UK altnets have built the fibre. The bigger question now is how fast consumers are signing up. Challenger operators now pass an estimated 66% of UK premises with superfast broadband coverage, but Opensignal's data shows they still account for just 11.4% of national broadband subscriptions. Converting the extensive fibre coverage built over the recent years into active subscribers is the defining challenge facing the broadband operators in Europe today.

This analysis draws on Opensignal's Subscriber Analytics data for Q2 2026, which tracks device-level switching events and market share across UK regions. Comparing this snapshot against Q4 2024, an eighteen-month window, we map where consumers are actually moving, and at what pace.

Key Findings:

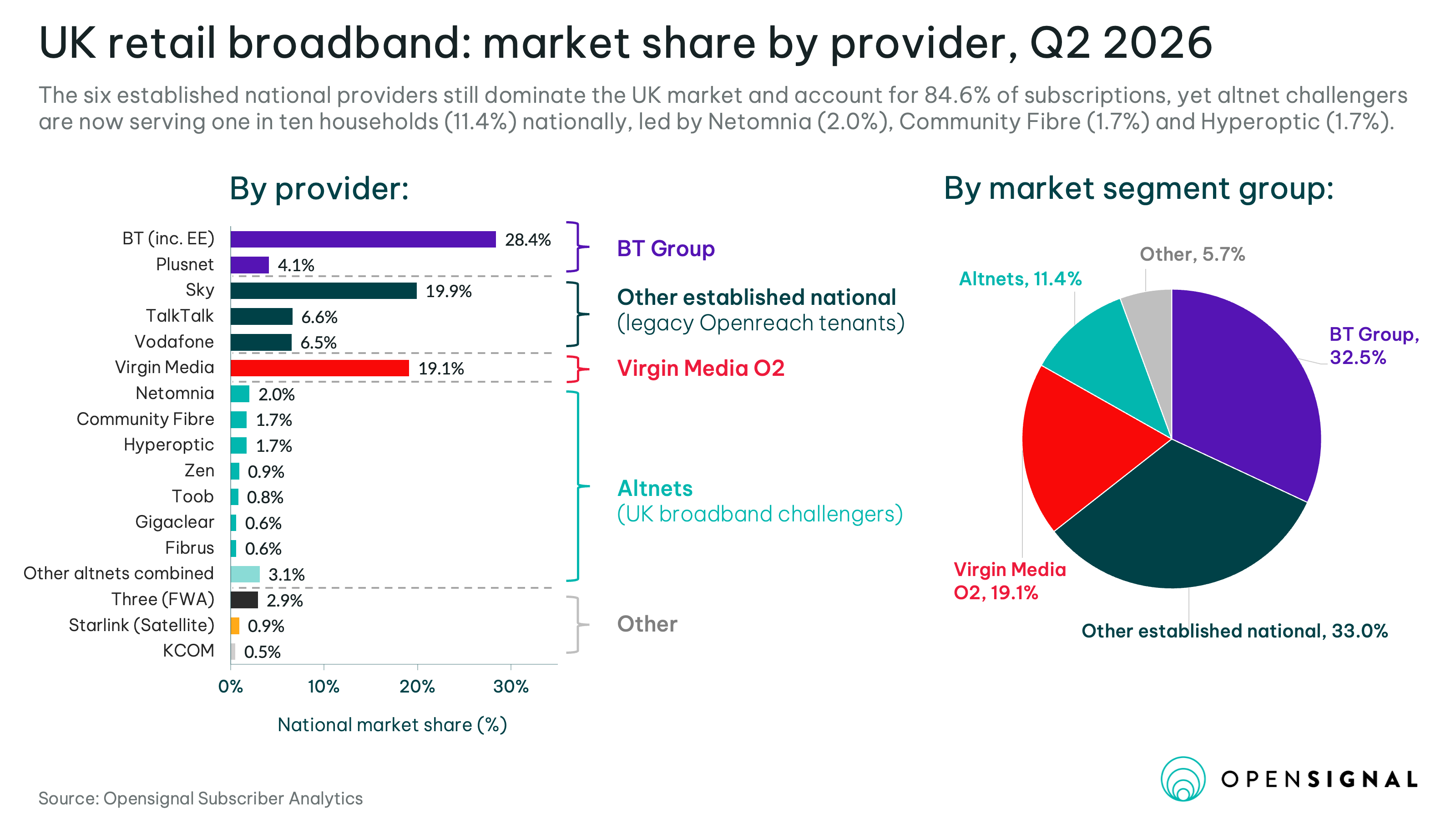

- Altnets now serve one in ten household connections in the UK. The established segment of BT (including EE), Plusnet, Sky, TalkTalk and Virgin Media still dominate with 85% of retail connections, yet altnets pulled away 4.4 percentage points in just eighteen months to account for 11% of the market, with every major challenger brand growing.

- Altnets are strongest today exactly where switching activity took place recently. London and Northern Ireland lead on altnet share (21% and 18%), having gained about a third of that share between Q4 2024 and Q2 2026. This pattern, of altnets recording a big chunk of their wins in the past eighteen months, holds across all twelve UK regions: the switching we are reporting points to where the market reshaping is headed.

- Altnets have gained share at the expense of the established national players, but which incumbent lost ground varied by region. In Northern Ireland the swing came almost entirely at BT Group's expense, while Virgin Media O2 barely moved. London's loss was opposite: Virgin Media O2 posted its steepest regional decline, while BT Group gave up only a single point.

Incumbents still dominant, but eroding fast

In our recent UK Fixed Broadband Experience report (December 2025), which measured the network experience UK users received from their providers, we found that while incumbents still take all the national awards by virtue of market dominance, across analysed cities altnets were often delivering superior network experience to their customers, shifting the competitive landscape decisively in their favour.

Industry body Independent Network Cooperative Association's (INCA) State of the Altnets 2026 report puts altnets' collective footprint at 19.7 million premises passed, representing 66% of the 29.7 million premises with superfast coverage reported in Ofcom's Connected Nations 2025. Against that footprint, altnets have signed up 3.5 million live connections, meaning they account for 11.9% of the UK's 29.5 million active broadband subscriptions estimated by Telegeography, closely matching Opensignal Subscriber Analytics' own figure of 11.4%.

As of Q2 2026 the three largest established providers hold roughly two-thirds of the UK market between them: BT (including EE) at 28.4%, Sky at 19.9%, and Virgin Media O2 at 19.1%. Sky, TalkTalk and Vodafone have long been known as retail resellers of the Openreach network, set apart from Virgin Media's own cable infrastructure. That distinction now understates how far the market has moved: each of the three also carries connections over CityFibre, so a growing share of their base already sits on altnet infrastructure.

Collectively, altnets hold 11.4% of the market, though no single altnet comes close to matching any of the established providers individually. Within that total, Netomnia leads at 2.0%, just ahead of Community Fibre and Hyperoptic (both 1.7%). Netomnia is still trading independently while its acquisition by nexfibre awaits CMA clearance. A long tail of full-fibre challenger providers, including Zen, Toob, Gigaclear and Fibrus, makes up most of the rest.

The rest of the market is driven by fixed-wireless and satellite. Notably, Three's Fixed Wireless Access (FWA) alone, at 2.9%, has a larger national share than any established altnet, with Starlink also playing a big role in the national market, at 0.9% market share.

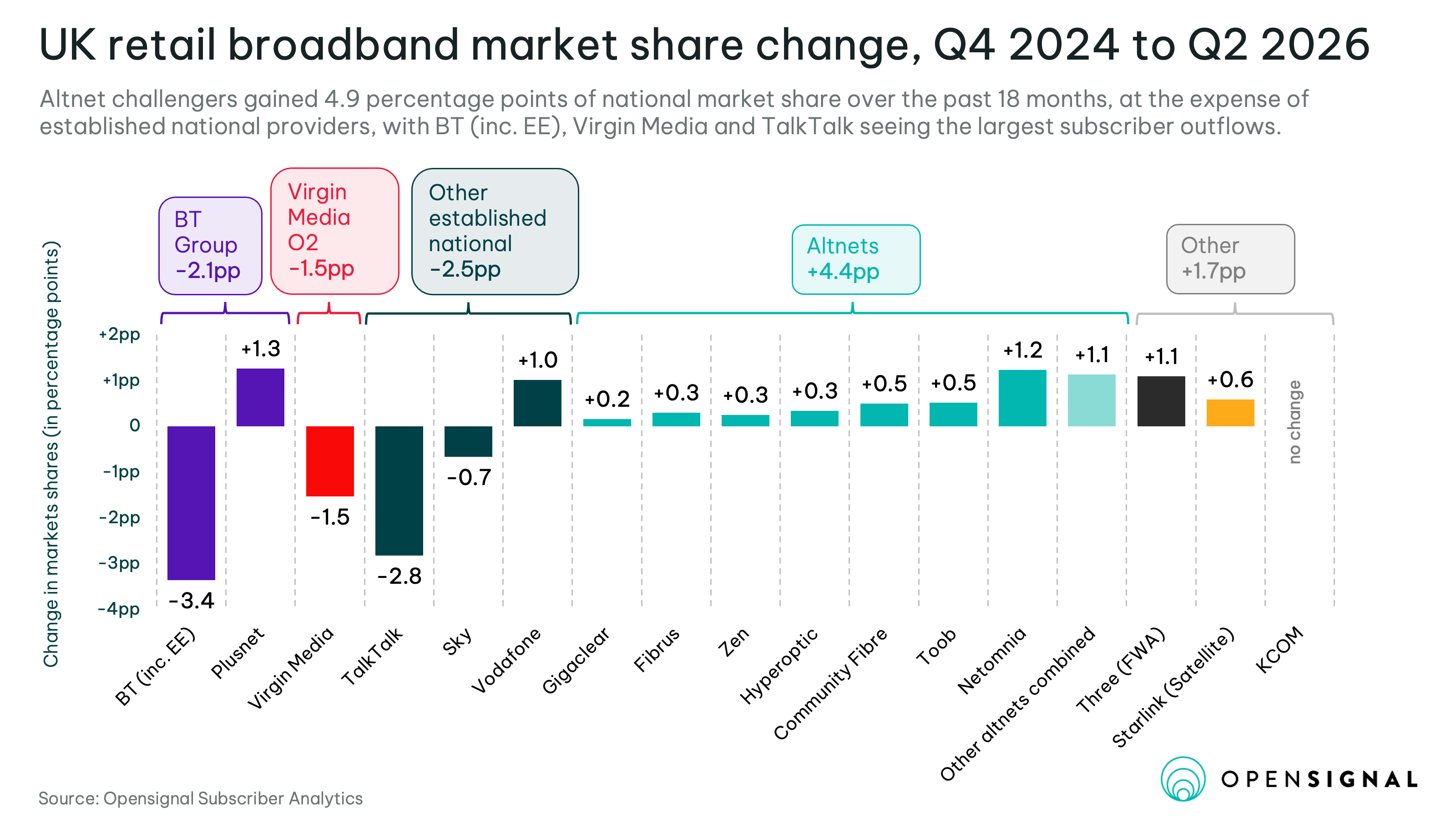

Customer flows over the eighteen months to Q2 2026 reveal rapid change in the UK retail broadband competitive landscape. Altnets gained 4.4 percentage points nationally, with every major challenger brand growing, from Gigaclear to Netomnia.

The gains came at the expense of the established-national segment, but the losses there were not uniform. BT Group itself hides an internal disparity: while its parent brand lost 3.4pp share, its budget arm Plusnet gained 1.3pp, indicating BT is successfully retaining part of the outflow within its own portfolio. Virgin Media O2 lost 1.5pp, taking significant loss driven by altnet advent.

TalkTalk and Sky lost share, at -2.8pp and -0.7pp, respectively, but Vodafone gained 1.0pp, one of only two established-national brands, alongside Plusnet, to grow. Vodafone's gain owes much to its partnership with CityFibre, the UK's wholesale altnet heavyweight. Sky and TalkTalk sell over CityFibre too, but having signed partnerships more recently and not on the same terms. Vodafone has been CityFibre's national tenant since 2017, with volume and exclusivity commitments, giving it a significant head start on TalkTalk, whose wholesale agreement began around 2020, and Sky, which only went live in 2025.

Alongside the altnet story, Three's fixed-wireless product added +1.1pp and Starlink +0.6pp, a global shift in the industry we've covered in more depth in our reports on FWA's growing disruption of fixed broadband and on Starlink's move from last resort to first choice.

London and Northern Ireland are the hotbeds of subscriber change

One of the revealing stories of the UK broadband market today is that the regions where altnets are most concentrated are also where consumers have switched fastest over the last eighteen months, a sign that the main act of market reshaping is happening now.

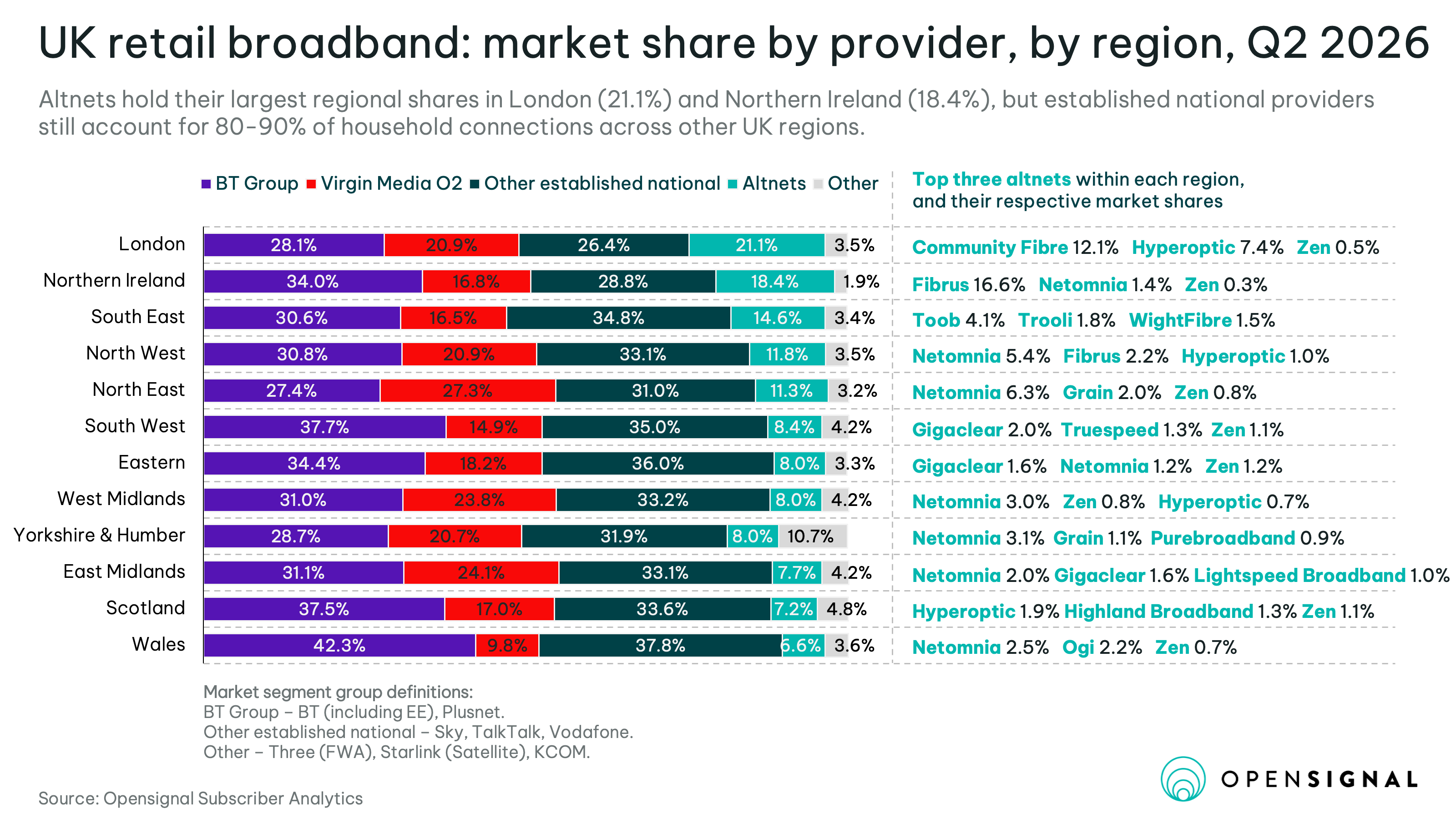

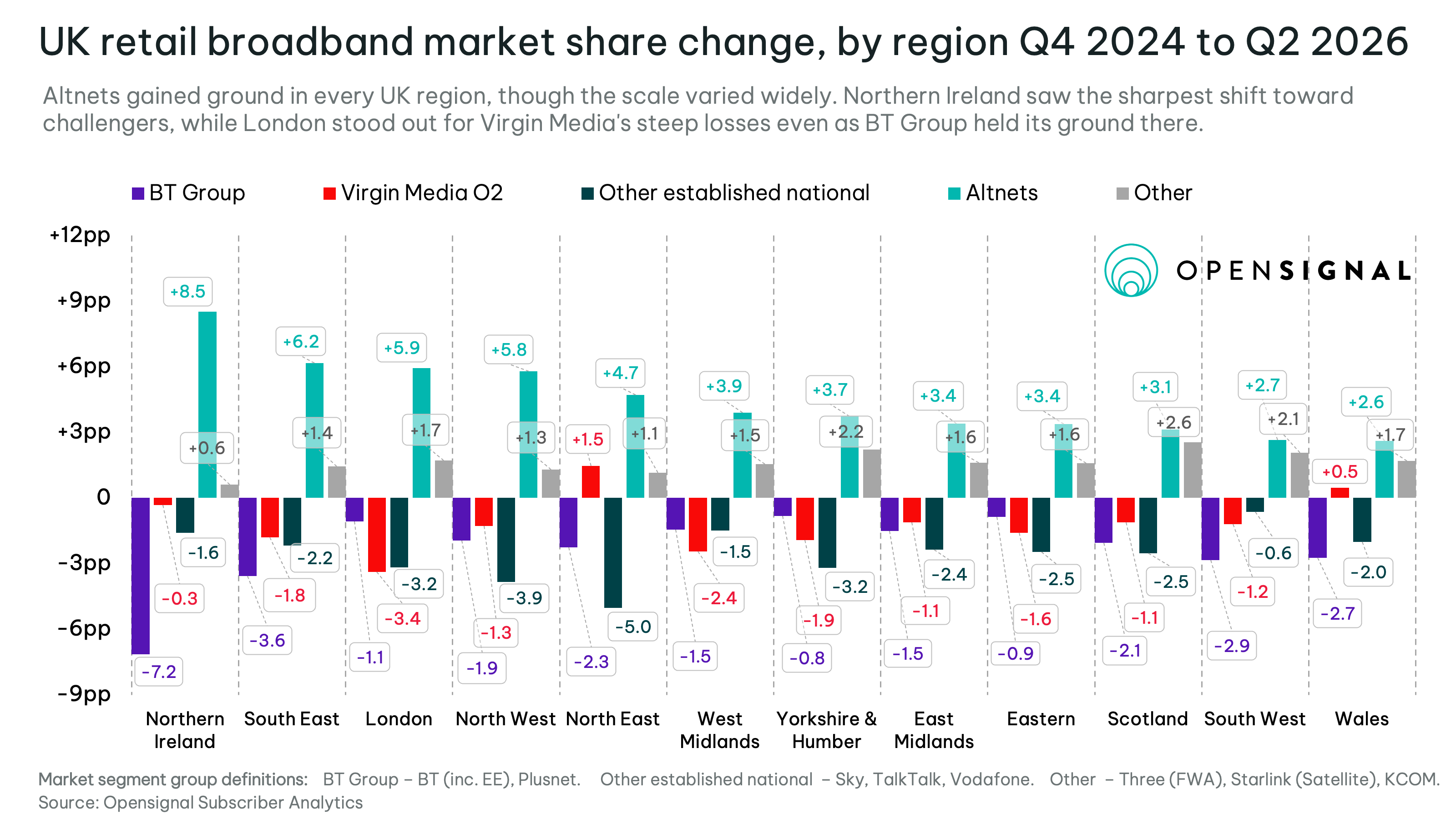

London and Northern Ireland lead the rest of the UK on altnet market share, at 21.1% and 18.4% of active altnet connections respectively. They also lead on the switching altnets have won, with their shares up 5.9 and 8.5 percentage points since Q4 2024, meaning roughly a third of London's current share, and nearly half of Northern Ireland's, was gained in just the past eighteen months. Wales and Scotland sit at the other end on both counts, with the lowest shares (6.6%, 7.2%) and the slowest growth (+2.6pp, +3.1pp). The pattern holds across all twelve regions: altnets are strongest today exactly where switching activity has been most concentrated recently, with the regions of highest altnet penetration also being those adding share fastest. We are in the midst of the market reshaping, and the switching activity of the past eighteen months points to where the momentum is headed.

However, the customer bases altnets accumulated came from different providers in the different regions – Northern Ireland's swing came almost entirely at BT Group's expense (-7.2pp), while Virgin Media O2 barely moved there (-0.3pp). London's loss was broader: Virgin Media O2 posted its own steepest regional decline (-3.4pp), the Sky/TalkTalk/Vodafone segment fell almost as far (-3.2pp), but BT Group gave up only a point (-1.1pp).

What happens next

Two forces will shape the next eighteen months: regulation and consolidation.

Ofcom's Telecoms Access Review 2026-31 confirmed the existing regime through 2031 rather than overhauling it. Expanding the share of footprint the authority deemed as having material and sustainable competition (called "Area 2") from 70% to 86% of premises, a tacit acknowledgment that altnet-driven competition is now established across a far wider footprint than its 2021 assumptions anticipated. In effect, Ofcom has chosen to let infrastructure competition, rather than price regulation, discipline the market across most of the country for the rest of the decade.

Consolidation is the bigger near-term story. In February 2026, nexfibre, backed by Virgin Media O2's parent companies and InfraVia, agreed to buy Netomnia's network for £2bn, with retail arm YouFibre sold separately to VMO2 for £150m. The CMA referred the deal to a Phase 2 investigation, with a decision due by 15 December 2026, its concern being the roughly 80% overlap between the two networks. Rather than extending fibre into new areas, the deal consolidates two networks already racing to serve the same premises, which is why CityFibre, itself a rival bidder, warns it would remove a competitor and risk a BT/VMO2 duopoly.

The direction of travel is reasonably clear. Financial pressure is pushing the smaller players toward the door even as stronger ones merge, which points to fewer altnet brands and larger surviving shares over the coming year. For established providers, the regional pattern may matter more than the national number. In Northern Ireland and London, the ambitious local rivals have taken commanding market momentum – Fibrus in the former, and Community Fibre and Hyperoptic in the latter. This is while Virgin Media O2's cable footprint has held up best in the North East and Wales. Vodafone's national gain, one of only two established-national brands to grow alongside Plusnet, shows what deeper altnet wholesale partnerships can deliver: selling over CityFibre alongside its Openreach lines turned network diversification into subscriber growth. The other established names can be expected to continue to pursue wholesale partnerships beyond Openreach wherever the coverage and commercial terms allow.

More from Opensignal

Opensignal Subscriber Analytics tracks market share, switching flows, and network experience at sub-regional granularity. If you want to map where your subscribers are at risk, and where your acquisition opportunity sits, get in touch. For more UK analysis, see our UK Market Insights.

Opensignal Limited retains ownership of this insight including all intellectual property rights, data, content, graphs & analysis. Reports and insights produced by Opensignal Limited may not be quoted, reproduced, distributed, published for any commercial purpose (including use in advertisements or other promotional content) without prior written consent. Journalists are encouraged to quote information included in Opensignal reports and insights provided they include clear source attribution. For more information, contact [email protected].