It’s been 25 years since the world’s first commercial 3G launch. Today, 4G is universal, 5G rapidly expands, and 6G already looms on the horizon. And yet … 3G is still very much alive.

So why hasn’t it disappeared?

Because networks are no longer the bottleneck. Users, devices, and legacy dependencies are. Even in March 2026, as two advanced APAC markets — Japan and New Zealand — finally shut down their 3G networks, the technology continues to persist across much of the region. Not by choice, but by necessity.

3G in APAC: not one story but many

APAC’s 3G transition isn’t just moving at different speeds — it’s solving fundamentally different problems.

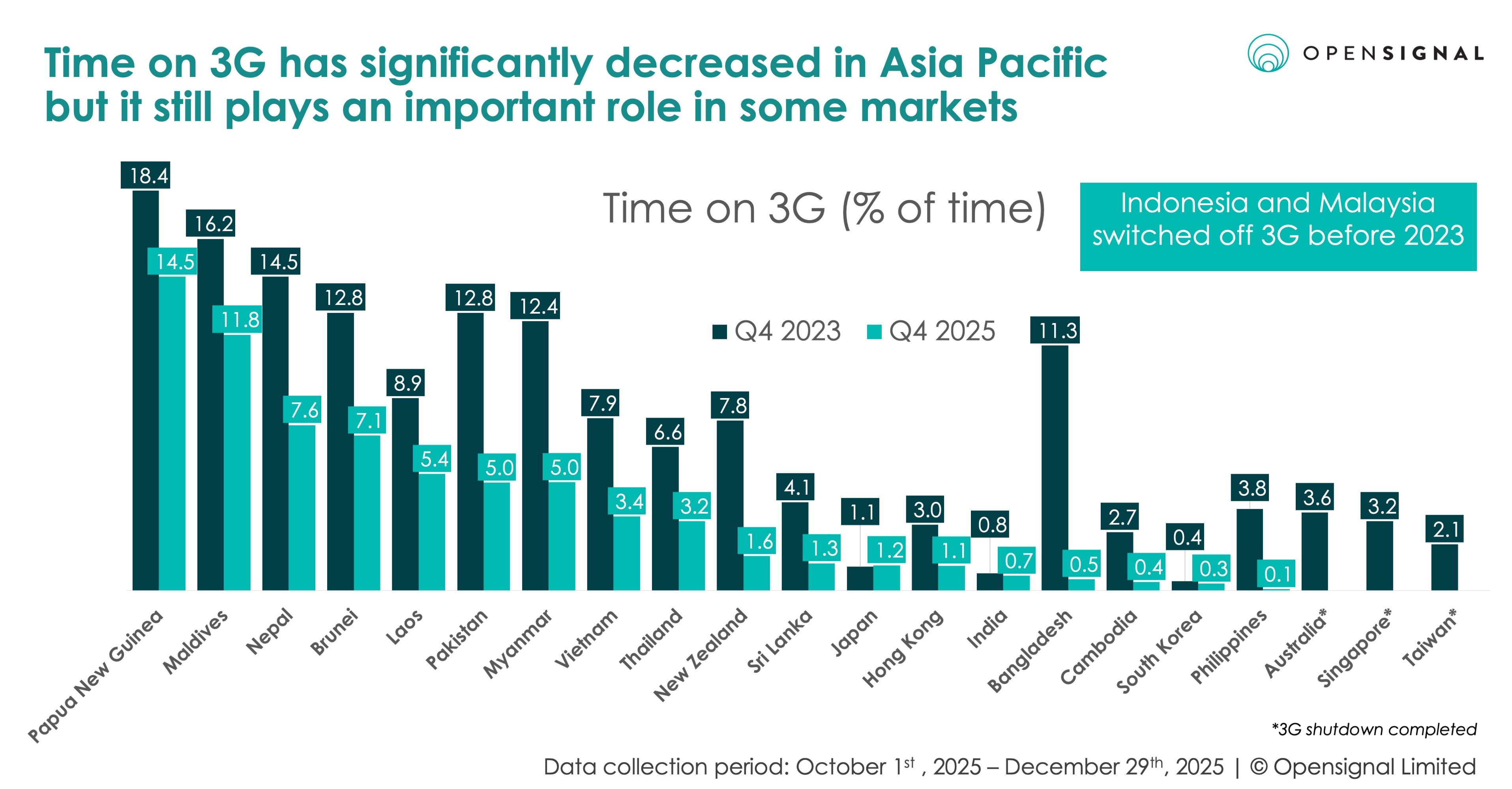

Looking at proportion of time our users spend connected to 3G network (Time on 3G) trends over the past two years, the region broadly falls into five groups:

- Mission Complete: Markets like Australia, Singapore, or Taiwan have already shut down 3G after earlier switching off 2G to prioritise 4G and 5G. Others, such as Malaysia or Indonesia, completed the transition earlier to accelerate national connectivity, but still retain their 2G networks.

- Fast Migrators: Countries including New Zealand, Bangladesh, Cambodia, and the Philippines have rapidly reduced 3G usage. Bangladesh stands out, dropping from 11.3% Time on 3G to just 0.5% in two years.

- Gradualists: Thailand, Vietnam, Laos, and Sri Lanka are progressing steadily, with some planning to retain 3G for several more years. Vietnam, for example, will use 3G networks until 2028 — but its 2G networks which have been gradually switched off since 2024 will be completely switched off by September 2026. In Thailand, the regulator NBTC has set a deadline for MNOs to submit shutdown plans for 2G and 3G by Q3 2026. Meanwhile, Laos plans to keep its 3G networks until 2035.

- 3G Residuals: Markets like India, Japan, and South Korea have shown minimal 3G usage for years, yet continue to operate these networks due to specific dependencies (e.g., IoT/M2M and users with incompatible devices).

- 3G Dependent: In countries such as Papua New Guinea, Nepal, and the Maldives, 3G still plays a significant role — and in some cases, even 2G remains widely used. Limited affordability of 4G/5G devices, lack of widespread access to mains electricity, the need for backup devices that can last a week on a single charge, and the high cost of upgrading remote infrastructure continue to slow the transition.

So why can’t we just flip the 3G switch?

We all understand the advantages of shutting down 3G. Refarming legacy spectrum improves 4G and 5G capacity and speeds, while reducing network complexity and costs.

So why can’t operators just turn it off and unlock these benefits right away?

Across APAC, one thing is clear: the persistence of 3G is driven by local constraints, not network preference. Even in markets we classified above as “3G Residuals”, where 3G usage is already minimal, 3G networks remain active. This is not limited to Asia Pacific — European users also experience noticeable Time on 3G across the continent, with some networks still operating both 2G and 3G.

The reason is simple: the transition away from 3G is far more complex than it seems:

- Legacy dependencies: 3G still supports a wide range of IoT and M2M use cases — from smart meters or traffic lights to vehicle trackers. Many rely on embedded 3G modules that would be costly or impractical to replace. Some are tied to critical services, including personal alarm devices — which prompts organisations like EENA to urge caution. Ironically, in some regions like Europe, operators even retain 2G longer than 3G, as it provides a low-cost, low-power foundation for simple IoT use cases, like sensors or meters.

- User behaviour: not all customers move at the same pace as networks. Millions still rely on 3G feature phones because they are affordable, durable, and have long battery life. For many users—especially in lower-income, rural, or older demographics—the benefits of upgrading are not compelling enough.

- Lack of device updates: As Australia found when it switched off 3G services (after earlier shutting down 2G), many smartphones lacked the necessary software updates to support 4G emergency calling.

- Roaming and voice gaps: while 4G and 5G rely on VoLTE, not all devices or international roaming agreements support it reliably. As a result, 3G continues to act as a universal fallback for voice calls and emergency access.

This is why 3G sunsets usually take many years and involve network upgrades, regulatory alignment, and sustained customer communication — and are often executed gradually, region by region.

This complexity is clearly illustrated by two advanced APAC markets that have only recently completed their 3G shutdowns: New Zealand and Japan.

New Zealand: coordinated and thorough approach

New Zealand’s operators shut down 3G within weeks of each other — 2degrees in February 2026, followed by One NZ and Sparks in March. This was the result of years of preparation and lessons learned from Australia’s earlier 3G shutdown. Operators phased out 3G gradually while upgrading infrastructure. They also worked closely with government initiatives like the Rural Mobile Programme to expand 4G coverage, ensuring rural areas were not left behind. At the same time, operators supported customers through device upgrades and targeted communication.

The result: one of the fastest 3G sunsets in APAC. In our previous analysis of New Zealand’s 3G phase-out, Time on 3G stood at 14%. Fast forward to Q4 2025, and it had dropped to just 1.6% as users migrated widely to 4G and 5G.

Japan: adapting to users’ preferences

Japan tells a different story. While Japanese networks were ready to move away from 3G, a segment of their subscribers were not.

KDDI shut down 3G in 2022, SoftBank in 2024, and Rakuten Mobile — as the latest entrant to the market — never relied on it. But NTT Docomo — the original 3G pioneer — only completed its shutdown in 2026.

Garakei phones

While competitors moved earlier, Docomo’s market leadership came with a heavier social burden, with 350,000 customers still relying on FOMA. This lingering user base helps explain why NTT Docomo chose to be the final holdout in the 3G sunset — any hasty shutdown would have effectively cut these users off the network. Many of these FOMA customers remain loyal to “garakei” feature flip phones — a uniquely Japanese phenomenon — that do not support newer network generations.

These devices are especially popular among older users who value their simplicity and familiarity. For this group, switching to modern smartphones — with touchscreens and complex interfaces — can be especially challenging.

To manage the transition, Japanese operators have offered alternatives over the years, including simplified smartphones and 4G-compatible “garakei”-style devices, helping users migrate at their own pace.

Japan highlights an important lesson: even in highly advanced markets, user behaviour — not network readiness — often is the limiting factor.

The final act of 3G in APAC

3G shutdowns won’t happen overnight and require a clear and long-term strategy. As the remaining APAC markets approach their own inevitable 3G sunsets, four observations stand out:

- Communicate early and clearly: Shutting down 3G requires years of preparation and sustained customer engagement.

- Make upgrades accessible: Affordable devices and simple alternatives are critical to moving users off legacy networks — especially those who are reluctant or unable to upgrade. There is also value, as demonstrated by several regulators in the region, in prohibiting the importation or connection of 2G- or 3G-only phones (e.g. in Vietnam or Thailand) ahead of the sunset date, so consumers do not invest in smartphones with a very limited lifespan.

- Support the most vulnerable users: Elderly populations, rural communities, and those dependent on legacy devices need targeted support. In some cases, operators may need to provide the safety net, e.g. through network sharing or Direct-To-Direct (D2D) partnerships to provide emergency coverage in areas where 3G signal suddenly disappears.

- Address legacy dependencies: Operators must plan the migration of IoT and M2M devices still reliant on 3G — prioritising critical emergency services, enabling device upgrades, and, where necessary, maintaining fallback technologies like 2G or LPWA to ensure continuity.

If you are interested in more analysis of Japan or New Zealand’s mobile or fixed broadband landscape — check out our previous reports. Please contact us if you are looking for a more custom approach. Subscribe to our newsletter to stay up to date!

The editorial views expressed in this article are solely those of the author and do not necessarily reflect the views of Opensignal.

Opensignal Limited retains ownership of this insight including all intellectual property rights, data, content, graphs & analysis. Reports and insights produced by Opensignal Limited may not be quoted, reproduced, distributed, published for any commercial purpose (including use in advertisements or other promotional content) without prior written consent. Journalists are encouraged to quote information included in Opensignal reports and insights provided they include clear source attribution. For more information, contact [email protected].