomes.

Key takeaways

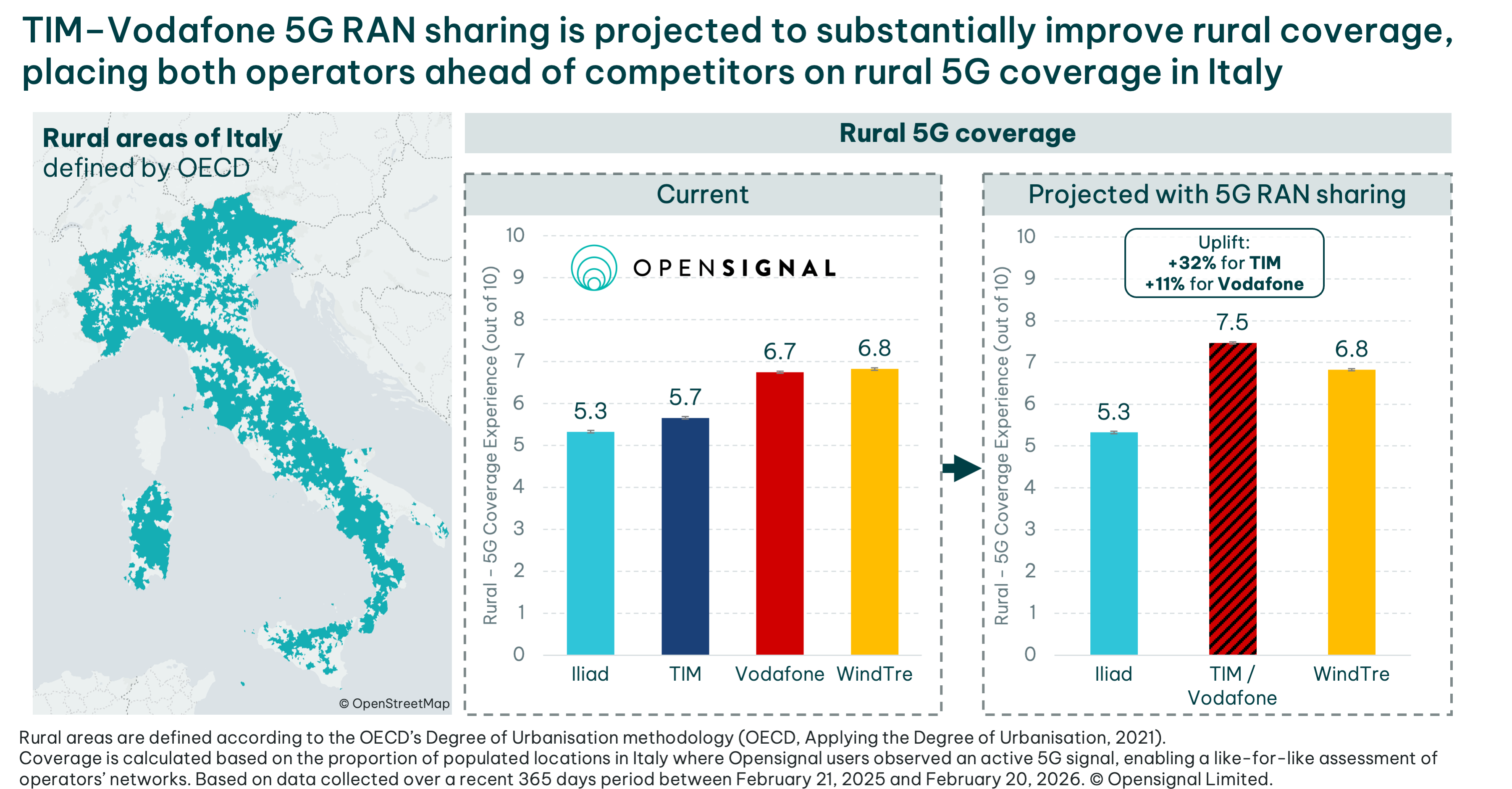

Immediate rural 5G uplift: Rural 5G Coverage Experience could rise to approximately 7.5 (on a 0–10 scale), up from 5.6 for TIM and 6.8 for Vodafone — a projected uplift of 32% and 11%, respectively.

No new spectrum, broader usable footprint: Both operators already hold same national allocations in low-band (700 MHz) and C-band (3.7 GHz). The benefit stems from infrastructure sharing and expanded deployment reach, not new spectrum access.

Measurable experience improvement: Even low-band 5G delivers a significant uplift in Consistent Quality over 4G in rural areas.

Rural 5G coverage: quantifying the immediate impact

Although operational details remain limited, the agreement’s stated objective is clear: pool resources to accelerate rural 5G rollout, with each operator managing half of Italy’s administrative regions.

To quantify the potential impact, we apply the same methodology Opensignal has used in previous consolidation and network integration analyses (including Vodafone–Three in the UK). We overlay the coverage footprints of both operators and estimate the proportion of populated areas where users would have access to the combined radio footprint, assuming existing sites continue to serve their current unique coverage areas. This provides a network-level projection without making assumptions about pricing, competition, or site rationalization.

Using Opensignal’s 5G Coverage Experience metric — which reflects the proportion of populated areas where users observed an active 5G connection, measured on a 0–10 scale — we project that rural scores for both operators would rise to approximately 7.5 following RAN sharing. Rural geographies are defined using the OECD’s Degree of Urbanisation (see Methodology).

This represents a substantial uplift from current levels: 5.6 for TIM and 6.8 for Vodafone.

A score of 7.5 implies that TIM and Vodafone users would observe 5G in around 75% of populated rural locations visited by users on their respective networks, up from roughly 57% for TIM and 67% for Vodafone today. Importantly, this represents a structural improvement in rural connectivity, directly supporting Italy’s ultra-wideband and 5G rollout obligations.

Spectrum: why the gains come from footprint, not bandwidth

Unlike several post-merger spectrum cases previously analyzed by Opensignal — including DTAC–TrueMove H (Thailand), Digi (Malaysia), and Taiwanese consolidation — TIM and Vodafone are not combining complementary spectrum portfolios.

Both operators already hold identical national allocations, including:

700 MHz (n28): 2×10 MHz each

3.7 GHz (n78): 80 MHz each

These are nationwide licenses. Therefore, neither operator gains access to new bands or additional spectrum bandwidth under this agreement.

The uplift comes instead from:

broader access to deployed 5G sites,

increased geographic deployment of each band, and

reduced asymmetry in rural rollout footprints.

In rural Italy, spectrum availability has not been the main constraint — deployment density and rollout pace have. RAN sharing effectively increases the usable radio-layer footprint per user, translating into improved Coverage Experience without expanding spectral capacity. Although spectrum holdings are broadly similar, deployment strategies have differed.

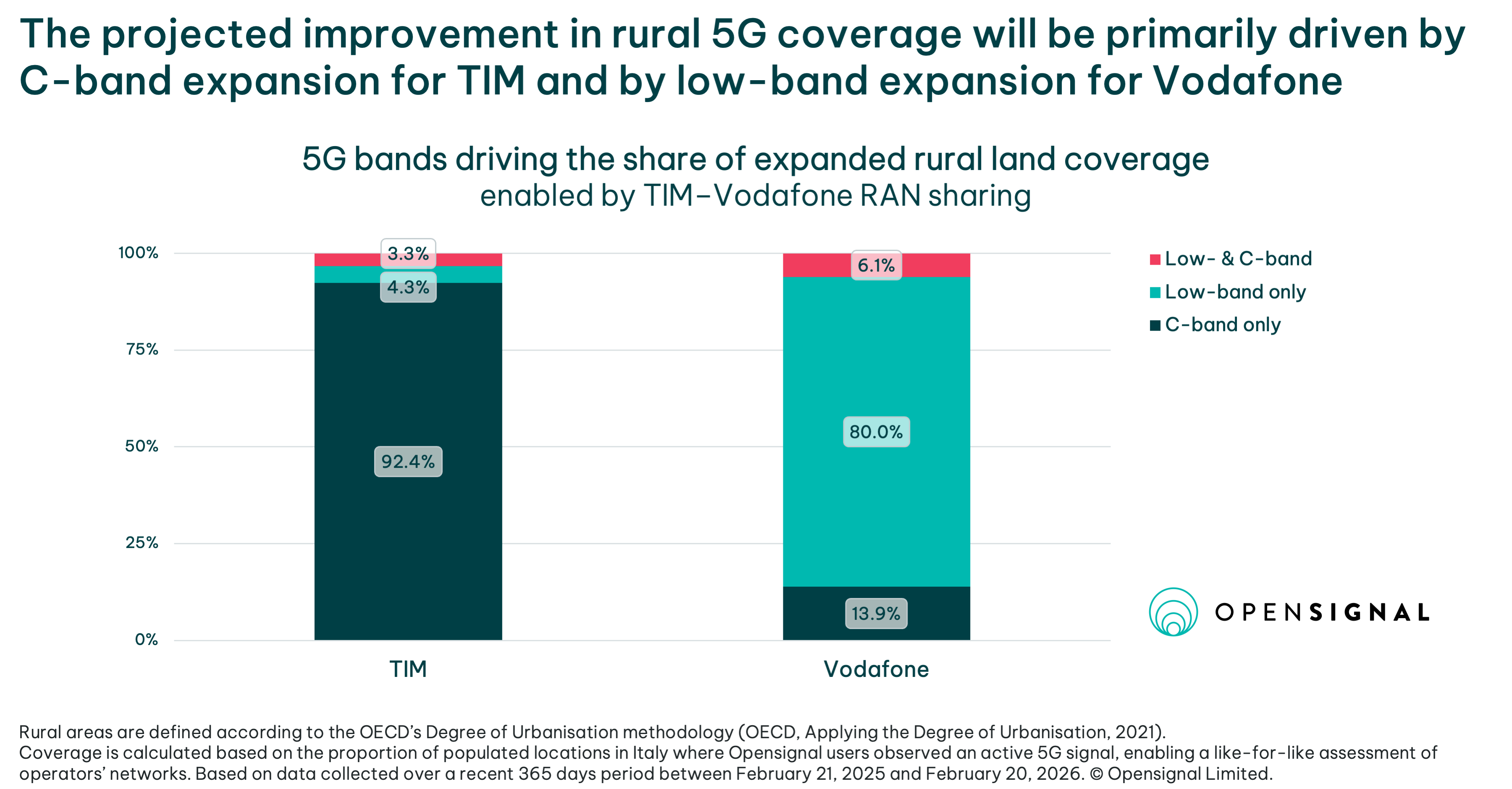

TIM users: expanded access to C-band

TIM’s 5G strategy has leaned more heavily on low-band (700 MHz) to maximize early coverage reach. Through RAN sharing, TIM customers gain wider access to Vodafone’s n78 (C-band) deployments.

This matters because C-band generally provides:

higher capacity and throughput,

stronger performance for data-intensive use cases, and

improved consistency under load.

As shown in Opensignal’s European spectrum analysis, increased use of 3.5 GHz correlates strongly with higher 5G Download Speeds and improved consistency.

Vodafone users: low-band reach extension

Vodafone has prioritised C-band deployment across the whole country. Through RAN sharing, Vodafone users gain expanded access to TIM’s low-band rural footprint.

While low-band cannot match C-band capacity, Opensignal data consistently shows that even low-band 5G provides improved reliability and higher Consistent Quality compared to 4G.

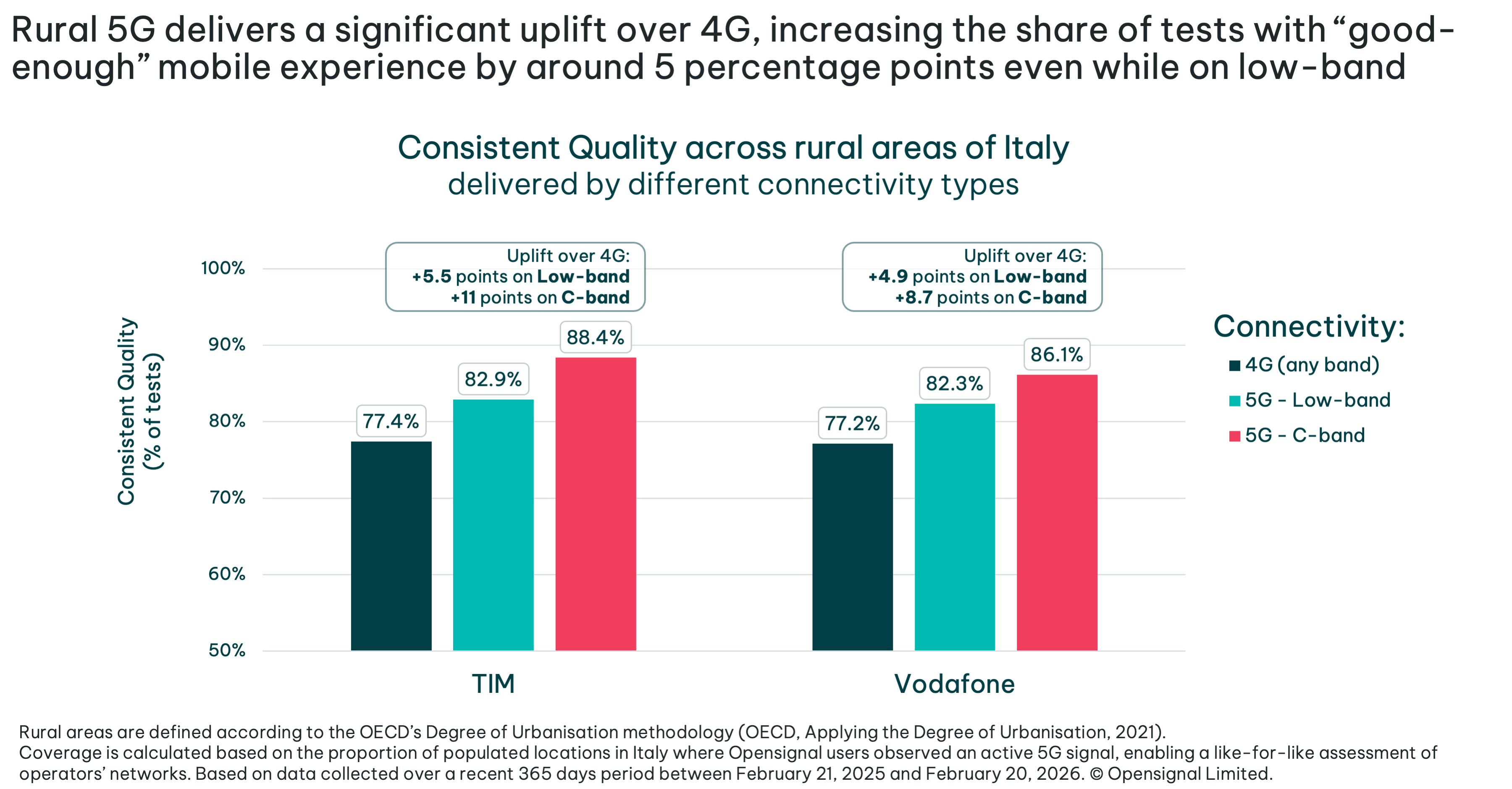

Customer experience: quantifying the uplift

To quantify user impact beyond coverage presence, we use Consistent Quality — a composite metric measuring how often users receive a “good enough” level of experience for everyday mobile applications.

The experience data from our users shows that in the case of TIM and Vodafone, upgrading from 4G to 5G in rural areas results in a 4.9–5.5 percentage-point uplift in Consistent Quality when 5G is delivered via low-band, and an 8.7–11 percentage-point uplift with C-band. The uplift is larger on TIM than Vodafone, with TIM's rural users seeing Consistent Quality rise from 77.4% on 4G to 88.4% on 5G C-band, which effectively halves the share of time with subpar network experience.

Strategic implications ahead of 2029 spectrum renewal

The timing of the agreement is significant. Italy’s upcoming spectrum renewal is expected to strengthen coverage obligations, potentially including stricter requirements linked to latency and connection density. In that context, expanded rural 5G reach supports both customer experience and regulatory compliance.

A key technical question concerns spectrum structure. A contiguous 100MHz mid-band block is widely regarded as a benchmark for high-performance 5G deployments. Today, TIM and Vodafone each hold 80MHz in 3.7GHz. While RAN sharing does not immediately increase spectrum bandwidth, it creates strategic optionality.

If future regulatory arrangements allow deeper coordination — potentially under a Multi-Operator Core Network (MOCN) framework — spectrum pooling could enable more efficient use of mid-band holdings. Such a development would shift the partnership from a rollout accelerator to a potential long-term capacity advantage. Given that Italy already permits MOCN structures under the Zefiro (Iliad–WindTre) arrangement, precedent exists.

Ultimately, beyond the immediate rural gains in coverage and customer experience, this agreement may signal a broader structural transition toward two major infrastructure partnerships:

Zefiro (Iliad–WindTre)

TIM–Fastweb+Vodafone

In a market defined by high capital intensity, demanding rollout obligations, and regulatory uncertainty, RAN sharing may prove not just an efficiency tool, but a cornerstone of sustainable 5G network leadership in the years ahead.

Conclusion

The TIM–Vodafone RAN sharing agreement delivers measurable short-term improvements in rural 5G Coverage Experience and Consistent Quality — without increasing spectrum holdings. The gains arise from expanded infrastructure access and complementary deployment footprints.

Looking ahead, the agreement provides strategic flexibility ahead of Italy’s 2029 renewal process and may create the foundation for deeper collaboration depending on regulatory evolution.

As implementation progresses, Opensignal will monitor whether an expanded 5G footprint translates into sustained improvements in consistency, mid-band utilization, and overall user experience across rural Italy.

If you’re interested in the mobile experience of Italian users, see the Italy: Mobile Network Experience (Dec 2025) report.

Methodology note

In this insight, rural areas are defined according to the OECD’s Degree of Urbanisation methodology; see OECD, Applying the Degree of Urbanisation (2021).

Opensignal Limited retains ownership of this insight including all intellectual property rights, data, content, graphs & analysis. Reports and insights produced by Opensignal Limited may not be quoted, reproduced, distributed, published for any commercial purpose (including use in advertisements or other promotional content) without prior written consent. Journalists are encouraged to quote information included in Opensignal reports and insights provided they include clear source attribution. For more information, contact [email protected].